In the intricate world of business finance, the timing of recognizing costs can significantly impact a company’s financial health and reporting accuracy. Among the various accounting treatments, deferred expenditure stands out as a critical concept, allowing businesses to spread the impact of certain outlays over the periods in which they yield benefits. Understanding deferred expenditure is fundamental for investors, financial analysts, and business owners seeking a clear picture of a company’s financial performance and strategic allocation of resources.

Unpacking the Concept of Deferred Expenditure

Deferred expenditure refers to costs incurred in one accounting period that are expected to provide benefits in future accounting periods. Instead of expensing the full amount immediately, these costs are capitalized as an asset on the balance sheet and then systematically expensed over their useful life through a process called amortization. This accounting treatment is rooted in the matching principle, a core tenet of accrual accounting, which dictates that expenses should be recognized in the same period as the revenues they help generate.

Defining Deferred Expenditure

At its core, a deferred expenditure is a payment made upfront for a service or asset that will be consumed or utilized over an extended period. Rather than hitting the income statement as a single, large expense in the period of payment, it is treated as an asset that depreciates or amortizes over the periods it contributes to the business’s operations or revenue generation. This provides a more accurate reflection of the company’s profitability by aligning costs with the benefits they produce. Without deferral, a company might show a large loss in the period of a significant outlay, even if that outlay is designed to drive revenue for years to come.

Key Characteristics

Several characteristics define deferred expenditures:

- Future Benefit: The most crucial aspect is that the expenditure provides economic benefits beyond the current accounting period.

- Materiality: While theoretically any future-benefiting cost could be deferred, generally only material amounts are treated this way due to the effort involved in tracking and amortizing smaller sums.

- Non-Physical Nature: Unlike tangible assets (which are depreciated), deferred expenditures often relate to intangible assets or services.

- Systematic Allocation: The cost is systematically expensed over its useful life, usually on a straight-line basis, though other methods may apply depending on the nature of the expenditure.

The Accounting Principle Behind Deferrals

The rationale for deferred expenditure primarily stems from the matching principle under accrual accounting. This principle aims to match expenses with the revenues they help generate. If an expenditure provides benefits over several years, expensing it entirely in the year of payment would distort the financial statements, making that year appear less profitable and subsequent years artificially more profitable. By deferring the expenditure, the cost is spread out, providing a more accurate representation of profitability across all affected periods. This ensures that the financial statements provide a fairer and more consistent view of a company’s performance over time, which is invaluable for stakeholders making informed decisions.

Common Examples Across Industries

Deferred expenditures manifest in various forms across different industries, each representing an investment made today for future returns. Recognizing these common examples helps solidify the understanding of this financial concept.

Research and Development Costs

While many R&D costs are expensed as incurred, certain development costs (especially those related to specific projects with probable future economic benefits, like the development of a new software product or a pharmaceutical drug that has reached a certain stage of technical feasibility) can be deferred. These costs, once deferred, are then amortized over the period the resulting product is expected to generate revenue. This treatment acknowledges the significant upfront investment required for innovation and its long-term revenue potential.

Advertising and Marketing Campaigns

Large-scale advertising campaigns, particularly those designed to build brand awareness over an extended period rather than generate immediate sales, are prime candidates for deferred expenditure. For instance, a major national advertising blitz for a new product launch, where the benefits (increased brand recognition, market share) are expected to accrue over several years, might be deferred. The cost would then be amortized over the estimated period of benefit, perhaps two to five years, rather than being expensed entirely in the quarter the ads ran.

Large Maintenance or Renovation Projects

Significant maintenance or renovation projects that extend the useful life or increase the efficiency of an existing asset are often deferred. If a company undertakes a major overhaul of its machinery that adds several years to its operational life, the cost of this overhaul might be capitalized and amortized over the extended life. This is distinct from routine maintenance, which is expensed immediately, as routine maintenance simply keeps the asset operational without extending its life or significantly enhancing its value.

Software Development Costs

Companies developing software for internal use or for sale to external customers frequently defer the costs incurred during the application development stage. Once technical feasibility is established and the project is expected to generate future economic benefits, development costs such as employee salaries, consulting fees, and allocated overhead are capitalized. These deferred costs are then amortized over the software’s estimated useful life, which reflects the period over which the software is expected to provide value.

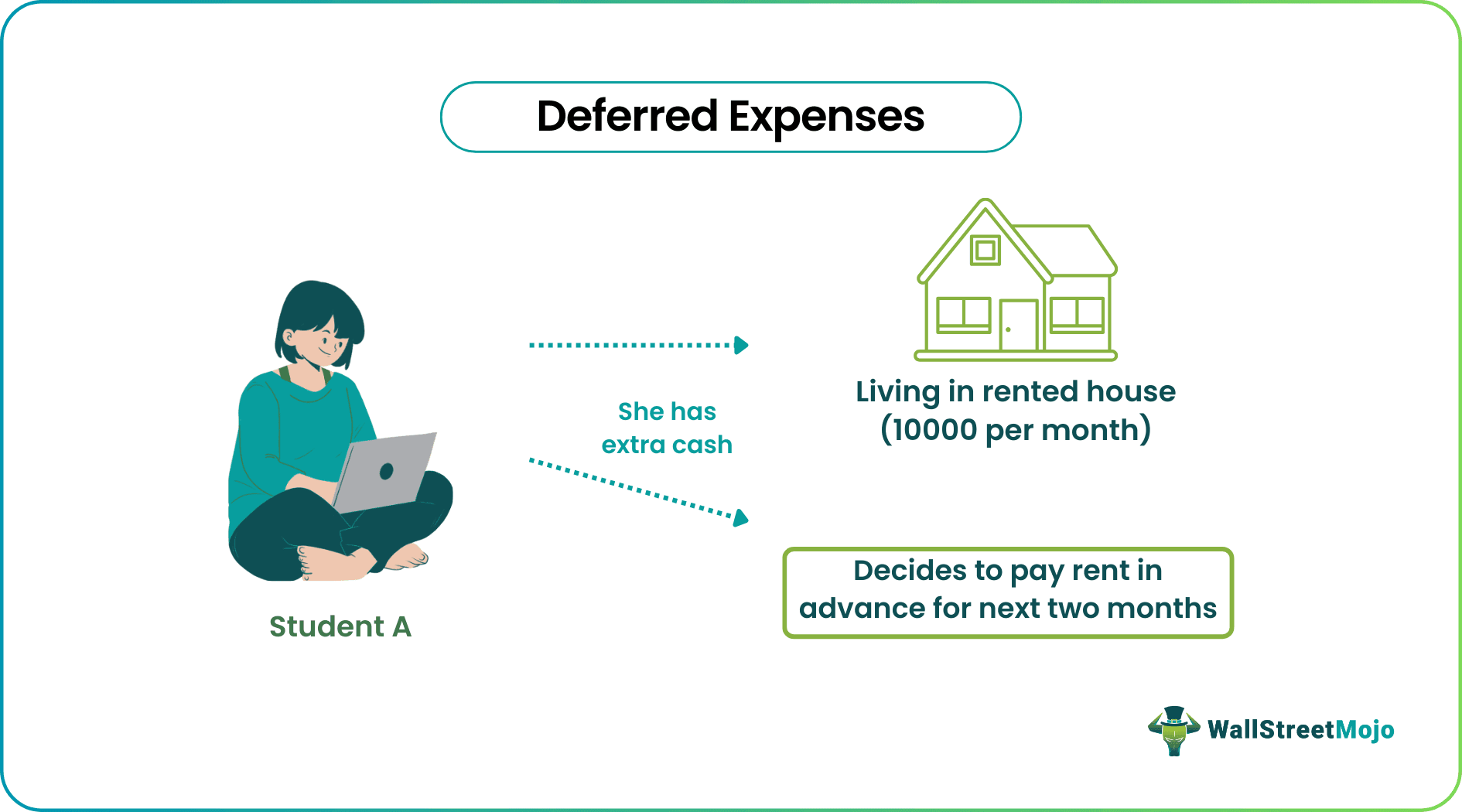

Prepaid Expenses

While closely related, prepaid expenses are a simpler form of deferred expenditure. These include items like prepaid rent, insurance premiums, or subscription services. A company pays for these services upfront but will consume them over a future period, typically within one year. The unconsumed portion is recorded as a prepaid asset on the balance sheet and then expensed as the service is used or the period lapses. While technically a deferral, prepaid expenses are usually classified separately from longer-term deferred expenditures due to their short-term nature.

Why Companies Defer Expenditures: Strategic and Financial Implications

The decision to defer expenditures is not merely an accounting formality; it carries significant strategic and financial implications for a business. It influences how a company’s financial health is perceived and how management makes decisions.

Accurate Financial Reporting

The primary reason for deferring expenditures is to ensure accurate financial reporting. By matching expenses with the revenues they help generate, deferred expenditures prevent income statements from being skewed by large, one-off payments. This leads to a smoother, more representative earnings stream over time, providing a clearer picture of a company’s true profitability and operational efficiency. For stakeholders, this consistency is crucial for evaluating performance trends and making informed investment decisions.

Smooths Out Earnings

Deferring large, infrequent expenditures prevents volatile swings in reported earnings. Imagine a company that undertakes a massive marketing campaign every three years. If the entire cost were expensed in the year of the campaign, that year’s profits would plummet, only to rebound in the subsequent years. Deferral and amortization mitigate this volatility, presenting a more stable and predictable earnings pattern, which can be attractive to investors who prefer consistency.

Potential Tax Advantages

In many jurisdictions, deferred expenditures can offer tax advantages. By capitalizing and amortizing certain costs, companies can spread out the tax deduction over several years, rather than taking a large deduction in a single year. This can lead to a more predictable tax liability and, in some cases, optimize tax planning by aligning deductions with periods of higher taxable income, although the specifics depend heavily on local tax laws and regulations.

Better Decision-Making for Investors and Management

For investors, a company’s consistent and accurate financial reporting, facilitated by deferred expenditures, provides a more reliable basis for valuation and investment analysis. Management also benefits, as the financial statements provide a truer reflection of departmental performance and project returns. This allows for better capital allocation decisions, strategic planning, and performance evaluations, ensuring resources are directed towards initiatives that yield long-term value.

The Amortization Process: Spreading the Cost Over Time

Amortization is the systematic process by which deferred expenditures are recognized as expenses on the income statement over their useful life. It is conceptually similar to depreciation for tangible assets but applies specifically to intangible assets or deferred costs.

Understanding Amortization

When an expenditure is deferred, it is initially recorded as an asset on the balance sheet. Amortization is the mechanism that gradually reduces the value of this asset while simultaneously recognizing a portion of its cost as an expense in each accounting period. This ensures that the cost is spread out over the periods that benefit from the expenditure, aligning with the matching principle. The amortization period is typically based on the estimated useful life of the asset or the duration over which the benefits are expected to accrue.

Methods of Amortization

The most common method of amortization is the straight-line method. Under this approach, the deferred expenditure is divided equally by its estimated useful life (in years or months), and that equal portion is expensed in each period. For example, if a $100,000 deferred expenditure has an estimated useful life of 5 years, $20,000 would be amortized annually. Other, less common methods, such as the declining balance method or units of production method, might be used if the asset’s economic benefits are expected to decline over time or are directly tied to production levels, respectively. The chosen method should consistently reflect the pattern in which the economic benefits are consumed.

Impact on Financial Statements

Amortization impacts both the balance sheet and the income statement.

- Balance Sheet: Each period, the accumulated amortization reduces the carrying value of the deferred expenditure asset. This means the asset’s book value decreases over its useful life until it reaches zero (or its residual value, if any).

- Income Statement: The amortization expense is recognized on the income statement in each period. This reduces reported net income and, consequently, earnings per share.

The statement of cash flows is not directly affected by amortization expense itself, as amortization is a non-cash expense. However, the initial cash outlay for the deferred expenditure would be reflected as an investing activity.

Distinguishing Deferred Expenditure from Other Financial Terms

The terminology in finance can be confusing, with several terms sounding similar but having distinct meanings. It’s crucial to differentiate deferred expenditure from related concepts to avoid misinterpretation.

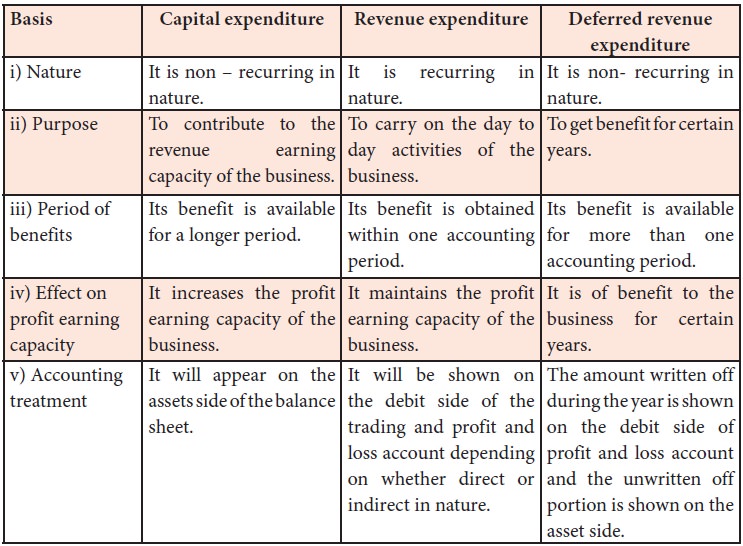

Deferred Expenditure vs. Capital Expenditure (CAPEX)

While some deferred expenditures are capitalized (recorded as assets), they are distinct from traditional capital expenditures (CAPEX). CAPEX refers to funds used by a company to acquire, upgrade, and maintain physical assets such as property, plants, buildings, technology, or equipment. These are tangible assets. Deferred expenditures, on the other hand, often relate to intangible assets or services like R&D for software, large advertising campaigns, or long-term leasehold improvements that are not directly acquiring a new physical asset but enhancing or prolonging the benefit of existing ones or creating new intangible value. The common thread is capitalization, but the nature of the asset differs.

Deferred Expenditure vs. Operating Expenditure (OPEX)

Operating expenditures (OPEX) are the costs a company incurs to run its day-to-day business operations. These include salaries, rent, utilities, office supplies, and routine maintenance. OPEX is expensed immediately in the period it’s incurred, directly affecting the current period’s profitability. Deferred expenditures, in contrast, are not expensed immediately because their benefits extend beyond the current period; they are capitalized and then amortized over time. The distinction lies in the timing of expense recognition and the duration of the benefit.

Deferred Expenditure vs. Prepaid Expenses

As briefly mentioned, prepaid expenses are a specific type of deferred expenditure, typically short-term (within one year). They represent payments made for goods or services that will be received or consumed in the near future. Examples include prepaid rent, insurance, or subscriptions. While both are initially recorded as assets and expensed over time, “deferred expenditure” often implies a longer-term outlay for intangible assets or services with benefits spanning multiple years, whereas “prepaid expenses” usually covers more routine, recurring operational costs with a shorter deferral period.

Deferred Revenue

Deferred revenue, or unearned revenue, is the inverse of deferred expenditure. It represents cash received by a company for goods or services that have not yet been delivered or performed. Instead of immediately recognizing this cash as revenue, the company records it as a liability on its balance sheet. Once the goods are delivered or services are performed, the deferred revenue liability is reduced, and the revenue is recognized on the income statement. This term relates to future income, whereas deferred expenditure relates to future expenses.

Challenges and Considerations

While deferred expenditures offer significant benefits for financial reporting, they also present certain challenges and considerations for businesses and auditors.

Subjectivity in Estimation

One of the primary challenges is the inherent subjectivity in estimating the useful life or the period of benefit for a deferred expenditure. For example, determining how many years a marketing campaign will continue to generate benefits or how long a piece of software will be economically viable requires significant judgment. Inaccurate estimations can lead to either overstating or understating assets and future expenses, thereby affecting the accuracy of financial statements. This subjectivity often requires robust internal controls and clear accounting policies.

Potential for Manipulation

Although less common with stringent accounting standards, there is a theoretical potential for companies to manipulate financial statements by aggressively or conservatively deferring expenditures. Overly deferring costs could artificially inflate current period profits, while under-deferring could depress them. Independent audits and adherence to Generally Accepted Accounting Principles (GAAP) or International Financial Reporting Standards (IFRS) are crucial safeguards against such practices, ensuring that deferral decisions are based on economic substance rather than financial engineering.

Impact of Changing Accounting Standards

Accounting standards evolve, and changes can impact how certain expenditures are treated. For instance, new standards might dictate stricter criteria for capitalizing R&D costs or alter the permissible amortization periods. Companies must stay abreast of these changes to ensure compliance and avoid restatements, which can be costly and damage investor confidence. The dynamic nature of financial regulations means that what qualifies as a deferred expenditure today might be treated differently in the future.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.