The prime rate stands as a cornerstone of the financial system, a pivotal benchmark that influences a vast array of lending products, from credit cards and personal loans to mortgages and business lines of credit. Understanding “what is current prime rate today” isn’t merely a matter of financial trivia; it’s an essential component of informed personal finance and sound business strategy. This rate, primarily dictated by the monetary policy decisions of central banks like the U.S. Federal Reserve, directly impacts the cost of borrowing and, by extension, the financial health of individuals and businesses alike.

In a world where economic conditions can shift rapidly, the prime rate acts as a compass, guiding lenders and borrowers through the ebb and flow of interest rate environments. Its movements signal broader economic trends – whether the central bank is tightening policy to combat inflation or loosening it to stimulate growth. For anyone managing debt, contemplating a major purchase, or looking to optimize their savings, a clear grasp of the prime rate’s definition, its determinants, and its far-reaching implications is not just beneficial, but critical.

This comprehensive guide will unpack the intricacies of the prime rate, explain its relationship with central bank policy, illustrate its tangible effects on your financial life, and provide a framework for tracking its movements to empower your decision-making. While the exact number for “today” varies dynamically and can be found via real-time financial news sources, this article will equip you with the knowledge to understand its current context and future implications.

The Prime Rate Unpacked: Definition and Determinants

To truly grasp the significance of the prime rate, one must first understand its fundamental definition and the primary forces that shape its value. It’s more than just a number; it’s a reflection of economic policy and market conditions.

What Exactly is the Prime Rate?

At its core, the prime rate is the interest rate that commercial banks charge their most creditworthy corporate customers. It serves as a benchmark for myriad other variable-rate loans. While individual banks may adjust their internal lending rates based on a customer’s specific credit risk and the type of loan, the prime rate provides a universal floor and a common reference point for these adjustments. For instance, a bank might offer a credit card with an interest rate of “prime rate plus 8%,” meaning the actual rate you pay fluctuates directly with the prime rate.

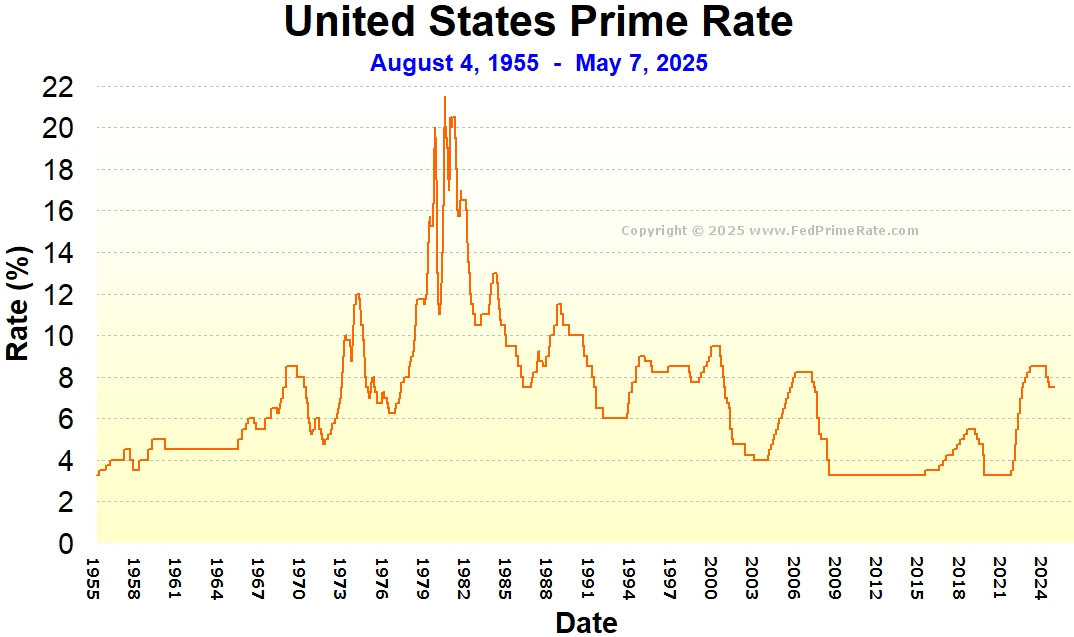

Historically, the prime rate has been incredibly stable in its relationship to the benchmark set by the Federal Reserve, almost invariably following suit within a day or two of any Fed policy change. This consistency makes it a reliable indicator of the overall cost of borrowing in the economy.

The Federal Funds Rate: The Prime Rate’s Closest Companion

The single most influential factor in determining the prime rate is the Federal Funds Rate. This is the target interest rate set by the Federal Open Market Committee (FOMC) of the U.S. Federal Reserve. The Federal Funds Rate is the rate at which banks lend their excess reserves to other banks overnight. It’s not a rate that consumers directly pay, but its target range is the primary tool the Fed uses to implement monetary policy and influence broader interest rates throughout the economy.

The connection between the Federal Funds Rate and the prime rate is remarkably direct and consistent: the prime rate is almost always set at 300 basis points (or 3 percentage points) above the upper bound of the Federal Funds Rate target range. For example, if the Fed targets a Federal Funds Rate range of 5.25% to 5.50%, the prime rate will typically be 8.50%. This predictable spread makes it relatively easy to anticipate changes to the prime rate once the Fed announces its monetary policy decisions.

The Fed uses the Federal Funds Rate to manage economic activity. If inflation is high and the economy is “overheating,” the Fed will raise the Federal Funds Rate, making it more expensive for banks to borrow from each other. This increased cost trickles down, causing banks to raise their prime rate, subsequently making all forms of borrowing more expensive for consumers and businesses. Conversely, in times of economic slowdown or recession, the Fed might lower the Federal Funds Rate to encourage borrowing and stimulate growth.

Beyond the Fed: Other Influences on Lending Decisions

While the Federal Funds Rate is the dominant factor, other elements can subtly influence a bank’s ultimate lending decisions, though typically not the publicly quoted prime rate itself. These include:

- Bank-Specific Costs: Each bank has its own operational costs, overhead, and profit margins.

- Credit Risk Assessment: For individual loans, a bank assesses the borrower’s creditworthiness. While the prime rate is for “most creditworthy” customers, an individual with a lower credit score will be offered a rate that is “prime rate plus” a higher spread to account for increased risk.

- Market Competition: The competitive landscape among banks can also play a role, as institutions strive to attract customers through favorable rates, even if their prime rate remains standard.

- Economic Outlook: Banks might adjust their internal lending policies based on their own assessment of future economic conditions and potential loan defaults.

However, it’s crucial to reiterate that these factors primarily influence the spread above the prime rate that an individual borrower pays, rather than the published prime rate itself, which remains remarkably tethered to the Federal Funds Rate.

The Ripple Effect: How the Prime Rate Impacts Your Loans and Debts

The prime rate isn’t an abstract economic indicator; its fluctuations have tangible, immediate effects on the cost of borrowing for millions of individuals and businesses. Understanding these impacts is key to effective debt management and financial planning.

Variable-Rate Borrowing: The Direct Connection

The most direct and immediate impact of a changing prime rate is felt by those with variable-rate loans. These are loans where the interest rate is not fixed for the entire term but instead adjusts periodically based on an underlying benchmark, often the prime rate itself.

- Home Equity Lines of Credit (HELOCs): Perhaps one of the most common prime-rate-linked products, HELOCs typically have interest rates expressed as “prime rate plus a margin” (e.g., prime + 0.50%). If the prime rate goes up, your monthly interest payment on your HELOC balance will increase, and vice versa.

- Adjustable-Rate Mortgages (ARMs): While many ARMs are tied to other indices like the Secured Overnight Financing Rate (SOFR) or the London Interbank Offered Rate (LIBOR-replacement rates), some older ARMs or specific products may still reference the prime rate. For these, your interest rate adjusts after an initial fixed period, and subsequent adjustments would follow the prime rate.

- Credit Cards: Many credit card annual percentage rates (APRs) are explicitly tied to the prime rate, often expressed as “prime rate plus a margin” (e.g., prime + 10%). If you carry a balance, an increase in the prime rate will directly translate to higher interest charges on your monthly statement.

- Small Business Loans and Lines of Credit: For many small and medium-sized businesses, lines of credit or certain term loans are structured with variable rates tied to the prime rate. Rising prime rates increase their operating costs, potentially impacting profitability and expansion plans.

For borrowers with these products, it’s essential to monitor prime rate movements. A rising prime rate means higher monthly payments and a greater overall cost of borrowing, while a falling prime rate offers the welcome relief of reduced payments.

Indirect Influence on Fixed-Rate Products

Even loans with fixed interest rates are indirectly influenced by the prime rate and the broader monetary policy it reflects. While your 30-year fixed-rate mortgage won’t directly change when the prime rate moves, the current rates offered for new fixed-rate loans are very much shaped by the same economic forces.

For example, when the Federal Reserve raises the Federal Funds Rate, signaling a commitment to higher interest rates to combat inflation, the yields on longer-term bonds (like the 10-year Treasury bond, which often influences fixed mortgage rates) also tend to rise. This is because investors demand higher returns for locking up their money for longer periods in an environment of rising rates. Therefore, while your existing fixed-rate mortgage is safe, the cost of new fixed-rate mortgages, auto loans, and personal loans will likely increase in step with prime rate hikes.

Debt Management Strategies in a Dynamic Rate Environment

Understanding the prime rate’s impact empowers borrowers to make strategic decisions:

- When Rates Are Rising:

- Prioritize Variable-Rate Debt: Focus on paying down high-interest credit card balances and HELOCs aggressively to minimize the impact of rising rates.

- Consider Refinancing to Fixed: If you have a significant variable-rate loan (like a HELOC or ARM) and rates are expected to continue rising, it might be wise to explore refinancing into a fixed-rate loan to lock in a predictable payment.

- Consolidate Debt: Consolidating high-interest, variable-rate debts into a lower-interest fixed-rate personal loan (if available and advantageous) can provide stability.

- When Rates Are Falling:

- Evaluate Refinancing Opportunities: This is often an opportune time to refinance existing fixed-rate debt (like a mortgage) to a lower rate, potentially saving tens of thousands over the life of the loan.

- Consider New Borrowing: If you were planning a major purchase or investment that requires a loan, falling rates can make borrowing more affordable.

Proactive monitoring and strategic adjustments to your debt portfolio are crucial in navigating interest rate cycles effectively.

More Than Just Debt: The Prime Rate’s Broader Economic Footprint

The prime rate’s influence extends far beyond individual loan products, casting a wide shadow over savings, business finance, and the overall trajectory of the economy. It acts as a barometer of the financial climate, signaling shifts that affect almost everyone.

Impact on Savings and Investments

While borrowers often dread rising interest rates, savers and some investors welcome them.

- Savings Accounts and Certificates of Deposit (CDs): When the prime rate (and by extension, the Federal Funds Rate) rises, banks are able to earn more on their reserves. This typically translates to higher interest rates offered on savings accounts, money market accounts, and Certificates of Deposit (CDs). For individuals building an emergency fund or saving for a short-term goal, a rising-rate environment can lead to greater returns on their cash.

- Bond Markets: The prime rate is closely watched by bond investors. When the Federal Reserve raises rates, newly issued bonds generally offer higher yields to remain competitive. This can cause the value of existing bonds (which have lower, fixed coupon rates) to fall, as they become less attractive compared to newer, higher-yielding alternatives. Conversely, falling rates make existing bonds more attractive, potentially increasing their market value.

- Stock Market: The relationship between interest rates and the stock market is complex. Higher interest rates can make borrowing more expensive for companies, potentially slowing their growth and reducing corporate profits. They also make “risk-free” investments like government bonds more attractive, drawing capital away from riskier assets like stocks. Conversely, lower rates can stimulate economic growth and corporate earnings, often boosting stock market performance. However, there are many other factors at play, and the stock market’s reaction is not always straightforward.

Business Finance and Economic Growth

For businesses, especially small and medium-sized enterprises (SMEs), the prime rate is a critical factor in their financial planning and operational costs.

- Cost of Capital: Businesses frequently rely on lines of credit or term loans tied to the prime rate for working capital, equipment purchases, or expansion projects. A higher prime rate directly increases their cost of capital, potentially reducing profit margins and making new investments less attractive. This can lead to slower growth, reduced hiring, and deferred expansion plans.

- Consumer Spending: When borrowing costs for consumers rise (due to higher prime rates on credit cards, auto loans, and mortgages), disposable income can shrink, and consumers may become more cautious about making large purchases. A slowdown in consumer spending can ripple through the economy, affecting businesses across various sectors.

- Investment Decisions: Companies make investment decisions based on expected returns versus the cost of financing. If the prime rate makes borrowing too expensive, fewer projects will meet the hurdle rate for investment, leading to less capital expenditure and potentially slower economic growth.

Signaling Economic Health

The Federal Reserve’s decisions regarding the Federal Funds Rate (and thus the prime rate) are not arbitrary; they are a deliberate response to prevailing economic conditions.

- Inflation Control: When inflation is high, the Fed typically raises rates to cool down the economy by making borrowing and spending more expensive. A rising prime rate signals the Fed’s commitment to bringing inflation under control.

- Employment and Growth: Conversely, if unemployment is high and economic growth is sluggish, the Fed might lower rates to stimulate borrowing, investment, and job creation. A falling prime rate signals a desire for economic expansion.

- Market Confidence: The Fed’s actions also influence market confidence. A clear and consistent monetary policy provides stability, while uncertainty or unexpected moves can create volatility. By monitoring the prime rate, individuals and businesses can gain insight into the central bank’s assessment of the economy’s current health and its future trajectory.

In essence, the prime rate serves as a key indicator of the broader economic environment, influencing not just the cost of money but also the decisions of savers, investors, and businesses, thereby shaping the overall pace and direction of economic activity.

Tracking the Prime Rate: Staying Informed and Prepared

Given its pervasive influence, knowing where to find the current prime rate and understanding how to interpret central bank communications is crucial for effective financial management. While I cannot provide real-time data, I can guide you on how to stay informed.

Where to Find the Current Prime Rate

The prime rate is a widely published financial metric, and several reliable sources update it almost immediately after any Federal Reserve policy change.

- Major Financial News Outlets: Reputable financial news websites like The Wall Street Journal, Bloomberg, Reuters, and CNBC consistently report the current prime rate. They often have dedicated sections for interest rates and Fed announcements.

- Bank Websites: Most major commercial banks (e.g., JPMorgan Chase, Bank of America, Wells Fargo) will list their current prime rate on their corporate websites, typically in sections related to interest rates or investor relations. Since banks universally adopt the same prime rate, checking one major bank’s site is usually sufficient.

- Financial Data Providers: Services like FRED (Federal Reserve Economic Data) by the Federal Reserve Bank of St. Louis, or sites like Bankrate.com, also track and publish the historical and current prime rate.

When looking for the “current prime rate today,” ensure you’re checking a source that updates regularly, especially around Federal Open Market Committee (FOMC) meeting dates, as this is when changes are most likely to occur.

Interpreting Federal Reserve Announcements

Since the prime rate is directly tied to the Federal Funds Rate, understanding the Federal Reserve’s announcements is paramount.

- FOMC Meetings: The FOMC meets eight times a year on a scheduled basis, with additional unscheduled meetings possible. Following each meeting, the FOMC releases a statement announcing any changes to the Federal Funds Rate target range. This statement is the primary driver of prime rate adjustments.

- Press Conferences: The Fed Chair typically holds a press conference after certain FOMC meetings (usually four times a year). These conferences offer further insights into the Fed’s rationale for its decisions, its economic outlook, and potential future policy direction. Pay attention to language regarding inflation, employment, and future “dot plots” (projections of future interest rates by FOMC members).

- Economic Projections: Alongside some FOMC meetings, the Fed releases its Summary of Economic Projections (SEP), which includes forecasts for GDP growth, inflation, unemployment, and the Federal Funds Rate. These projections can provide clues about the Fed’s longer-term thinking.

By following these announcements, you can anticipate changes to the prime rate and understand the economic context driving those changes. For instance, if the Fed signals a “hawkish” stance (a bias towards higher rates to fight inflation), you can expect the prime rate to rise or remain elevated. Conversely, a “dovish” stance (a bias towards lower rates to stimulate growth) might suggest stability or future declines.

Proactive Financial Planning

Staying informed about the prime rate isn’t just about curiosity; it’s about enabling proactive financial planning.

- Regular Review of Debt and Savings: Periodically review your loans (especially variable-rate ones) and savings accounts. Are your credit card rates tracking the prime rate as expected? Are your savings accounts offering competitive rates in a rising-rate environment?

- Budgeting for Rate Changes: If you have significant variable-rate debt, consider how a 0.25% or 0.50% increase in the prime rate would affect your monthly payments. Factor these potential changes into your budget.

- Consulting Financial Advisors: For complex financial situations or significant debt, consulting a financial advisor can provide personalized strategies for managing interest rate risk and optimizing your financial portfolio.

- Seizing Opportunities: Just as rising rates demand caution, falling rates present opportunities. Be prepared to act on refinancing options or new investment strategies when conditions become favorable.

In an ever-evolving economic landscape, a proactive approach to understanding and reacting to prime rate movements is a hallmark of sound financial stewardship, allowing you to optimize your borrowing costs and maximize your savings returns.

A Glimpse into the Present and Future Outlook

While providing the exact “current prime rate today” is beyond the scope of this article due to the dynamic nature of real-time data, we can discuss the context surrounding its recent trajectory and potential future movements. Readers should always check a reliable financial news source for the most up-to-the-minute figure.

Understanding Today’s Prime Rate Context

In recent times, particularly following periods of elevated inflation, central banks globally, including the U.S. Federal Reserve, embarked on a series of significant interest rate hikes. This aggressive monetary tightening was aimed squarely at cooling down the economy and bringing inflation back towards their target levels. As a direct consequence of these Fed actions, the Federal Funds Rate target range reached levels not seen in over two decades, which in turn pushed the prime rate correspondingly high.

Therefore, if you look up the prime rate today, you will likely find it in a range reflective of a restrictive monetary policy environment. For example, if the Federal Funds Rate’s upper bound is currently at 5.50%, the prime rate would be 8.50%. This elevated prime rate signifies a higher cost of borrowing across the board compared to the decade leading up to 2022. This environment means:

- Borrowers face higher interest expenses: Servicing variable-rate debt, or taking on new loans, is more expensive.

- Savers can earn more: High-yield savings accounts and Certificates of Deposit offer more attractive returns.

- Businesses face increased financing costs: This can temper investment and expansion plans.

This context underscores the Fed’s commitment to price stability, even if it comes with the trade-off of potentially slower economic growth.

The Road Ahead: Potential Scenarios for Interest Rates

Looking forward, the future path of the prime rate hinges primarily on the Federal Reserve’s assessment of inflation, employment, and overall economic activity. Economic projections and market sentiment continuously evolve, but several key themes generally dominate the discussion:

- Inflation Trajectory: The primary determinant of future rate decisions will be the sustained trajectory of inflation. If inflation continues to decelerate towards the Fed’s 2% target, it would create room for the Fed to consider lowering the Federal Funds Rate, and thus the prime rate.

- Economic Growth and Employment: The Fed also monitors economic growth and the labor market closely. A strong and resilient labor market might allow the Fed to maintain higher rates for longer, even if inflation is moderating. Conversely, signs of significant economic weakening or rising unemployment could prompt the Fed to cut rates sooner to avoid a severe recession.

- “Higher for Longer” vs. Rate Cuts: Debates among economists and market participants often center on whether the Fed will maintain a “higher for longer” stance to ensure inflation is fully vanquished, or if they will begin a cycle of rate cuts in the near future. These expectations significantly influence market sentiment and long-term interest rates.

- Potential for Volatility: Geopolitical events, supply chain disruptions, or unexpected shifts in consumer behavior could always introduce new variables, leading to potential shifts in the Fed’s outlook and, consequently, the prime rate.

Ultimately, the future path of the prime rate is not set in stone. It will be a dynamic response to incoming economic data and the Fed’s evolving assessment of the balance between inflation control and supporting economic growth. Staying tuned to central bank communications and major economic indicators will be crucial for understanding where rates are headed next.

Conclusion

The prime rate is far more than an obscure financial figure; it is a dynamic and powerful force that directly shapes the financial landscape for every individual and business. As the benchmark for a multitude of loans and a critical indicator of broader economic conditions, its movements reflect the intricate dance between central bank policy, inflation, and economic growth.

By understanding what the prime rate is, how it’s inextricably linked to the Federal Funds Rate, and its pervasive impact on everything from your credit card bills to the returns on your savings, you equip yourself with invaluable knowledge. In an era of potentially fluctuating interest rates, an informed approach to financial planning, coupled with diligent monitoring of economic news and central bank announcements, empowers you to make strategic decisions. Whether you are seeking to minimize borrowing costs, maximize savings returns, or simply navigate the economic currents, the prime rate serves as an essential guidepost on your financial journey. Stay informed, stay prepared, and take proactive steps to align your financial choices with the evolving interest rate environment.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.