Understanding current mortgage rates is paramount for anyone navigating the intricate world of homeownership, whether you’re a first-time buyer, looking to refinance, or considering an investment property. These rates, essentially the cost of borrowing money to purchase real estate, are not static; they are dynamic, influenced by a complex interplay of economic forces, central bank policies, and global events. A slight shift in mortgage rates can significantly impact your monthly payments, the total interest paid over the life of the loan, and ultimately, your financial well-being. This guide aims to demystify mortgage rates, providing a clear, insightful, and engaging overview of how they work, what influences them, and how you can position yourself to secure the most favorable terms in today’s market.

Understanding the Dynamics of Mortgage Rates

Mortgage rates don’t just appear out of thin air; they are a direct reflection of broader economic conditions and specific financial market signals. Grasping these underlying dynamics is the first step toward becoming an informed borrower.

Key Factors Influencing Mortgage Rates

Several powerful forces collectively shape the direction and magnitude of mortgage rates. Understanding these can help you anticipate market shifts and make timely decisions.

- Federal Reserve Policy: While the Federal Reserve doesn’t directly set mortgage rates, its actions profoundly impact them. The Fed’s primary tool, the federal funds rate, influences short-term interest rates, which in turn affect the cost of borrowing for banks. When the Fed raises this rate to combat inflation, it typically leads to higher mortgage rates. Conversely, a reduction might stimulate economic activity and lower rates. Additionally, the Fed’s bond-buying or selling programs (quantitative easing/tightening) directly influence long-term rates, including those for mortgages.

- Inflation: This is arguably the most significant driver. When inflation is high or expected to rise, lenders demand higher interest rates to compensate for the eroded purchasing power of future repayments. The fear of inflation often sends bond yields – to which mortgage rates are closely tied – upward.

- Economic Growth and Employment Data: A robust economy with strong job growth generally indicates higher inflation potential and increased demand for credit, pushing rates up. Conversely, signs of economic slowdown or recession often lead to lower rates as investors seek the safety of bonds, driving their prices up and yields down.

- The Bond Market (Specifically 10-Year Treasury Yields): Mortgage rates are primarily linked to the yield on the 10-year U.S. Treasury bond. When investors buy Treasury bonds, their prices rise, and yields fall, often bringing mortgage rates down. When investors sell bonds, yields rise, and mortgage rates tend to follow suit. This correlation is a crucial indicator for tracking mortgage rate movements.

- Housing Market Conditions: High demand for homes coupled with limited supply can put upward pressure on rates, as lenders may see more risk or opportunity. Conversely, a sluggish housing market might lead lenders to offer more competitive rates to attract borrowers.

- Geopolitical Events: Global instability, conflicts, or significant international policy changes can lead to investor uncertainty. Often, this drives investors towards “safe haven” assets like U.S. Treasury bonds, which can temporarily push their yields down and, consequently, mortgage rates.

The Difference Between Fixed-Rate and Adjustable-Rate Mortgages (ARMs)

The choice between a fixed-rate and an adjustable-rate mortgage is fundamental, impacting your financial predictability and risk exposure.

- Fixed-Rate Mortgages: As the name suggests, the interest rate on a fixed-rate mortgage remains the same for the entire life of the loan, typically 15 or 30 years. This offers unparalleled stability and predictability, allowing you to budget precisely for your monthly principal and interest payments. Fixed-rate loans are ideal for borrowers seeking long-term certainty, especially when rates are low.

- Adjustable-Rate Mortgages (ARMs): ARMs typically offer a lower initial interest rate for a fixed period (e.g., 3, 5, 7, or 10 years). After this initial period, the rate adjusts periodically (e.g., annually) based on a specified market index plus a margin set by the lender. ARMs come with caps that limit how much the interest rate can increase or decrease per adjustment period and over the life of the loan. They can be attractive for borrowers who plan to sell or refinance before the fixed period ends, or for those who anticipate their income will rise significantly, making future payment increases manageable.

How Lenders Determine Your Specific Rate

While market forces establish baseline rates, your individual financial profile plays a critical role in the rate a lender offers you.

- Credit Score: A higher credit score (generally 740 and above) signals to lenders that you are a reliable borrower, often qualifying you for the lowest available rates. A lower score indicates higher risk, resulting in a higher interest rate.

- Debt-to-Income (DTI) Ratio: This ratio compares your total monthly debt payments to your gross monthly income. A lower DTI (ideally under 43%) demonstrates your ability to manage debt, making you a less risky borrower.

- Loan-to-Value (LTV) Ratio (Down Payment): The LTV compares the amount of your mortgage to the appraised value of the home. A larger down payment results in a lower LTV, signifying more equity upfront and less risk for the lender, which can translate into a better rate.

- Loan Term: Shorter loan terms (e.g., 15-year mortgages) typically come with lower interest rates than longer terms (e.g., 30-year mortgages). Lenders view shorter terms as less risky because their money is tied up for a shorter period.

- Loan Type: Different mortgage programs (Conventional, FHA, VA, USDA) have varying risk profiles and, consequently, different rate structures and eligibility requirements.

- Points: Borrowers can sometimes “buy down” their interest rate by paying discount points at closing. One point equals 1% of the loan amount. While this increases upfront costs, it can significantly reduce interest payments over the life of the loan.

Navigating the Current Mortgage Rate Landscape

Staying informed about current rates and their trends is crucial for making strategic decisions in the housing market. Knowledge empowers you to act decisively.

Where to Find Real-Time Rate Information

Access to accurate, up-to-date rate information is essential for comparison shopping.

- Online Lenders and Brokers: Most major online mortgage lenders and brokers provide daily rate updates on their websites, often allowing you to get personalized quotes without impacting your credit score.

- Traditional Banks and Credit Unions: Local banks and credit unions also publish their current rates, though these may be less frequently updated than online aggregators.

- Financial News Outlets and Data Providers: Reputable financial news sources (e.g., The Wall Street Journal, Bloomberg) and dedicated mortgage data providers (e.g., Freddie Mac’s Primary Mortgage Market Survey, Fannie Mae) offer reliable historical and current rate averages.

- Mortgage Rate Comparison Sites: Websites like Bankrate, Zillow Mortgages, and LendingTree allow you to compare rates from multiple lenders simultaneously by entering a few key pieces of information. This is an efficient way to survey the market.

Understanding Rate Trends and Forecasts

While current rates are a snapshot, understanding trends and forecasts provides context for future planning.

- Why Forecasts Are Educated Guesses: Mortgage rate forecasts are based on economic models and expert analysis, but they are not guarantees. Unexpected geopolitical events, sudden shifts in inflation, or unforeseen central bank actions can quickly alter predictions. Treat forecasts as indicators, not certainties.

- Importance of Staying Informed: Regularly monitoring economic news, particularly reports on inflation, employment, and central bank commentary, can provide clues about the likely direction of rates. This helps you gauge whether the market is entering a period of rising or falling rates.

- Impact on Short-Term vs. Long-Term Trends: Short-term fluctuations are common and often reactive to daily news. Long-term trends are driven by more fundamental economic shifts, such as sustained inflation or significant changes in monetary policy.

The Impact of Mortgage Rates on Affordability

Even small changes in interest rates can have a profound effect on your financial capacity to buy a home.

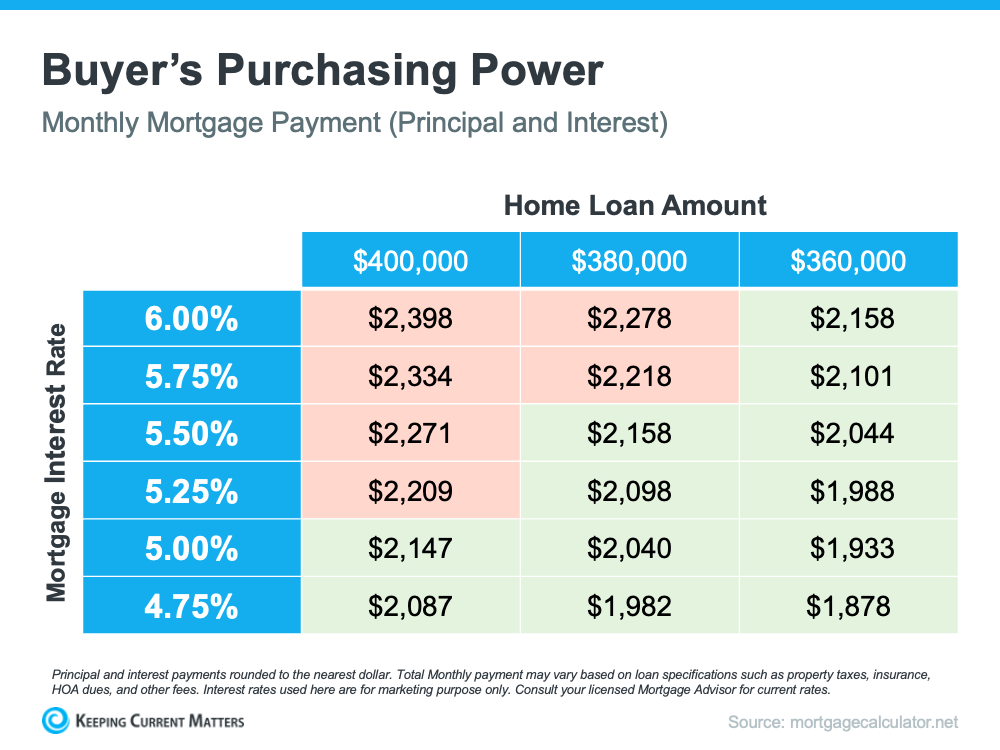

- Monthly Payment Calculation: A higher interest rate means a larger portion of your monthly payment goes towards interest, reducing the amount that applies to your principal. For example, on a $300,000 30-year fixed-rate mortgage, moving from 6.0% to 7.0% can increase your monthly payment by over $180.

- Total Interest Paid Over Loan Term: Over 30 years, that seemingly small difference in monthly payments adds up significantly. The difference between 6.0% and 7.0% on a $300,000 loan equates to paying roughly an additional $65,000 in interest over the life of the loan.

- Buying Power Adjustments: Higher rates reduce your purchasing power. If your budget dictates a specific monthly payment, rising rates mean you can afford a smaller loan amount, effectively limiting the price range of homes you can consider.

Strategies for Securing the Best Mortgage Rate

Knowing the factors and landscape is one thing; proactively taking steps to secure the best rate for your situation is another.

Improving Your Financial Profile

Before you even start shopping for a loan, optimize your financial health.

- Boosting Your Credit Score: Pay bills on time, reduce credit card balances, dispute errors on your credit report, and avoid opening new lines of credit before applying for a mortgage. A higher score directly translates to lower rates.

- Reducing Debt: A lower DTI ratio makes you more attractive to lenders. Prioritize paying down high-interest debt, especially credit cards and personal loans.

- Increasing Your Down Payment: Aim for at least 20% to avoid private mortgage insurance (PMI) and to secure a lower LTV, which can improve your rate. Even an extra few percentage points can make a difference.

- Building Savings Reserves: Lenders look favorably on borrowers with a healthy emergency fund, demonstrating financial stability beyond just the down payment.

Shopping Around and Comparing Offers

This is perhaps the most impactful step in securing a favorable rate.

- Getting Multiple Quotes: Don’t settle for the first offer. Contact at least 3-5 different lenders – including national banks, local credit unions, and online lenders – to compare their rates and terms.

- Understanding the Loan Estimate Document: Lenders are required to provide a standardized Loan Estimate form within three business days of application. This document outlines your estimated interest rate, monthly payment, and closing costs. Compare these forms carefully.

- Comparing APR vs. Interest Rate: The interest rate is the cost of borrowing the principal. The Annual Percentage Rate (APR) includes the interest rate plus other fees and charges (like origination fees and discount points) expressed as an annual percentage. APR gives a more accurate overall cost of the loan for comparison purposes.

When to Lock Your Rate

Timing your rate lock can save you money or prevent disappointment.

- Benefits of Locking a Rate: Once you lock your rate, it’s guaranteed for a specific period (typically 30 to 60 days), protecting you from market fluctuations if rates rise before your closing.

- When It’s Advisable: If rates appear to be on an upward trend, or if you’re nearing your closing date and want certainty, locking your rate is generally a good idea. In a stable or falling rate environment, you might wait, but this involves more risk.

- Lock-in Periods and Extensions: Be aware of the length of your rate lock. If your closing is delayed beyond this period, you may need to pay a fee for an extension, or risk having your rate adjusted to current market levels.

Considering Refinancing Opportunities

For existing homeowners, current rates present an ongoing opportunity for optimization.

- When Do Lower Rates Make Refinancing Appealing? If current rates are significantly lower than your existing mortgage rate (e.g., a drop of 0.75% to 1.0% or more), refinancing could reduce your monthly payments or the total interest paid.

- Types of Refinancing:

- Rate-and-Term Refinance: Changes your interest rate, loan term, or both, but you don’t take cash out.

- Cash-Out Refinance: Allows you to borrow more than you owe on your current mortgage and receive the difference in cash, often used for home improvements or debt consolidation.

- Costs Associated with Refinancing: Be mindful of closing costs (appraisal fees, origination fees, title insurance, etc.), which can total 2% to 5% of the loan amount. Calculate the break-even point to ensure the savings outweigh the costs within your expected time in the home.

The Future Outlook for Mortgage Rates

While no one has a crystal ball, understanding the prevailing economic sentiment and expert predictions can help frame your financial planning.

Expert Predictions and Economic Indicators

The consensus among economists offers a general direction, but always with caveats.

- What Are Economists Generally Saying? Many economists often project that mortgage rates will remain sensitive to inflation data and the Federal Reserve’s actions. Periods of high inflation could see rates remain elevated or even rise, while a stable or declining inflationary environment might allow for modest rate decreases. However, the path is rarely linear, and predictions frequently adjust based on new data.

- Influence of Inflation and Fed Actions: If inflation proves persistent, the Fed may maintain a restrictive monetary policy, keeping upward pressure on rates. Conversely, if inflation cools more rapidly than expected, the Fed might ease its stance, potentially allowing rates to soften.

- Potential Scenarios: We could see scenarios ranging from rates stabilizing within a certain range, to modest dips as inflation is brought under control, or even gradual increases if economic growth accelerates unexpectedly. The overarching theme is often one of continued volatility in response to economic data.

Long-Term Financial Planning with Mortgage Rates in Mind

Regardless of short-term fluctuations, strategic long-term planning is key.

- Stress Testing Your Budget: When considering a mortgage, especially an ARM, ensure your budget can comfortably absorb potential future rate increases. Don’t stretch yourself too thin with the initial low payment.

- Considering Future Rate Changes for ARMs: If you opt for an ARM, have a plan for when the fixed period ends. Will you be in a position to refinance into a fixed-rate loan, or will your income support higher payments?

- The Long-Term Value of Homeownership: While current rates are important, remember that homeownership is often a long-term investment. Building equity, potential appreciation, and the stability of having a permanent residence are significant benefits that often outweigh temporary rate volatility.

Conclusion

Understanding “what are current mortgage rates” goes far beyond simply knowing a number; it involves a deep dive into economic indicators, personal finance, and strategic decision-making. Mortgage rates are a constantly moving target, shaped by forces as large as global economics and as personal as your credit score. By actively monitoring market trends, meticulously improving your financial profile, and diligently shopping for the best terms, you empower yourself to navigate this complex landscape with confidence. Whether you’re buying your first home, looking to move, or considering refinancing, an informed and proactive approach to current mortgage rates is your most valuable asset in securing a financial future built on solid ground. Always remember to consult with a qualified financial advisor or mortgage professional who can provide personalized guidance tailored to your unique circumstances.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.