Understanding the cost of living is the cornerstone of effective personal finance management. Whether you are planning a cross-country move, negotiating a salary, or simply trying to optimize your monthly budget, the concept of the cost of living (COL) acts as the primary lens through which you must view your purchasing power. At its core, the cost of living is the amount of money needed to cover basic expenses—such as housing, food, taxes, and healthcare—in a certain place and time.

However, for the modern investor or professional, the cost of living is more than just a survival metric; it is a strategic variable. It determines the true value of your income and dictates the lifestyle you can afford. In this guide, we will break down the components of the cost of living, how it is measured, and how you can leverage this knowledge to build a more resilient financial future.

Decoding the Components of the Cost of Living

The cost of living is not a monolithic figure. It is a composite of several economic factors that fluctuate based on geography, policy, and market demand. To manage your money effectively, you must understand the “big rocks” that constitute the majority of this metric.

Housing: The Foundation of Your Budget

For most individuals and families, housing is the single largest expenditure. This includes either rent or mortgage payments, property taxes, and homeowners’ insurance. In high-demand metropolitan areas, housing costs can consume upwards of 40% to 50% of a household’s net income. When evaluating the cost of living in a new city, the real estate market is the first indicator of financial feasibility. A high salary in San Francisco may offer less disposable income than a moderate salary in Austin, primarily due to the disparity in square-footage costs.

Essential Goods and Services: Food, Utilities, and Transport

Beyond shelter, the “basket of goods” required for daily life includes groceries, utilities (electricity, water, heating), and transportation. Transportation costs can vary wildly; in a city with robust public transit, you might avoid the expense of a car, whereas, in suburban or rural areas, fuel, maintenance, and insurance become mandatory overhead. Grocery prices are also regionally sensitive, influenced by local supply chains and state-level taxes on essential goods.

Healthcare and Education: The Variable Variables

Healthcare is a significant component of the cost of living that often goes overlooked until it becomes an emergency. This includes insurance premiums, out-of-pocket maximums, and the general price of services in a specific region. Similarly, for those with families, the cost of childcare and education (both public and private) can drastically shift the financial landscape. In some regions, high property taxes fund elite public schools, whereas, in others, private tuition becomes a necessary expense for quality education.

Measuring the Cost of Living: Indices and Metrics

Economists and financial planners use specific tools to quantify the cost of living. Understanding these metrics allows you to compare different geographic locations and track how your money’s value changes over time.

The Consumer Price Index (CPI) Explained

The Consumer Price Index (CPI) is the most widely recognized measure of inflation and the cost of living. It tracks the weighted average of prices of a basket of consumer goods and services. When the CPI rises, it indicates that the cost of living is increasing—meaning each dollar you earn has less “buying power” than it did previously. For those focused on personal finance, monitoring the CPI is essential for understanding whether your income growth is outpacing the rising costs of survival.

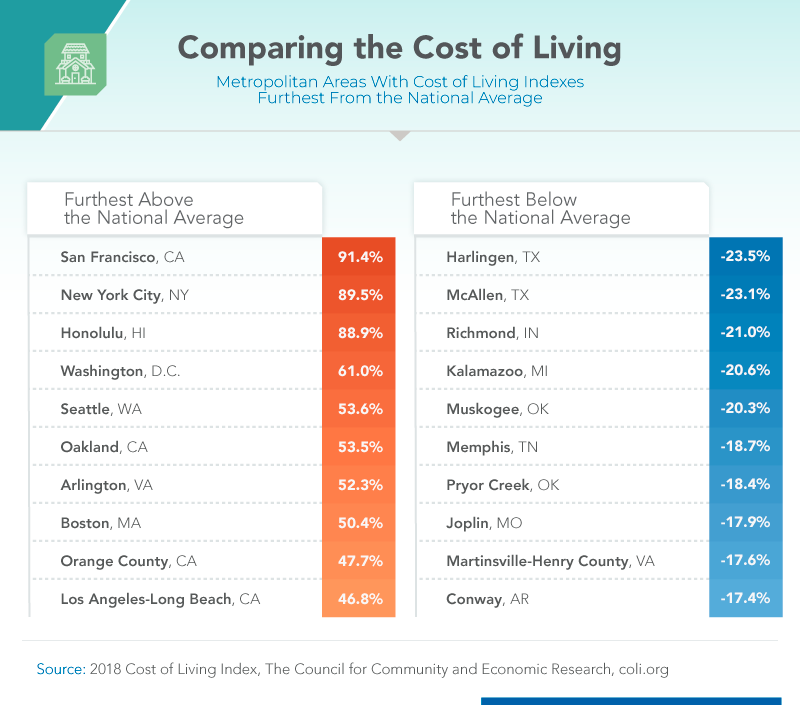

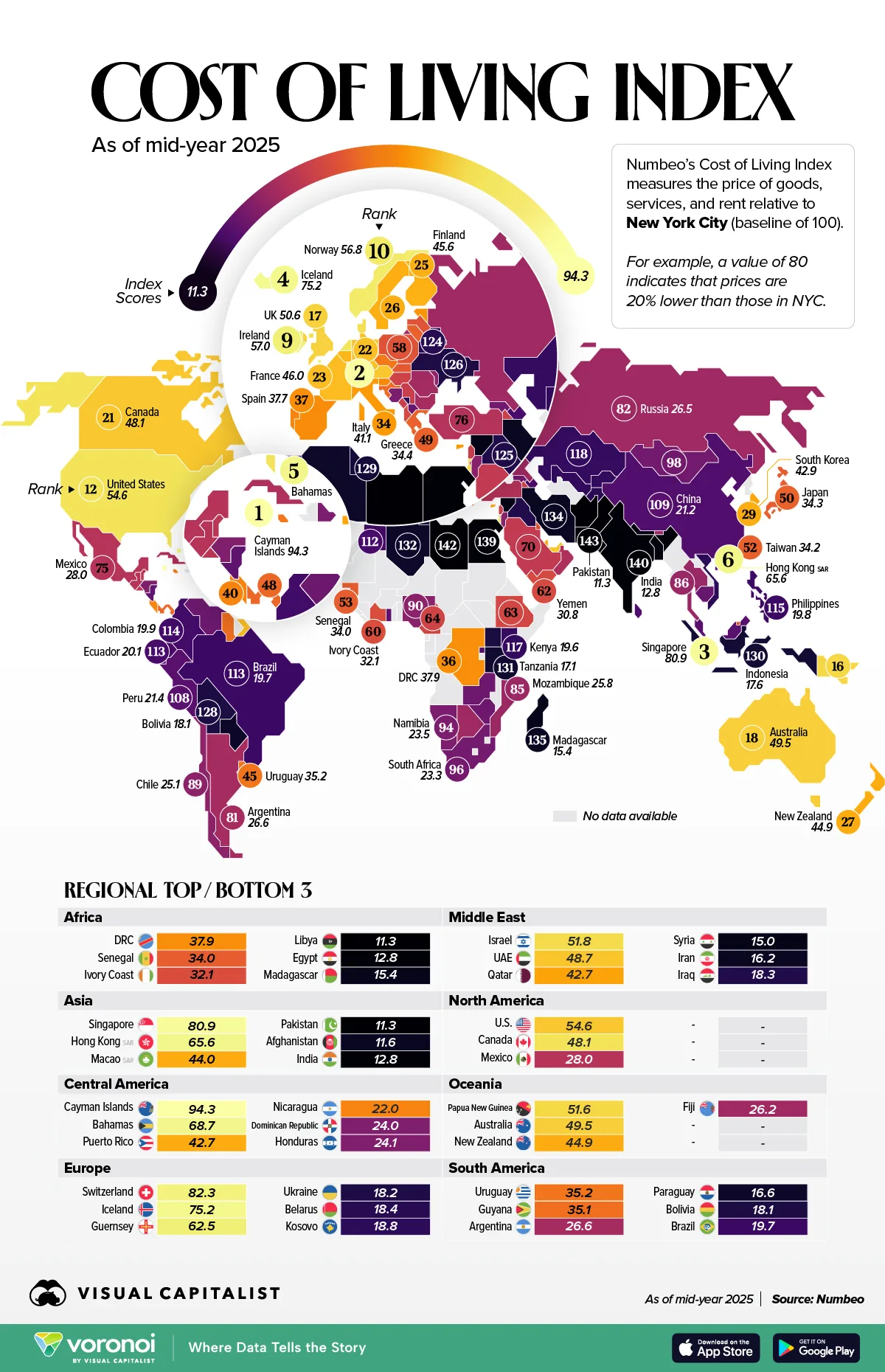

Cost of Living Indices (COLI) and Purchasing Power

While the CPI tracks changes over time, a Cost of Living Index (COLI) compares the cost of living between different locations at a single point in time. Typically, a base city (like New York or Chicago) is assigned a value of 100. If a city has an index of 120, it is 20% more expensive than the base. This is crucial for “Purchasing Power Parity.” It answers the question: “How much would I need to earn in City B to maintain the same lifestyle I have in City A?”

Regional Differences: Why Location Dictates Wealth

The “Money” niche often discusses “Geographic Arbitrage”—the practice of earning a high-level currency or salary while living in a low-cost-of-living area. The disparity in regional costs is driven by land availability, local labor laws, and state taxes. For example, states with no income tax may have a lower overall cost of living, but this is sometimes offset by higher property or sales taxes. A sophisticated financial plan accounts for these nuances rather than looking at gross income alone.

Impact on Personal Finance and Strategy

The cost of living isn’t just a static number; it is a dynamic force that should influence your career moves, investment choices, and long-term wealth-building strategies.

Inflation vs. Cost of Living: Understanding the Difference

While often used interchangeably, inflation and cost of living have a nuanced relationship. Inflation is the general rise in prices across the economy, whereas the cost of living is the actual cost an individual incurs to maintain a specific standard. If your personal “basket of goods” consists mostly of technology and travel (which may see price drops), your personal cost of living might stay flat even if national inflation is rising due to energy or food costs.

Salary Negotiation and the Geographic Arbitrage Strategy

When discussing compensation with an employer, the cost of living should be your primary leverage point. A $10,000 raise is a massive win in a low-cost area but may be completely swallowed by a move to a high-cost coastal city. The rise of remote work has popularized “Geographic Arbitrage,” where professionals maintain high-paying roles in “Tier 1” tech or finance hubs while physically residing in “Tier 3” cities. This strategy effectively supercharges your savings rate by artificially lowering your cost of living while keeping your income ceiling high.

Adjusting Your Investment Portfolio for COL Shifts

A savvy investor understands that the “real return” on an investment is the nominal return minus the cost of living increases. If your portfolio grows by 7% but the cost of living in your area increases by 5%, your actual wealth has only grown by 2%. This necessitates investing in assets that historically outpace the cost of living, such as equities, real estate, or inflation-protected securities (TIPS).

Practical Tools and Tactics for Managing Rising Costs

Knowledge of the cost of living is only valuable if it leads to action. Here are the financial frameworks used to mitigate the impact of rising costs.

Budgeting Frameworks for High-COL Areas

In expensive regions, traditional budgeting rules like the “50/30/20 rule” (50% needs, 30% wants, 20% savings) often require adjustment. In high-cost-of-living areas, your “needs” (housing) might take up 60%. To compensate, individuals must be more aggressive in the “wants” category or seek out “house hacking” opportunities—such as renting out a room—to bring their housing costs back in line with their financial goals.

Maximizing Online Income and Side Hustles to Offset Costs

When the cost of living rises faster than corporate wages, creating secondary income streams becomes a necessity rather than a luxury. The digital economy offers various “side hustles”—from freelance consulting to e-commerce—that allow you to earn in a global marketplace. Because online income isn’t usually tied to your local economy, it serves as a powerful hedge against localized cost-of-living spikes.

Long-term Financial Planning in a Changing Economy

The most successful financial planners don’t just look at today’s costs; they project future costs. If you plan to retire in twenty years, you must estimate what the cost of living will be then. Assuming a modest 3% annual increase, the cost of living will nearly double in 24 years. This realization underscores the importance of compound interest and early investing. Your goal is to build a “Money Machine” that generates enough cash flow to cover your cost of living, regardless of how high those costs may climb.

Conclusion: Mastering Your Financial Landscape

The cost of living is the most significant external factor in your personal finance journey. It determines where you live, how much you save, and when you can retire. By understanding the components that drive these costs—housing, goods, and services—and by utilizing tools like the CPI and COLI, you can make informed decisions about your career and your investments.

True financial freedom isn’t just about the number in your bank account; it’s about the relationship between that number and the cost of the life you want to lead. By strategically managing your location, negotiating your salary with cost-of-living data in hand, and investing in assets that outpace inflation, you can ensure that your purchasing power grows, providing you with security and opportunity in any economic climate.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.