In the intricate world of personal finance and investing, few concepts hold as much transformative power as compound interest. Often lauded as the “eighth wonder of the world” by Albert Einstein, its ability to generate wealth is profound yet frequently underestimated. At its core, compound interest is the interest earned not only on the initial principal but also on the accumulated interest from previous periods. This seemingly simple mechanism sets in motion a powerful exponential growth curve, allowing money to grow at an increasingly accelerated rate over time.

Understanding compound interest is not merely an academic exercise; it is a fundamental pillar upon which successful long-term financial planning is built. Whether you are saving for retirement, a down payment on a home, or your child’s education, leveraging the power of compounding can significantly alter your financial trajectory. This comprehensive guide will demystify compound interest, exploring its mechanics, illustrating its impact, and providing practical strategies to harness its full potential in your financial journey. By the end, you’ll not only grasp “what is compound interest” but also how to make it work tirelessly for you.

Understanding the Mechanics of Compound Interest

To truly appreciate the power of compound interest, one must first grasp its underlying mechanics and how it fundamentally differs from its simpler counterpart.

Simple Interest vs. Compound Interest: The Fundamental Difference

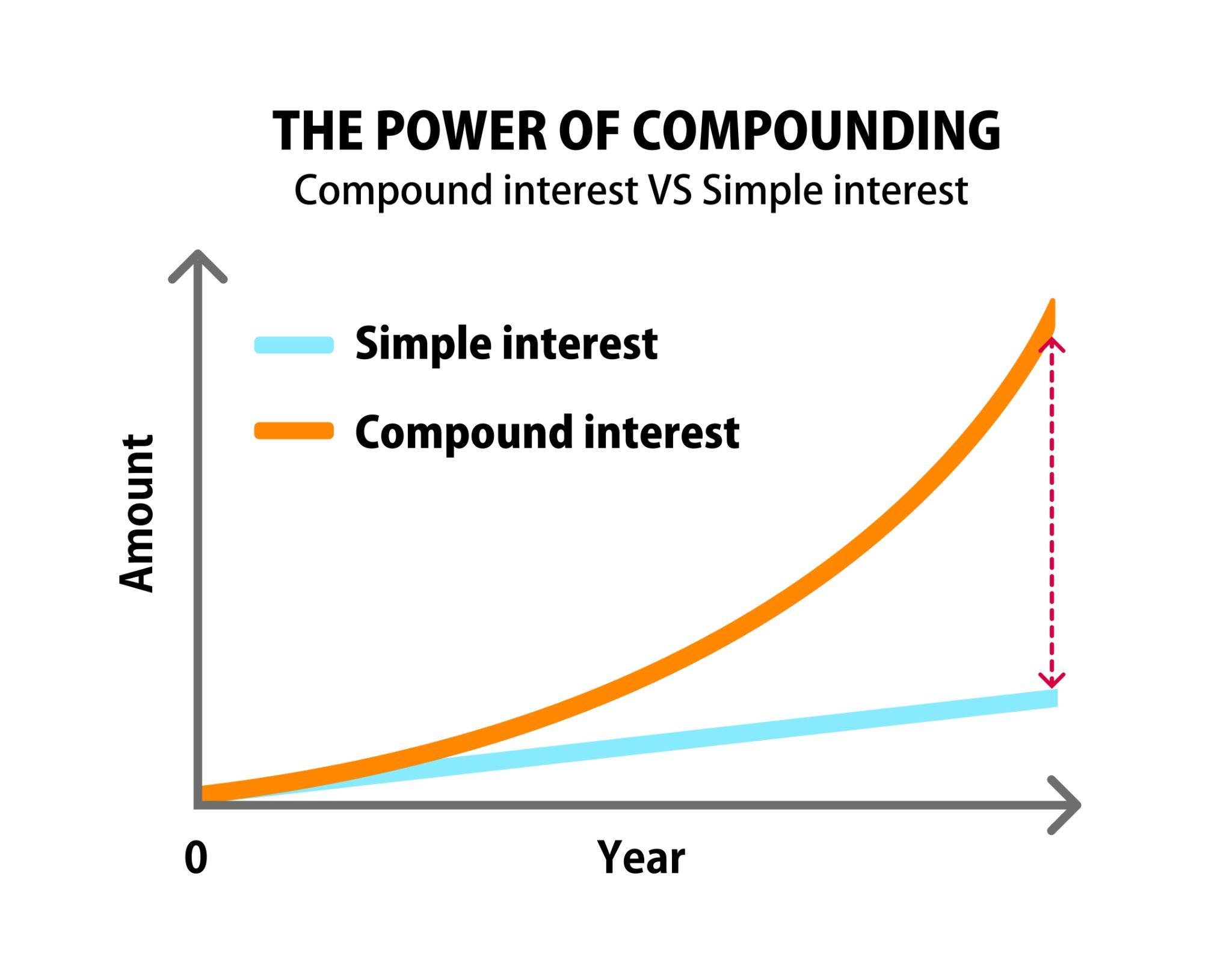

The distinction between simple and compound interest is crucial. Simple interest is calculated solely on the principal amount of a loan or deposit. If you deposit $1,000 at a 5% simple interest rate, you would earn $50 each year, regardless of how long the money is held. The interest earned never contributes to the principal for subsequent interest calculations.

Compound interest, however, operates differently. It’s calculated on the initial principal plus all the accumulated interest from previous periods. This means your interest begins earning interest itself, creating a snowball effect. Using the same example: a $1,000 deposit at a 5% compound interest rate would earn $50 in the first year. In the second year, the interest would be calculated on $1,050 (the original principal plus the first year’s interest), yielding $52.50. This incremental increase, while small initially, becomes dramatically significant over extended periods.

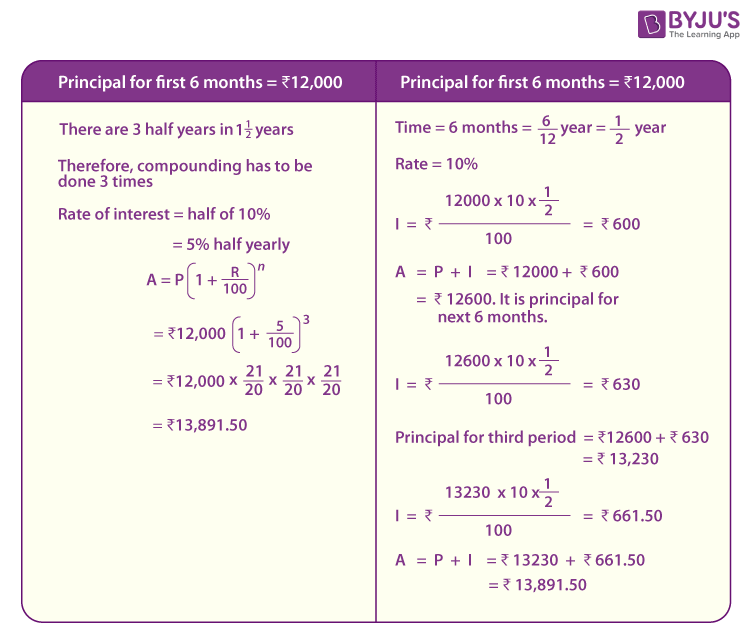

How the Calculation Works: A Step-by-Step Explanation

The formula for compound interest is:

$A = P (1 + r/n)^{nt}$

Where:

- A = the future value of the investment/loan, including interest

- P = the principal investment amount (the initial deposit or loan amount)

- r = the annual interest rate (as a decimal)

- n = the number of times that interest is compounded per year

- t = the number of years the money is invested or borrowed for

Let’s break down the components:

- Principal (P): This is your starting sum. The larger the principal, the more interest it can generate.

- Interest Rate (r): This is the percentage return your investment yields annually. A higher rate accelerates growth.

- Compounding Frequency (n): This refers to how often the interest is calculated and added to the principal. Interest can compound annually, semi-annually, quarterly, monthly, daily, or even continuously. The more frequent the compounding, the faster your money grows, because interest starts earning interest sooner. For instance, interest compounded daily will grow faster than interest compounded annually, assuming the same annual rate.

- Time (t): This is the duration your money remains invested. This is arguably the most critical factor, as compound interest thrives on time.

Consider $10,000 invested at an annual interest rate of 7% compounded annually for 10 years:

$A = 10,000 (1 + 0.07/1)^{1*10}$

$A = 10,000 (1.07)^{10}$

$A approx 10,000 * 1.96715$

$A approx $19,671.51$

After 10 years, your initial $10,000 would nearly double, with $9,671.51 earned in interest. If this were simple interest, you would only earn $700 per year ($10,000 * 0.07), totaling $7,000 over 10 years, resulting in a final amount of $17,000. The difference of $2,671.51 is purely due to the magic of compounding.

The Role of Interest Rate, Principal, and Time

Each variable plays a distinct role in the compounding equation, but their interplay is what truly unlocks significant growth.

- Higher Interest Rate: A higher interest rate means a larger percentage of your principal (and accumulated interest) is added each compounding period, leading to faster growth. Even a small difference in rates can result in a substantial difference over the long term.

- Larger Principal: Starting with a larger principal gives you a bigger base from which to generate interest. While not always feasible for everyone initially, increasing contributions over time can mimic the effect of a larger principal.

- Longer Time Horizon: Time is the ultimate accelerator for compound interest. The longer your money has to grow, the more periods interest can compound, and the more pronounced the “interest on interest” effect becomes. This is why financial advisors consistently stress the importance of starting to invest early. The earlier you begin, the less you may need to save out of your own pocket to reach your financial goals.

The Power of Compounding: A Time-Tested Strategy

The true marvel of compound interest lies in its ability to transform modest beginnings into substantial wealth over time, a phenomenon often described as the “snowball effect.”

The Snowball Effect: Compounding’s Exponential Growth

Imagine a small snowball rolling down a snowy hill. As it rolls, it picks up more snow, growing larger and gaining momentum. The larger it gets, the more snow it collects with each turn, causing it to grow even faster. This is an apt analogy for compound interest. Your initial investment is the small snowball. The interest it earns is the snow it picks up. As the interest is added to the principal, the “snowball” gets bigger, and subsequently, the amount of “snow” (new interest) it collects in the next period increases.

This exponential growth is what differentiates compound interest from linear growth. With simple interest, the growth is linear – a straight line upward. With compound interest, the growth starts slow but gradually curves upward, becoming steeper and steeper over time. The longer the duration, the more dramatic this curve becomes, demonstrating the power of time in conjunction with compounding.

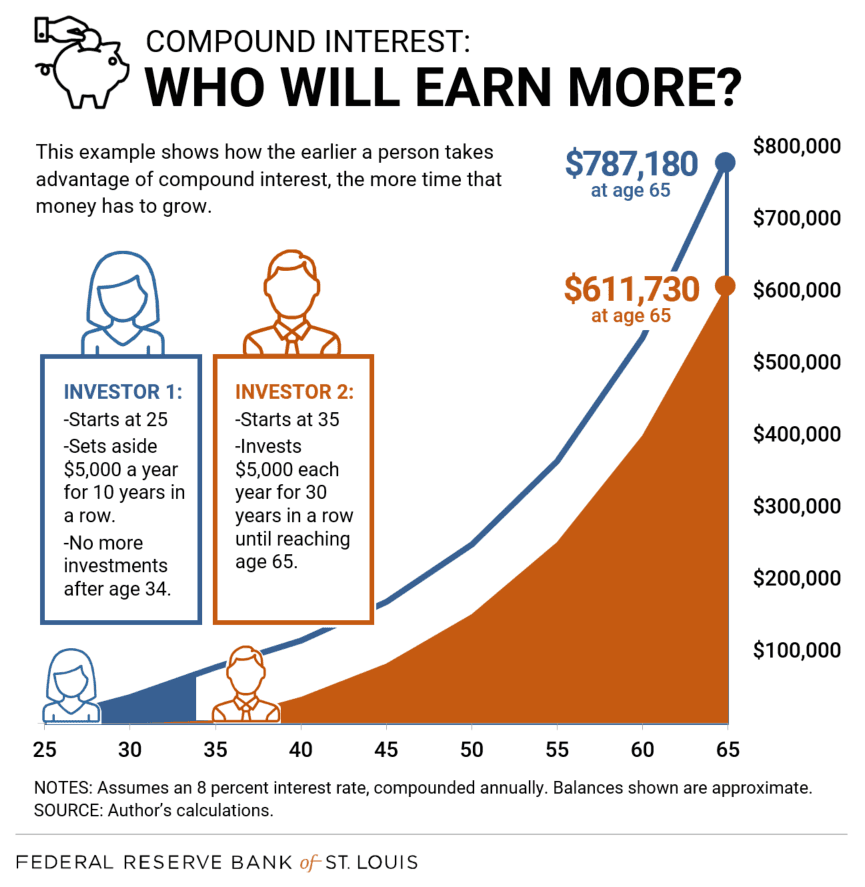

The Importance of Starting Early: Time as Your Ally

The concept of time being an investor’s greatest ally is central to maximizing compound interest. Due to the exponential nature of compounding, the earliest dollars invested have the longest time to grow, and thus contribute disproportionately to total wealth.

Consider two individuals, Alice and Ben, both investing $5,000 annually at an 8% average annual return:

- Alice: Starts at age 25 and invests for 10 years, then stops at age 35, leaving her money to grow until age 65. Total invested: $50,000.

- Ben: Starts at age 35 and invests for 30 years, until age 65. Total invested: $150,000.

Despite investing three times as much money, Ben will likely end up with significantly less than Alice. Alice’s initial $50,000 has an additional 10 years of compounding advantage. The “interest on interest” from those early years gives her a monumental head start. This scenario vividly illustrates that the power of starting early outweighs the sheer volume of later contributions for long-term growth.

Illustrative Examples: Seeing the Growth in Action

Let’s look at another example to underscore the difference over a significant period.

Suppose you invest $1,000 today at an average annual return of 10%.

- After 1 year: $1,100 (You earned $100)

- After 5 years: $1,610.51 (Total interest earned: $610.51)

- After 10 years: $2,593.74 (Total interest earned: $1,593.74)

- After 20 years: $6,727.50 (Total interest earned: $5,727.50)

- After 30 years: $17,449.40 (Total interest earned: $16,449.40)

- After 40 years: $45,259.26 (Total interest earned: $44,259.26)

Notice how the growth accelerates. It took 10 years to more than double your money, but only about 7 more years to more than double it again from year 10 to year 17 (approx. $2,593 to $5,186). The longer the horizon, the more pronounced the “J-curve” of compounding becomes, leading to truly astounding results from seemingly modest initial investments.

Compound Interest in Real-World Investing

While the theoretical calculations demonstrate its power, compound interest is not confined to textbooks. It is a fundamental principle woven into the fabric of almost every investment vehicle available today. Understanding how different investments leverage compounding is key to building a robust financial portfolio.

Savings Accounts and Certificates of Deposit (CDs)

These are perhaps the most straightforward examples of compound interest at work. When you deposit money into a savings account, the bank typically pays interest on your balance, which is then added to your principal (compounded), usually monthly or quarterly. The next interest payment is then calculated on this new, higher balance. CDs operate similarly, but you commit your money for a fixed term at a fixed interest rate, often yielding slightly higher returns than standard savings accounts. While the interest rates on these vehicles are generally low, they offer a risk-free environment to see compounding in action.

Stocks and Mutual Funds: Reinvesting Dividends

In the equity market, compound interest manifests through dividend reinvestment. Many companies distribute a portion of their profits to shareholders in the form of dividends. Instead of taking these dividends as cash, investors can choose to reinvest them to buy more shares of the same stock or mutual fund. These newly purchased shares then generate their own dividends, which can also be reinvested, creating a compounding loop. Over time, this strategy allows an investor to accumulate a significantly larger number of shares than they initially purchased, amplifying both dividend income and potential capital appreciation. This is a powerful form of compounding often overlooked.

Bonds and Other Fixed-Income Investments

Bonds offer another avenue for compounding. When you invest in a bond, you lend money to a government or corporation in exchange for regular interest payments (coupons) and the return of your principal at maturity. If you reinvest these coupon payments into additional bonds or other investments, you are effectively compounding your returns. Zero-coupon bonds offer an even more direct form of compounding; they are bought at a discount and mature at face value, with the difference representing the compounded interest earned over the bond’s term.

Retirement Accounts: IRAs and 401(k)s

Retirement accounts like Individual Retirement Accounts (IRAs) and 401(k)s are designed to be powerful compounding machines, often with significant tax advantages. Contributions made to these accounts are invested in a variety of assets (stocks, bonds, mutual funds), and any earnings from these investments grow tax-deferred or tax-free until withdrawal in retirement (in the case of Roth accounts). This means that all dividends, capital gains, and interest payments can be fully reinvested and compound over decades without being eroded by annual taxes, providing an enormous boost to the snowball effect. The combination of long time horizons, regular contributions, and tax-advantaged compounding makes these accounts exceptionally effective for wealth building.

Strategies to Maximize Your Compounding Returns

Understanding how compound interest works is the first step; actively applying strategies to optimize its effect is the path to maximizing your financial growth.

Increasing Your Contributions

The most direct way to accelerate compounding is to increase the principal. Regular, consistent contributions, even small ones, add to your base and provide more money for interest to be calculated on. Automating savings and investment contributions is a highly effective method to ensure consistency. As your income grows, consider increasing your contribution percentage. The more you put in early on, the larger the initial snowball, and the faster it will grow.

Optimizing Your Interest Rate

While you can’t control market returns, you can make informed choices to seek better interest rates or returns within your risk tolerance.

- Research High-Yield Accounts: For cash savings, look for high-yield savings accounts or money market accounts that offer better interest rates than traditional banks.

- Diversify Investments: For long-term growth, diversify your portfolio across different asset classes (stocks, bonds, real estate) and geographies to capture broader market returns. Historically, equities have offered higher long-term returns, albeit with greater volatility.

- Review Investment Performance: Periodically review your investment’s performance and adjust if necessary, ensuring your money is working as hard as possible for you. However, avoid chasing returns based on short-term market fluctuations.

Minimizing Withdrawals and Fees

Every withdrawal from an investment account reduces your principal, effectively shrinking the “snowball” and hindering its growth. Try to avoid unnecessary withdrawals, especially from long-term retirement accounts. Similarly, fees (management fees, trading fees, expense ratios on mutual funds) erode your returns. Even seemingly small fees can have a significant impact over decades due to the inverse power of compounding. Choose low-cost index funds or ETFs where appropriate, and be mindful of any hidden fees in your investment products.

Staying Invested for the Long Term

Patience is a virtue, especially when it comes to compound interest. Market downturns and economic volatility can be unsettling, but pulling your money out during these times locks in losses and prevents your investments from recovering and benefiting from subsequent market upturns. For compound interest to truly work its magic, your money needs time – decades, not just years. Resist the urge to time the market and maintain a long-term perspective aligned with your financial goals. Consistently investing through market cycles is often referred to as “dollar-cost averaging” and helps mitigate risk while ensuring continuous compounding.

Common Misconceptions and Important Considerations

While compound interest is a powerful ally, a holistic understanding requires addressing common misconceptions and considering external factors that can influence its real-world impact.

It’s Not Just for Savers: Applying it to Debt

Compound interest works both ways. Just as it can grow your wealth, it can rapidly escalate your debt. Credit card debt, for example, typically carries very high interest rates that compound frequently (often daily or monthly). If not paid down quickly, the interest owed starts accruing interest, making it incredibly difficult to escape. Understanding this inverse effect is crucial. Prioritizing the repayment of high-interest debt is essentially “earning” a guaranteed return equivalent to that interest rate, freeing up capital to then leverage compound interest for wealth building.

Inflation and the Real Rate of Return

Nominal returns from compound interest can be impressive, but it’s important to consider inflation – the rate at which the purchasing power of currency declines over time. If your investment earns 5% interest, but inflation is 3%, your “real” rate of return (what your money can actually buy) is only 2%. For long-term financial planning, always aim for investments that have a strong likelihood of outpacing inflation to ensure your wealth grows in real terms.

Tax Implications of Compound Growth

The tax treatment of your investments can significantly impact the net effect of compounding.

- Taxable Accounts: Interest, dividends, and capital gains are often taxed annually, which means a portion of your compounded gains is siphoned off each year, reducing the base for future compounding.

- Tax-Deferred Accounts (e.g., Traditional IRA/401(k)): Earnings grow without being taxed until withdrawal in retirement. This allows for uninterrupted compounding over decades, leading to a much larger sum. Taxes are paid on the full amount upon withdrawal.

- Tax-Free Accounts (e.g., Roth IRA/401(k)): Contributions are made with after-tax dollars, but qualified withdrawals in retirement are entirely tax-free. This offers the ultimate compounding advantage, as every dollar of growth is yours to keep, forever free from federal income tax.

Understanding these distinctions and utilizing tax-advantaged accounts where appropriate is a critical strategy for maximizing your compounded returns.

The Rule of 72: A Quick Estimation Tool

The “Rule of 72” is a handy mental shortcut to estimate how long it will take for an investment to double in value, given a fixed annual rate of return. You simply divide 72 by the annual interest rate.

For example:

- At an 8% annual return, your money will roughly double in 9 years (72 / 8 = 9).

- At a 6% annual return, it will take approximately 12 years (72 / 6 = 12).

- If you want your money to double in 6 years, you’ll need an approximate 12% annual return (72 / 6 = 12).

This rule provides a quick estimate for financial planning and helps illustrate the impact of different growth rates on your wealth accumulation timeline.

Conclusion

Compound interest is far more than a financial formula; it is a fundamental principle that underpins long-term wealth creation. From the modest beginnings of a savings account to the sophisticated strategies within retirement portfolios, its ability to generate “interest on interest” makes it an indispensable tool for anyone aspiring to financial independence. We’ve explored its mechanics, witnessed its exponential growth through the snowball effect, and identified its presence in various investment vehicles.

The key takeaways are clear:

- Start Early: Time is your most valuable asset in compounding. The sooner you begin, the more pronounced the effect.

- Be Consistent: Regular contributions, even small ones, significantly enhance your principal and accelerate growth.

- Minimize Fees and Withdrawals: Protect your growing principal from erosion by unnecessary costs and premature withdrawals.

- Understand Its Dual Nature: While a powerful ally for wealth, compound interest can also be a formidable foe in the realm of debt.

- Leverage Tax Advantages: Utilize accounts like 401(k)s and IRAs to allow your money to compound uninterrupted by taxes.

By embracing and actively employing the principles of compound interest, you harness a force that works tirelessly on your behalf, turning small, consistent efforts into substantial financial outcomes. It’s not magic; it’s mathematics, made profoundly accessible and incredibly potent for those who choose to understand and utilize it. Make compound interest your ally, and watch your financial future grow, one compounding period at a time.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.