In the realm of personal finance and investing, few concepts carry as much weight as compound growth. Often referred to by Albert Einstein as the “eighth wonder of the world,” compound growth is the process where the value of an investment increases because the earnings on an investment—both capital gains and interest—earn interest as time passes. While it may seem like a simple mathematical curiosity at first glance, it is the fundamental force that transforms modest savings into significant fortunes.

Understanding compound growth is not merely about memorizing a formula; it is about adopting a specific mindset toward time, discipline, and capital allocation. In a world of “get rich quick” schemes and high-frequency trading, compounding stands as a testament to the power of patience and the exponential nature of mathematics.

The Mechanics of Compound Growth: Beyond Simple Interest

To truly grasp compound growth, one must first distinguish it from its linear cousin: simple growth (or simple interest). Simple growth occurs when you earn interest only on the original principal amount. For example, if you invest $1,000 at a 10% simple annual interest rate, you will earn $100 every year. After 30 years, you would have your original $1,000 plus $3,000 in interest, totaling $4,000.

Compound growth, however, functions on a different trajectory. It is interest earned on interest.

The Mathematical Formula

The standard formula for compound growth is $A = P(1 + r/n)^{nt}$.

- A represents the final amount.

- P is the initial principal.

- r is the annual interest rate (decimal).

- n is the number of times interest is compounded per year.

- t is the number of years the money is invested.

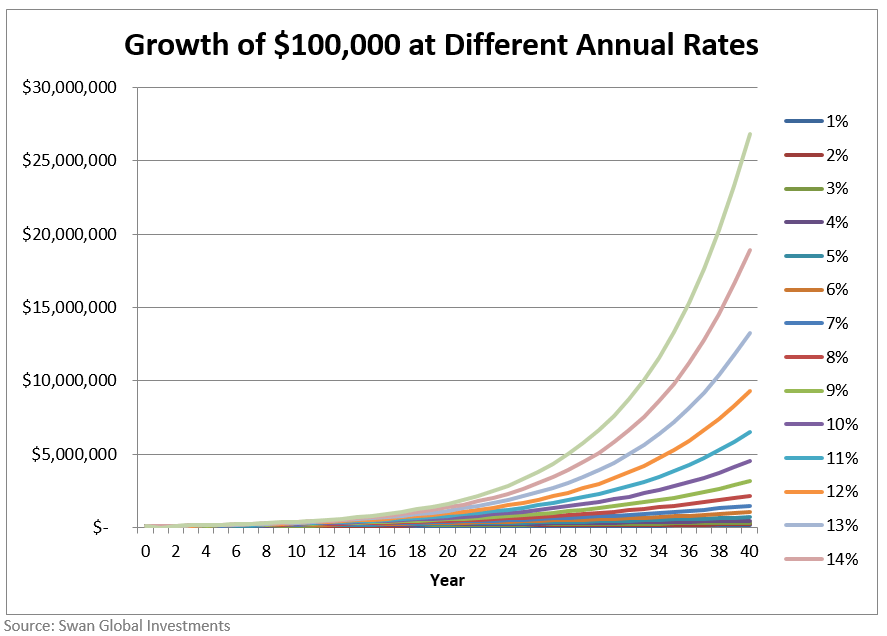

The “exponential” part of this equation is the exponent ($nt$). Because the time factor sits in the exponent, its impact on the final result is not additive; it is multiplicative. This is why compound growth curves look relatively flat in the early years but turn sharply upward—almost vertically—in the later stages.

The Rule of 72

For a professional investor or a casual saver, the “Rule of 72” serves as a vital mental shortcut to understand compounding. By dividing 72 by your annual rate of return, you can estimate how many years it will take for your initial investment to double. If you earn a 7% return, your money doubles roughly every 10 years ($72 / 7 approx 10.3$). If you earn 10%, it doubles every 7.2 years. This highlights how even small increases in the rate of return can drastically shorten the time required to grow wealth.

The Critical Drivers of the Compounding Engine

While the formula provides the structure, three primary variables drive the effectiveness of compound growth: time, the rate of return, and the frequency of compounding.

Time: The Great Multiplier

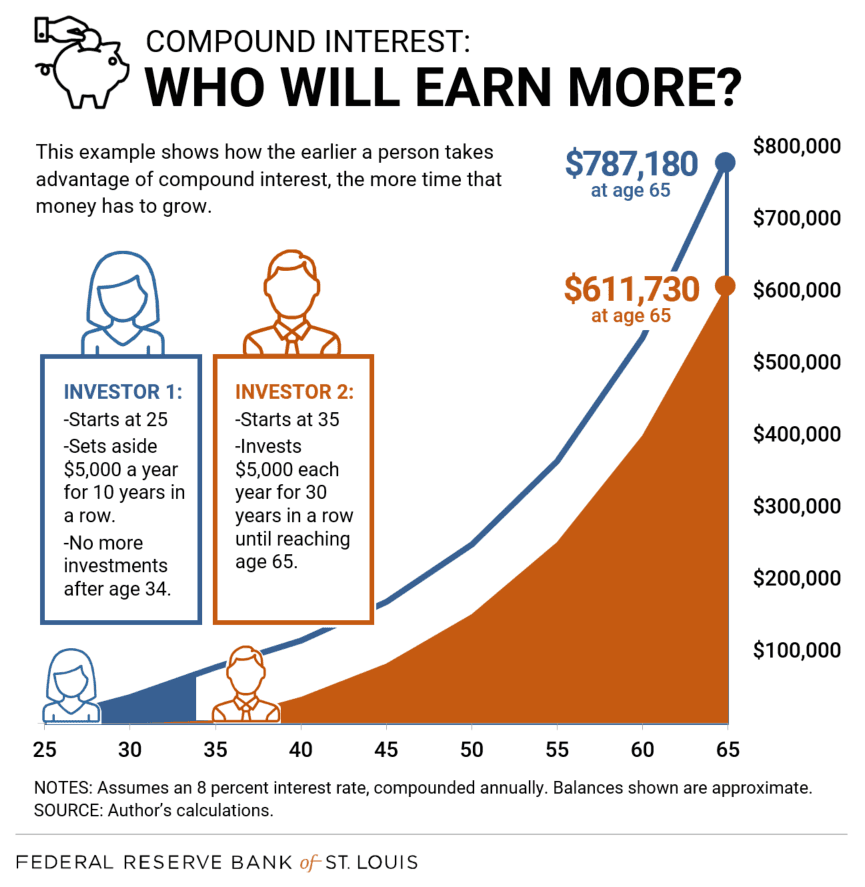

Time is the most significant factor in the compounding equation. The longer the money is left to grow, the more dramatic the results become. This is why financial advisors relentlessly stress the importance of starting early.

Consider two investors, Alex and Blake. Alex starts investing $500 a month at age 25 and stops at age 35, never adding another cent but leaving the money to grow at a 7% annual return. Blake starts at age 35 and invests $500 a month until age 65 (30 years) at the same 7% return. Despite Blake investing three times as much total capital over a much longer duration, Alex will likely end up with a larger portfolio at age 65. The ten-year “head start” allowed Alex’s money to reach the “vertical” part of the growth curve sooner.

The Rate of Return

The rate of return acts as the “accelerant” for compound growth. While you cannot control the stock market’s performance, understanding the impact of the rate is crucial for portfolio construction. A 2% return barely keeps pace with inflation, meaning the “real” compound growth is negligible. However, the difference between a 7% return and a 10% return over 30 years is not just a 3% difference in the final balance—it can result in a final sum that is twice as large. This underscores the importance of choosing asset classes (like equities) that historically offer higher rates of return compared to cash or savings accounts.

Frequency of Compounding

The frequency with which interest is added back to the principal also matters. Interest can be compounded annually, semi-annually, quarterly, monthly, or even daily. The more frequently interest is compounded, the faster the principal grows. For most retail investors, mutual funds and ETFs often distribute dividends quarterly or annually, but the “daily” compounding effect is most commonly seen in high-yield savings accounts or the way interest is charged on credit card debt.

Compound Growth in the Real World: Investment Vehicles

For an individual looking to harness this power, compound growth is typically realized through specific financial instruments and strategies.

The Stock Market and Reinvested Dividends

Equities are perhaps the most accessible way to experience compound growth. Beyond the appreciation of the stock price, dividends play a massive role. When a company pays a dividend, an investor has the choice to take the cash or reinvest it to buy more shares. By choosing to reinvest (often automated through a Dividend Reinvestment Plan, or DRIP), the investor increases their share count. In the next period, they receive dividends on those new shares as well. Over decades, reinvested dividends can account for a substantial portion of total market returns.

Tax-Advantaged Retirement Accounts

The “drag” of taxes can significantly hinder compound growth. In a standard brokerage account, you may owe taxes on capital gains or dividends every year, which pulls money out of the “compounding machine.”

Accounts like the 401(k) or a Roth IRA are designed to maximize compounding by eliminating this annual tax drag. In a Roth IRA, for example, your investments grow tax-free. Every dollar earned stays in the account to earn more money, rather than being diverted to the government. Over a 40-year career, the difference between a tax-dragged account and a tax-advantaged account can amount to hundreds of thousands of dollars.

High-Yield Savings and Fixed Income

While less aggressive than stocks, high-yield savings accounts (HYSAs) and certificates of deposit (CDs) use compound interest to provide steady growth. In a high-interest-rate environment, these tools become viable for preserving capital while still benefiting from the monthly compounding of interest.

Behavioral Strategies for Long-Term Success

The math of compound growth is infallible, but the human element is often the weak link. To let compounding work, one must navigate the psychological challenges of investing.

The Danger of Early Withdrawal and “Leakage”

The greatest enemy of compound growth is interruption. When an investor withdraws funds during a market downturn or “cashes out” a retirement account when changing jobs, they reset the compounding clock. Because the most significant growth happens in the final years of the investment horizon, pulling money out early doesn’t just remove the principal; it removes the potential for all the future growth that principal would have generated. Treating investments as “untouchable” is a prerequisite for compounding success.

Consistency and Dollar-Cost Averaging

Compound growth works best when paired with consistent contributions. Dollar-cost averaging—the practice of investing a fixed amount of money at regular intervals regardless of market conditions—ensures that you are constantly adding fuel to the compounding engine. This strategy also mitigates the risk of “timing the market,” ensuring that you are buying more shares when prices are low and fewer when prices are high, further optimizing the long-term growth rate.

The “J-Curve” and Patience

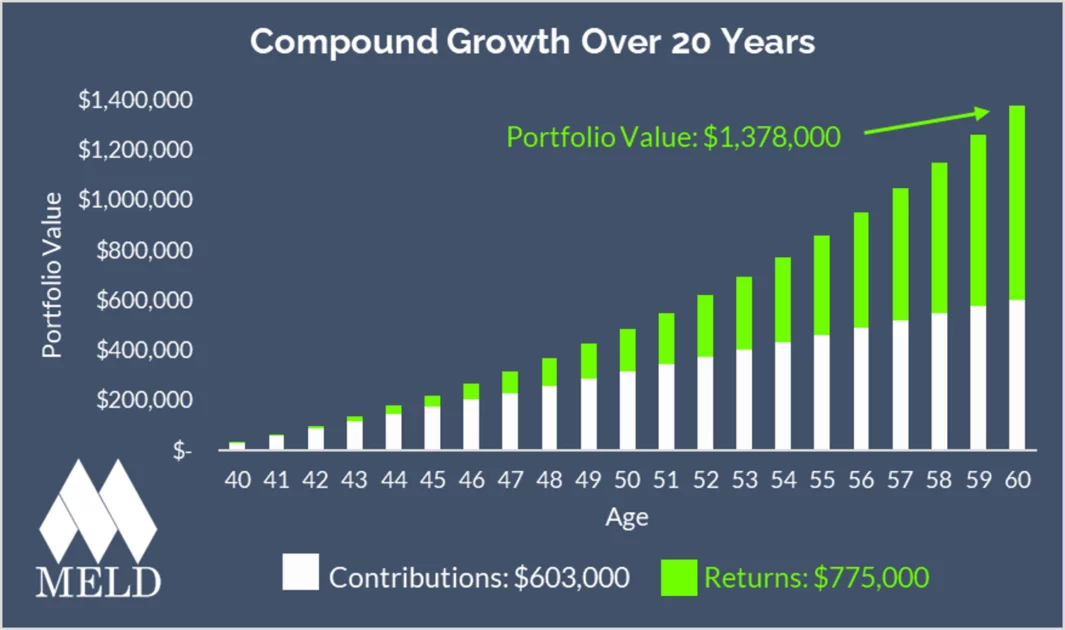

The “J-Curve” refers to the visual representation of compound growth. For the first several years, the growth looks almost like a flat line. This is the “boring” phase where many investors lose interest or decide that “investing doesn’t work.” Insights from professional wealth management suggest that the real “magic” of compounding doesn’t usually become visible until the second or third decade. Staying the course during the flat part of the curve is what separates successful investors from those who fluctuate between strategies.

The Negative Side of Compounding: Debt and Inflation

While compound growth is a tool for wealth creation, it is a double-edged sword. It can work against you just as powerfully as it can work for you.

High-Interest Debt

Credit card debt is the inverse of a retirement account. When you carry a balance, the bank charges you interest, which is then added to your balance. The following month, you are charged interest on that interest. With average credit card APRs often exceeding 20%, the compounding effect can lead to a debt spiral that is mathematically difficult to escape. Understanding compound growth is the first step in realizing why high-interest debt must be liquidated before significant investing begins.

The Erosion of Inflation

Inflation is essentially “negative compound growth” on the purchasing power of your currency. If inflation is 3% per year, the value of $100 today will be significantly less in 20 years. To achieve “real” compound growth, your investments must return a rate higher than the rate of inflation. This is why “playing it safe” by keeping all of one’s wealth in a standard checking account is actually a guaranteed way to lose wealth over time through the compounding effect of rising prices.

Conclusion: Starting the Engine Today

Compound growth is the most powerful tool in the arsenal of the individual investor. It does not require a high IQ or a background in complex derivatives; it requires only three things: capital, a reasonable rate of return, and—most importantly—time.

The math of compounding proves that wealth is not built overnight, but rather accumulated through the relentless reinvestment of gains. By starting as early as possible, minimizing fees and taxes, and avoiding the temptation to interrupt the process, anyone can leverage the exponential nature of finance to secure their financial future. The best time to start was ten years ago; the second best time is today.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.