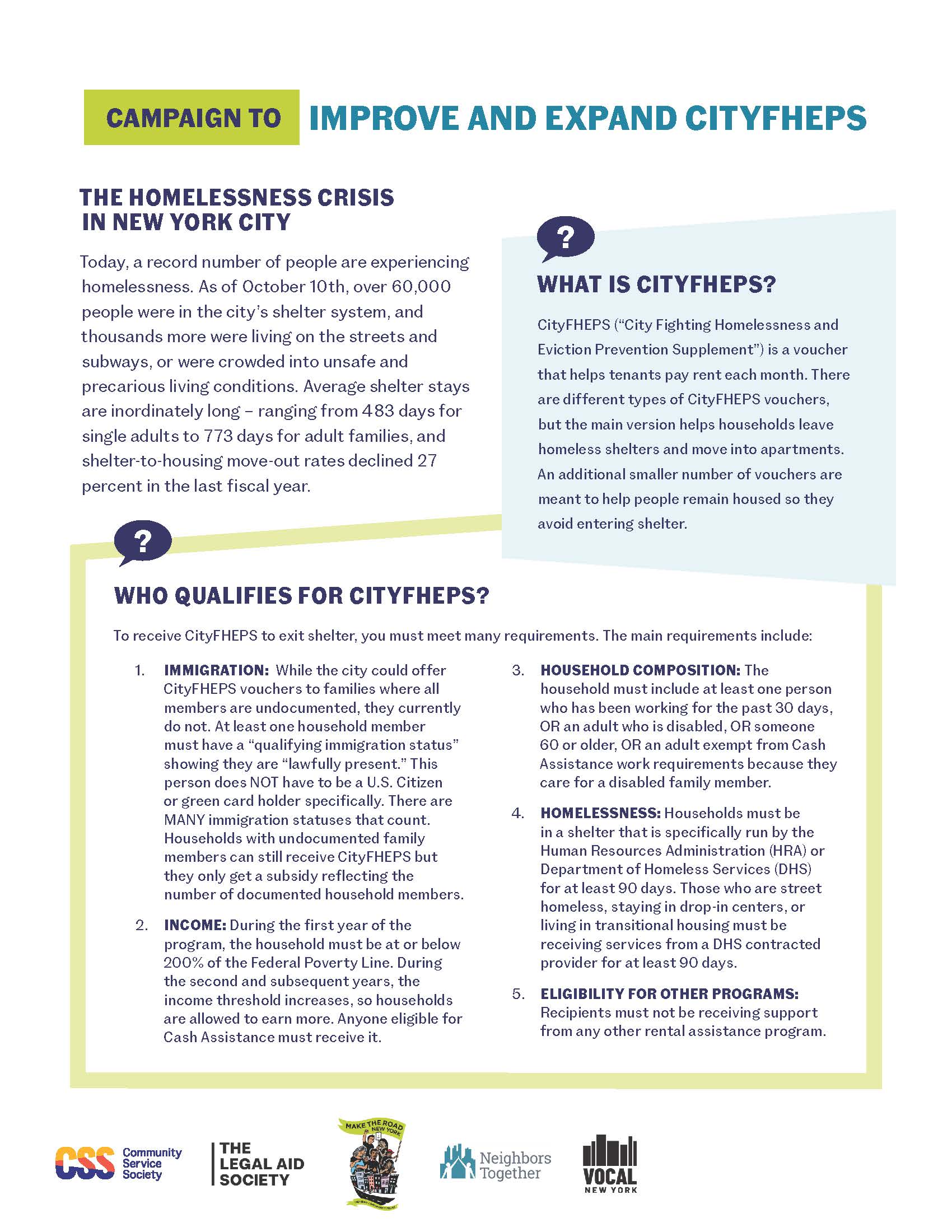

In the complex landscape of urban economics, housing remains the single largest expense for the average household. In a city like New York, where the real estate market is notoriously aggressive, the gap between stagnant wages and rising rents has created a significant financial chasm. To bridge this gap, the City of New York developed CityFHEPS (City Fighting Homelessness and Eviction Prevention Supplement). This program is not merely a social service; it is a critical financial tool designed to stabilize the local economy by preventing homelessness and providing a steady stream of rental income to property owners.

Understanding CityFHEPS requires looking through the lens of personal and business finance. It is a rental assistance supplement that helps individuals and families find and keep housing. By injecting government-backed capital directly into the private rental market, CityFHEPS serves as a vital pillar of the city’s financial strategy to manage the high costs associated with the shelter system and housing instability.

Understanding the Financial Mechanics of CityFHEPS

At its core, CityFHEPS is a financial subsidy program managed by the Department of Social Services (DSS) and the Human Resources Administration (HRA). It consolidates several older, more fragmented rental assistance programs into a single, streamlined financial vehicle. The primary goal is to provide a reliable payment structure that allows low-income New Yorkers to compete in a market where they would otherwise be priced out.

Income Limits and Financial Eligibility

Eligibility for CityFHEPS is strictly defined by financial parameters. To qualify, a household’s total gross income must generally be at or below 200% of the Federal Poverty Level (FPL). This metric ensures that the funds are targeted toward those for whom housing costs represent an unsustainable percentage of their monthly budget.

From a personal finance perspective, the program acts as a massive “side hustle” or passive income supplement provided by the state. Instead of a family spending 70% of their income on rent—a situation known as being “severely rent-burdened”—CityFHEPS caps the tenant’s contribution (usually around 30% of their income), while the city covers the remainder. This allows the household to reallocate their limited capital toward other essential financial goals, such as debt reduction, education, or emergency savings.

The Role of the Human Resources Administration (HRA)

The HRA acts as the financial fiduciary for the program. When a tenant is approved for CityFHEPS, the HRA issues a “Shopping Letter.” This document is essentially a pre-approval for a specific amount of financial backing, similar to a mortgage pre-approval letter. It tells landlords that the City of New York is guaranteeing a portion of the monthly rent.

The HRA manages the disbursement of these funds, ensuring that payments are made directly to the landlord. This direct-payment model is a crucial component of the program’s financial design, as it removes the risk of the tenant misappropriating the rent money, thereby offering a layer of security to the property owner’s cash flow.

Navigating Personal Finance with Housing Subsidies

For the recipient, CityFHEPS is a transformative financial asset. In a city where a studio apartment can cost upwards of $2,000, a low-income worker earning $15 an hour faces an impossible mathematical reality. CityFHEPS corrects this market failure by adjusting the individual’s purchasing power to meet market demands.

How Payment Standards Affect Your Budget

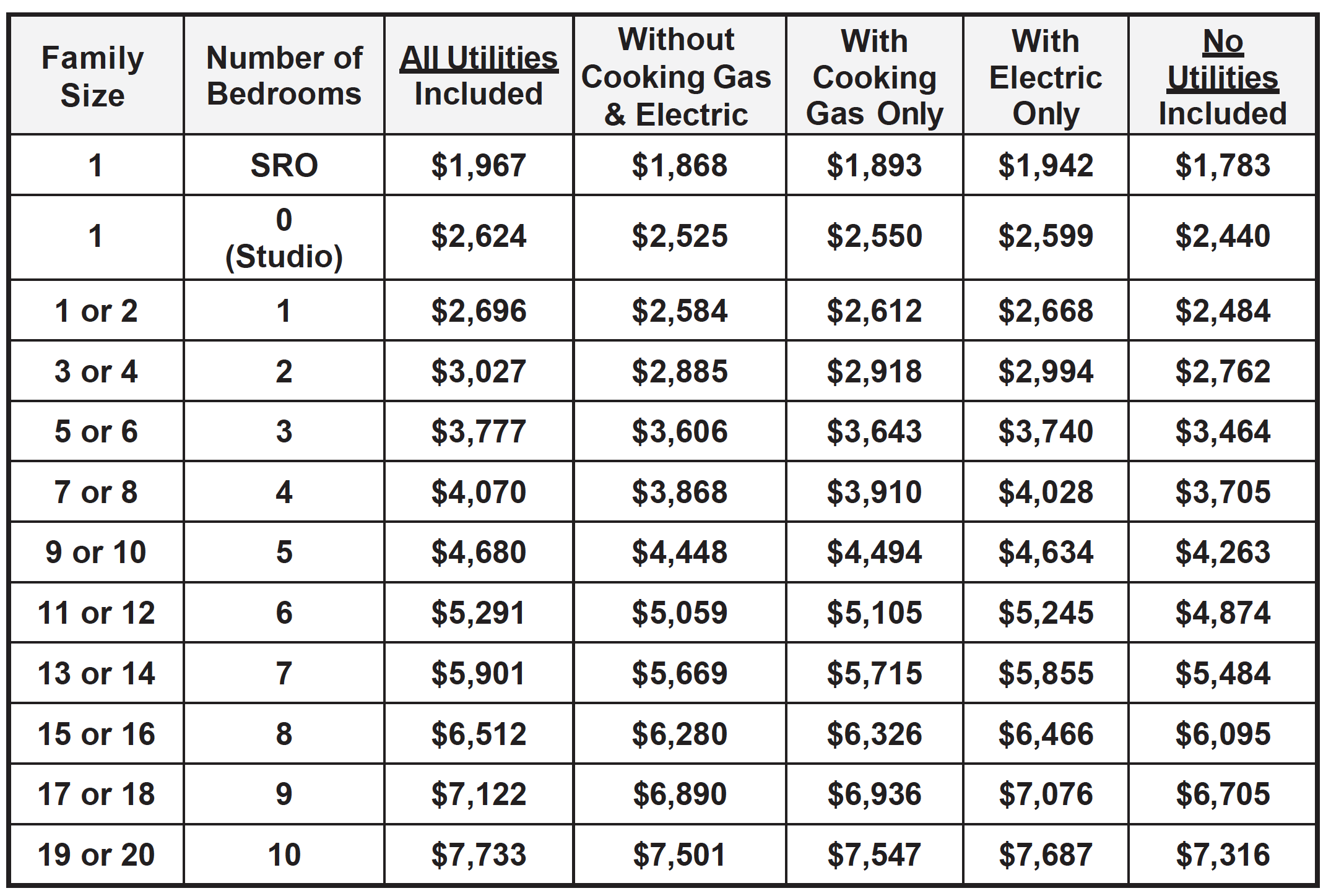

The amount CityFHEPS will pay is dictated by “Payment Standards,” which are indexed to the Fair Market Rents (FMR) set by the federal government. For example, if the payment standard for a one-bedroom apartment is $2,451, CityFHEPS will cover the difference between that amount and the tenant’s required contribution.

For the tenant, this creates a predictable monthly expenditure. Financial planning becomes possible because the “rent” variable in their budget is stabilized. This stability is the bedrock of financial health; it prevents the “eviction-homelessness-job loss” cycle that often leads to total financial ruin. By capping rent costs, the program effectively increases the tenant’s disposable income, which is then cycled back into the local economy through the purchase of goods and services.

Long-term Financial Stability and Subsidy Renewal

CityFHEPS is not a one-time grant; it is a recurring financial supplement. However, it requires annual recertification. This process involves a full audit of the household’s finances to ensure they still meet the eligibility criteria. From a financial management standpoint, this encourages participants to maintain accurate records of their income and expenses.

Furthermore, recent legislative changes have expanded the program’s reach, removing certain barriers like the “90-day shelter stay” rule. This means the financial assistance is now more accessible as a preventative measure. By providing the funds before a family loses their home, the city saves thousands of dollars in shelter costs, and the family avoids the catastrophic financial hit associated with an eviction on their credit report.

The Business Finance Perspective: Why Landlords Participate

While CityFHEPS is often discussed as a social benefit, it is also a powerful business tool for landlords and property management companies. In the world of real estate investment, “vacancy loss” and “bad debt” (unpaid rent) are the primary enemies of a healthy bottom line. CityFHEPS offers a solution to both.

Guaranteed Rental Income and Incentives

For a landlord, a CityFHEPS tenant represents a recession-proof revenue stream. While a private-pay tenant might lose their job and stop paying rent, the City of New York does not “go out of business.” The government portion of the rent is guaranteed and arrives consistently.

To make the program even more financially attractive to the business community, the city often provides “Landlord Incentives.” These can include:

- Sign-on Bonuses: A one-time payment equivalent to one or two months’ rent.

- Security Deposit Vouchers: Coverage for potential damages or unpaid rent at the end of a lease.

- Broker Fees: The city often pays the full broker’s fee, making these units easier to move for real estate professionals.

These incentives turn CityFHEPS into a high-yield opportunity for property owners who are willing to navigate the administrative requirements.

Understanding the “Roommate” and “Single Room” Financial Models

CityFHEPS also accounts for alternative housing models, such as Single Room Occupancy (SRO) or roommate arrangements. From a business finance perspective, this allows landlords to maximize the “rent per square foot” of a property. By renting individual rooms to multiple CityFHEPS recipients, a landlord can often generate higher total gross income than they would by renting the entire apartment to a single family at a market rate. This flexibility makes the program a versatile tool for different types of real estate portfolios, from large multi-family buildings to smaller individual units.

The Broader Economic Impact of Rental Assistance

When we look at CityFHEPS through a macro-economic lens, we see a program that impacts the fiscal health of the entire city. The “Money” story of CityFHEPS is not just about individual checks; it is about the efficient allocation of public resources.

Reducing the Cost of Homelessness on Public Funds

It is significantly more expensive for a city to house a family in a shelter than it is to provide them with a rental subsidy. A shelter stay can cost the city upwards of $4,000 to $8,000 per month depending on the facility and services provided. In contrast, a CityFHEPS subsidy might cost the city $1,500 per month.

By transitioning individuals from shelters to permanent housing, or preventing them from entering the system entirely, CityFHEPS acts as a cost-saving measure for the municipal budget. It is a strategic reinvestment of tax dollars that yields a high “social return on investment” (SROI) by keeping the labor force stable and reducing the burden on emergency services, hospitals, and the legal system.

Supporting the Local Real Estate Market

Finally, CityFHEPS provides a “floor” for the rental market. During economic downturns, when private demand might slacken, the consistent demand from voucher holders ensures that buildings remain occupied and owners can continue to pay their mortgages and property taxes. This circular flow of capital—from the city to the landlord, from the landlord to the bank and the tax office—helps maintain the overall financial stability of the New York City real estate market.

In conclusion, CityFHEPS is a sophisticated financial instrument designed to manage the high stakes of urban living. Whether viewed as a personal finance lifeline for tenants or a reliable revenue stream for landlords, its impact on the “money” side of New York City is undeniable. By understanding its mechanics, eligibility, and incentives, stakeholders can better navigate the financial realities of one of the world’s most expensive housing markets.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.