In the modern digital economy, moving money from one point to another feels instantaneous. However, behind every “Send” button on a banking app lies a complex infrastructure of identifiers that ensure your funds arrive at the correct destination. For customers of JPMorgan Chase, one of the largest financial institutions in the world, the question “What is Chase Bank’s routing number?” is rarely answered with a single digit. Because Chase operates across dozens of states and serves millions of customers, it utilizes a variety of routing numbers based on geography and the type of transaction being performed.

Understanding your routing number is a fundamental aspect of personal finance management. Whether you are setting up a direct deposit for a new job, paying a utility bill online, or receiving a domestic wire transfer, having the correct nine-digit code is the difference between a seamless transaction and a week-long administrative headache.

1. Understanding the Role of Routing Numbers in Personal Finance

A routing number, often referred to as an ABA (American Bankers Association) routing transit number (RTN), is a nine-digit code used to identify a specific financial institution within the United States. Think of it as a zip code for your bank. While your account number identifies your individual “house” within the bank, the routing number tells the Federal Reserve and other banks exactly which “city and street” the money needs to travel to.

What is an ABA Routing Number?

The ABA routing number system was developed in 1910 to make the processing of paper checks more efficient. Over a century later, the system remains the backbone of the U.S. financial grid. Every legitimate bank in the U.S. is assigned at least one routing number. For a massive entity like Chase, which has grown through decades of mergers and acquisitions (including the likes of Washington Mutual and Bear Stearns), the bank has inherited and maintained several different routing numbers to manage its vast regional operations.

The Anatomy of a Routing Number

A routing number isn’t just a random string of digits. It follows a specific logic:

- The first two digits represent the Federal Reserve district where the bank is located.

- The third digit identifies the Federal Reserve check processing center originally assigned to the bank.

- The fourth digit identifies the state where the bank is located.

- The next four digits are unique to the bank itself.

- The ninth digit is a “checksum,” a mathematical verification used to ensure the first eight digits were entered correctly.

Why Chase Has Multiple Routing Numbers

Unlike smaller community banks that might have only one routing number for all operations, Chase utilizes a regional model. When you open an account, your routing number is typically tied to the state in which you opened that account. This helps the bank manage liquidity and transaction processing across different regional Federal Reserve branches. If you move from New York to California, your routing number will remain the one from New York unless you close that account and open a new one in your new state.

2. How to Find Your Specific Chase Routing Number

Because Chase uses different numbers for different regions, you cannot simply guess which one to use. Using the wrong routing number can lead to rejected transfers or, in some cases, funds being temporarily held in limbo. Fortunately, finding your specific number is a straightforward process.

A State-by-State Breakdown

Chase provides a directory of routing numbers for various states. While these are subject to update, here are some of the most common Chase routing numbers for personal checking accounts:

- California: 122000661

- New York: 021000021

- Texas: 111000614

- Illinois: 071000013

- Florida: 063100277

- Arizona: 122105155

- Ohio: 044000037

It is important to note that these numbers are primarily for ACH (Automated Clearing House) transfers, such as direct deposits and automatic bill payments.

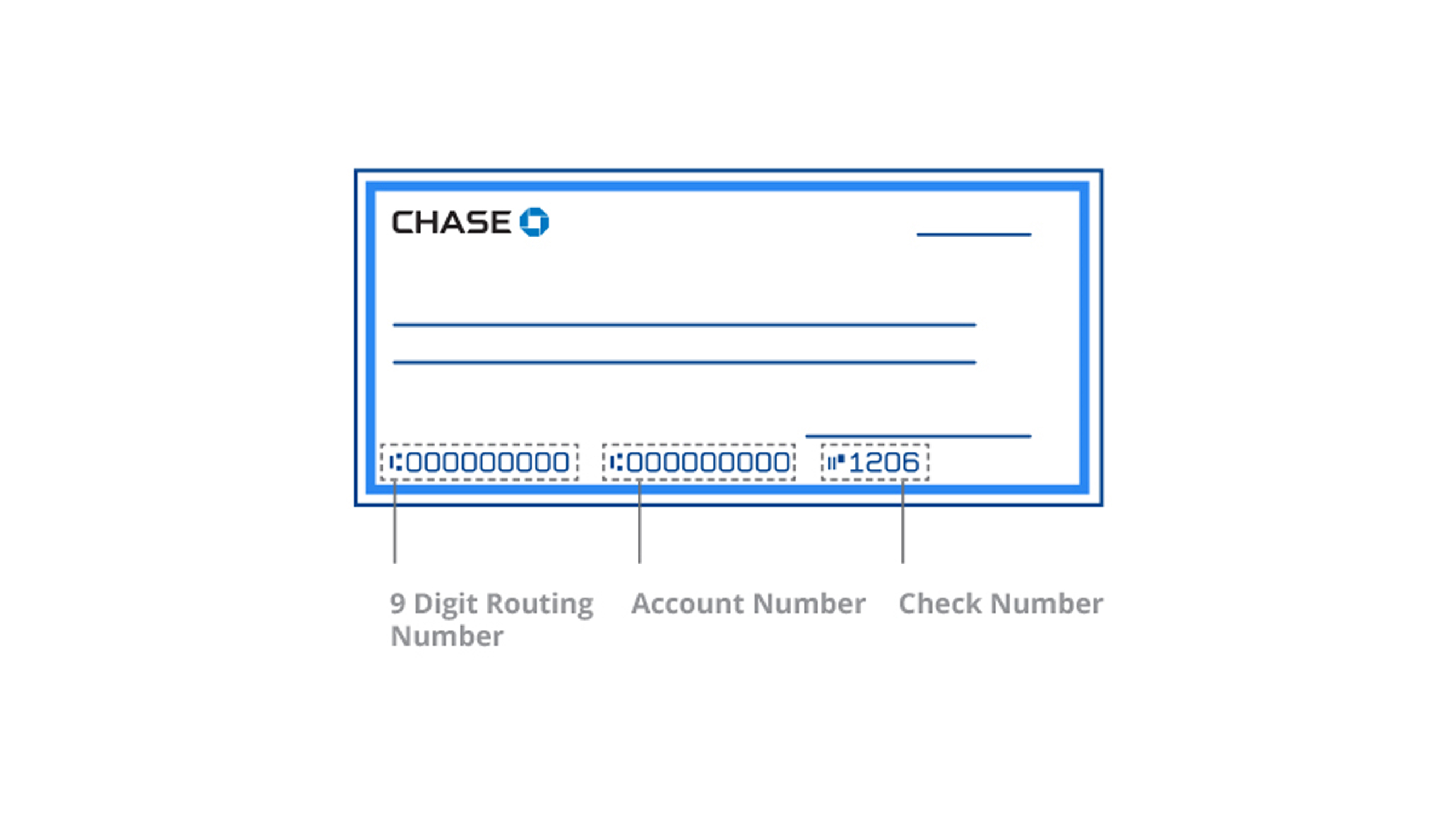

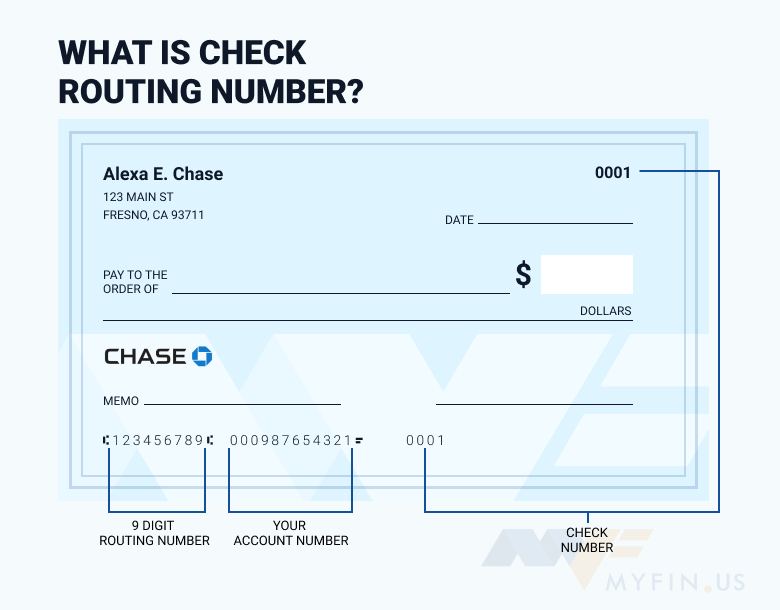

Locating the Number on a Physical Check

If you still use paper checks, the easiest way to find your routing number is to look at the bottom left-hand corner of a check. You will see three sets of numbers printed in a special computer-readable font. The first set of nine digits on the far left is your routing number. The second set of numbers is your account number, and the third (shorter) set is the check number.

Finding the Number via the Chase Mobile App and Online Banking

In an era of paperless banking, most customers rely on digital tools. To find your routing number via the Chase website or app:

- Log in to your account.

- Select the specific checking or savings account you are inquiring about.

- Click on “See details” or “Account services.”

- Your routing and account numbers will be displayed (usually masked for security, but you can click an icon to reveal them).

3. When to Use a Routing Number vs. Other Identifiers

In personal finance, precision is paramount. One of the most common mistakes consumers make is using an ACH routing number for a wire transfer, or vice versa. While they may seem interchangeable, they serve different functions within the banking software.

Direct Deposits and Bill Pay (ACH)

The most common use for a routing number is for ACH transactions. This includes your employer depositing your paycheck or you setting up an automatic payment for your mortgage. For these “electronic checks,” you should always use the standard regional routing number associated with your account’s home state. These transactions are typically processed in batches and may take 1-3 business days to clear.

Domestic and International Wire Transfers

Wire transfers are different from ACH transfers because they happen in near real-time and are handled individually rather than in batches. Chase often uses a specific routing number for all domestic wire transfers, regardless of which state the account was opened in. As of the current period, Chase often uses a centralized routing number for incoming domestic wires to streamline the process.

For international transfers, a routing number is not enough. You will need a SWIFT/BIC code. This is an international standard for identifying banks worldwide. The SWIFT code for Chase (JPMorgan Chase Bank, N.A.) is generally CHASUS33. Without this code, an international bank will not be able to direct funds to the Chase network in the United States.

Peer-to-Peer (P2P) Payments

With the rise of apps like Zelle, Venmo, and Cash App, many people wonder if they need their routing number for daily transfers. Zelle is integrated directly into the Chase app, meaning you don’t need to manually enter your routing number to send or receive money; the app handles the “handshake” between banks automatically. However, if you are linking your Chase account to Venmo or a similar third-party service for the first time, you will indeed need to provide your routing and account numbers to verify ownership.

4. Security and Best Practices for Protecting Your Financial Data

Because a routing number and an account number are the only two pieces of information needed to initiate an ACH pull from an account, protecting this information is a vital component of your digital security strategy.

Is It Safe to Share Your Routing Number?

A routing number itself is public information. You can find Chase’s routing numbers on their website or in this article. There is no inherent risk in someone knowing a bank’s routing number. However, the risk arises when your routing number is paired with your account number. With these two pieces of information, an unauthorized party could theoretically print “demand drafts” (fake checks) or set up unauthorized bill payments.

Common Scams to Watch Out For

Scammers often pose as Chase representatives via “phishing” emails or texts, asking you to “verify” your routing and account numbers to prevent an account freeze. Chase will never ask you for these details through an unsolicited text or email. Another common scam involves “overpayment,” where a scammer sends you a fake check and asks you to wire back a portion of the funds using your routing information. Always verify the source of any transaction before providing your banking coordinates.

Verifying Information Before Large Transfers

If you are involved in a high-stakes financial transaction, such as a down payment on a home, never rely solely on an email for routing instructions. Wire fraud in real estate is a multi-billion-dollar problem. Always call a verified phone number for the title company or the bank to verbally confirm the routing and account numbers before sending a wire transfer.

5. The Evolution of Chase’s Banking Infrastructure

The reason Chase has such a complex web of routing numbers is a testament to its history as a pillar of American finance. JPMorgan Chase is the result of the merger of more than 1,000 institutions over two centuries.

Mergers and Legacy Systems

When Chase acquired Washington Mutual in 2008, it didn’t just acquire customers; it acquired a massive technological infrastructure. For years, former WaMu customers continued to use their old routing numbers because migrating millions of accounts to a new system overnight is a logistical nightmare. While Chase has since consolidated many of these, some legacy numbers still function to ensure that long-standing automated payments aren’t disrupted.

The Shift Toward Real-Time Payments (RTP)

The future of routing numbers may look very different. The U.S. is currently moving toward Real-Time Payments (RTP) and the FedNow service. These systems aim to make transfers as fast as a text message, 24/7/365. As these technologies become the standard, the way we use routing numbers may be simplified by “alias” systems, where your phone number or email acts as a proxy for your complex banking digits.

Conclusion: The Importance of Accuracy

While the world of finance becomes increasingly automated, the fundamental “addressing” system of routing numbers remains essential. For a Chase customer, knowing your routing number—and knowing which one to use—is the first step toward financial literacy and security. By taking a few moments to verify your state-specific code and understanding the difference between ACH and wire requirements, you ensure that your money moves exactly where it’s supposed to, safely and efficiently. Always refer back to your official Chase mobile app or a physical check for the most accurate, up-to-the-minute information regarding your specific account.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.