In the complex landscape of personal finance, one of the most significant variables for any individual or family is the cost of healthcare. For many, choosing a health insurance plan feels like a balancing act between monthly affordability and long-term security. Among the various tiers of coverage defined by the Affordable Care Act (ACA), “Catastrophic Insurance” stands out as a unique financial instrument. It is designed not for everyday medical needs, but as a safety net for the “worst-case scenarios”—those life-altering medical events that could otherwise lead to bankruptcy.

Understanding catastrophic insurance is essential for young professionals, those experiencing financial hardship, and anyone looking to optimize their personal balance sheet while maintaining a baseline of protection. This guide explores the mechanics, eligibility, and strategic financial implications of choosing a catastrophic plan.

The Fundamentals of Catastrophic Health Insurance

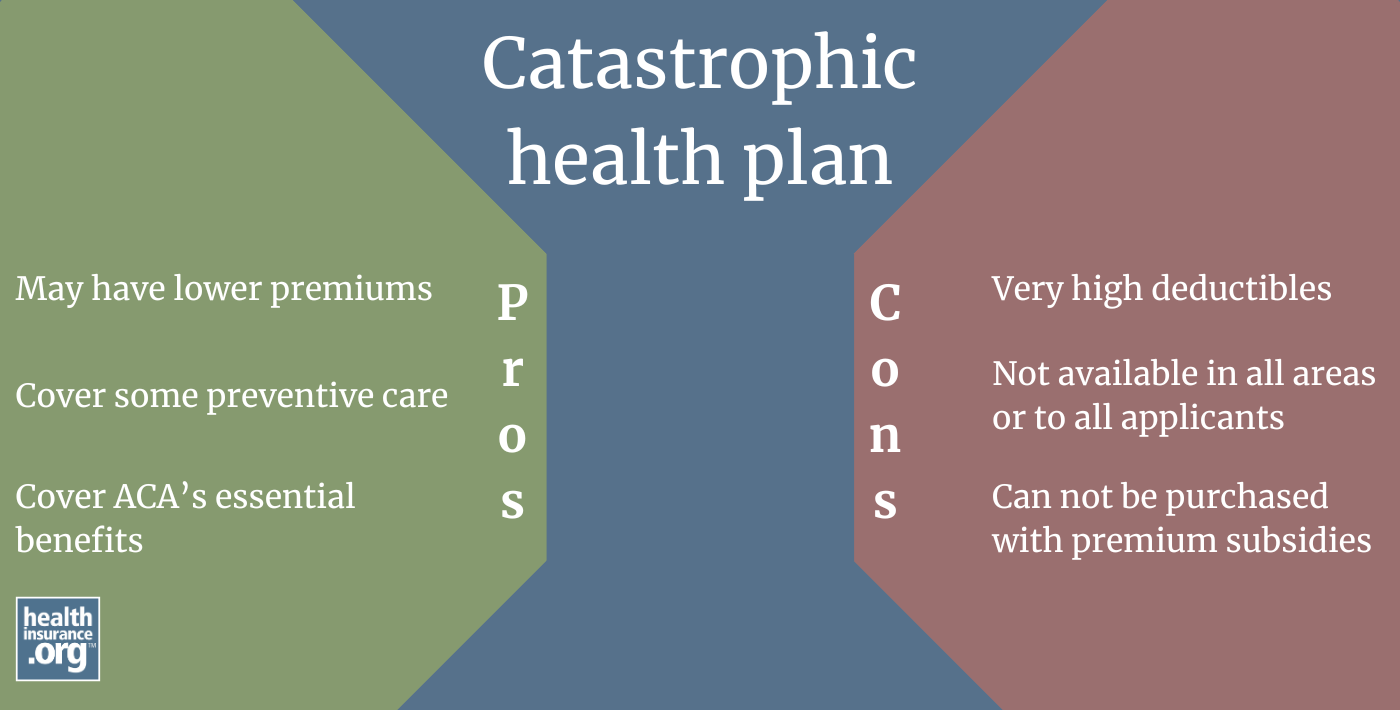

Catastrophic insurance is a type of high-deductible health plan (HDHP) specifically structured to protect policyholders from the immense costs associated with serious accidents or chronic illnesses. Unlike comprehensive plans that might cover a portion of your prescriptions or doctor’s visits from day one, a catastrophic plan requires the individual to pay for almost all medical care out of pocket until a very high annual deductible is met.

The Core Mechanics of the Plan

The primary characteristic of a catastrophic plan is its low monthly premium. Because the insurance company is taking on less immediate risk, they charge significantly less per month than they would for a Bronze, Silver, or Gold plan. However, the trade-off is the deductible. As of 2024 and 2025, these deductibles are often set at the maximum out-of-pocket limit allowed by law—frequently exceeding $9,000 for an individual.

Once this deductible is reached, the insurance company typically pays 100% of the costs for covered essential health benefits. This means that while you are responsible for the first several thousand dollars of your care, you are shielded from a $100,000 hospital bill resulting from a major surgery or an extended ICU stay.

Essential Health Benefits and Preventive Care

A common misconception is that catastrophic insurance covers nothing until the deductible is met. Under the ACA, these plans are required to cover certain “essential health benefits” even before the deductible is reached. This includes:

- Preventive Services: Annual check-ups, certain screenings (like mammograms or colonoscopies), and immunizations are covered at 100% with no out-of-pocket cost.

- Primary Care Visits: Most catastrophic plans allow for at least three primary care visits per year before the deductible applies, though a small co-pay may still be required.

Eligibility and the Financial Profile of the Policyholder

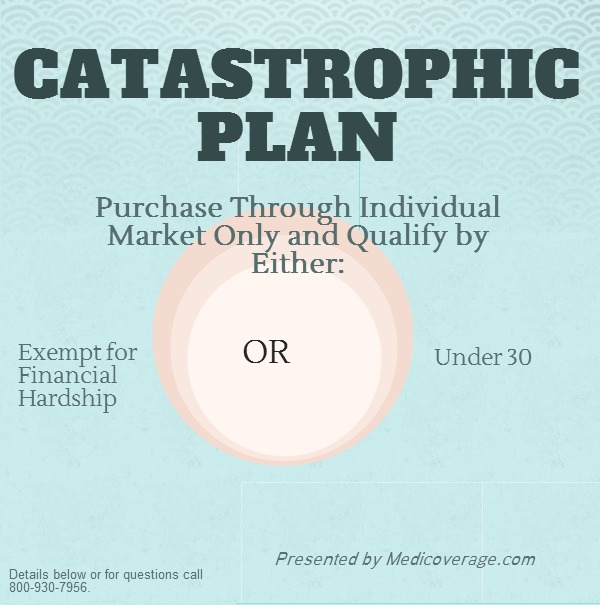

Catastrophic insurance is not available to everyone. It is a restricted financial product designed for a specific demographic and those in specific financial circumstances. The government limits access to these plans to ensure that those who can afford more comprehensive coverage are incentivized to participate in the broader insurance pools.

The Under-30 Rule

The most common group eligible for catastrophic insurance is individuals under the age of 30. For young adults who are generally healthy and may be just starting their careers, these plans offer a way to comply with health requirements and protect against disaster without the burden of a $400 or $500 monthly premium. It is a “just in case” policy for a demographic that statistically utilizes fewer medical services.

Hardship Exemptions and Affordability

If you are over 30, you can only purchase a catastrophic plan if you qualify for a “hardship exemption” or an “affordability exemption.” This is a crucial area of personal finance for those navigating economic instability. Exemptions are granted by the Health Insurance Marketplace for various reasons, including:

- Homelessness or Eviction: If you have faced housing instability.

- Bankruptcy: If you have filed for bankruptcy in the last six months.

- Domestic Violence: If you are a survivor of domestic abuse.

- Death of a Close Family Member: If the loss has impacted your financial standing.

- Unexpected Financial Hardship: Such as a fire, flood, or other natural or human-caused disaster that caused substantial damage to your property.

For individuals in these situations, catastrophic insurance provides a way to stay insured at the lowest possible cost during a period of recovery.

How Catastrophic Plans Compare to Traditional Metal Tiers

To make an informed financial decision, one must compare catastrophic plans against the standard “Metal” tiers: Bronze, Silver, Gold, and Platinum. Each tier represents a different split of costs between the insurer and the insured.

Premiums vs. Deductibles: The Financial Trade-off

In the world of personal finance, health insurance is often a “pay now or pay later” scenario.

- Gold/Platinum Plans: High monthly premiums, very low deductibles. These are “pay now” plans, ideal for those who know they will need frequent medical care.

- Bronze/Silver Plans: Moderate premiums and moderate deductibles.

- Catastrophic Plans: The lowest possible premiums and the highest possible deductibles. This is the “pay later” (and only if necessary) model.

If you are a healthy individual who rarely sees a doctor, choosing a catastrophic plan over a Bronze plan could save you thousands of dollars in premiums over the course of a year. However, if an accident does occur, you must have the liquidity to cover the deductible immediately.

The Impact of Premium Tax Credits

One of the most important financial distinctions is the availability of subsidies. Most people who buy insurance through the Marketplace are eligible for Premium Tax Credits based on their income. However, catastrophic plans are not eligible for these tax credits.

This creates a unique financial paradox: For some low-income individuals, a Silver or Bronze plan might actually be cheaper than a catastrophic plan because the tax credits can be applied to those tiers but not to the catastrophic tier. Therefore, it is vital to run the numbers on the Marketplace after subsidies are calculated before assuming the catastrophic plan is the most economical choice.

The Risks and Rewards of High-Deductible Coverage

Every financial decision involves a risk-reward calculation. Catastrophic insurance is no different, and its suitability depends entirely on your personal risk tolerance and cash flow.

Advantages: Lower Monthly Costs and Emergency Security

The primary reward is cash flow. By paying a minimal premium, you keep more money in your monthly budget. This capital can be redirected toward high-interest debt repayment, an emergency fund, or retirement accounts. Furthermore, the plan serves its namesake purpose: it prevents a “catastrophic” financial collapse. If you are diagnosed with a serious illness, your financial liability is capped at the annual out-of-pocket maximum, rather than being theoretically infinite.

Risks: High Out-of-Pocket Liability

The risk is equally clear. If you break a leg or require a minor surgery that costs $5,000, you will likely pay for the entire procedure yourself. For someone living paycheck to paycheck, a $9,000 deductible is a mountain that is impossible to climb. Without a dedicated emergency fund, a catastrophic plan can feel like having no insurance at all for mid-level medical needs.

Strategic Financial Planning with Catastrophic Coverage

Choosing a catastrophic plan should not be a passive decision; it should be part of a broader financial strategy. If you choose this path, you must manage your finances differently than someone with a low-deductible plan.

The Role of the Emergency Fund

If you carry a catastrophic insurance policy, your emergency fund should, at a minimum, equal your plan’s annual out-of-pocket maximum. If your deductible is $9,450, you should have that amount in a high-yield savings account or a liquid money market fund. This ensures that a medical emergency becomes a physical crisis but not a financial one.

Catastrophic Insurance vs. HSAs

It is a common error to confuse Catastrophic plans with Health Savings Account (HSA)-eligible plans. While both have high deductibles, not all catastrophic plans are HSA-compliant. An HSA is a powerful financial tool that allows for triple-tax-advantaged savings for medical expenses. Many Bronze and Silver plans are “HSA-qualified,” but most catastrophic plans are not because their deductibles and out-of-pocket structures don’t always align with IRS regulations for HSAs. If your goal is to use health insurance as a vehicle for tax-advantaged investing, you must verify the plan’s HSA eligibility before enrolling.

When to Transition to Comprehensive Coverage

Personal finance is dynamic. A catastrophic plan might be perfect for a 24-year-old freelancer with no dependents, but it is rarely the right choice for someone planning to start a family. Prenatal care, delivery, and pediatric visits quickly exceed the costs where a Silver or Gold plan would have been more cost-effective. Regularly auditing your life stage and health needs during the annual Open Enrollment period is crucial to ensuring your insurance still fits your financial reality.

Conclusion

Catastrophic insurance is a specialized tool in the personal finance toolkit. It offers a lean, cost-effective way for young people and those in financial distress to secure themselves against the most devastating financial impacts of the healthcare system. However, it requires a high degree of financial discipline.

To successfully navigate a catastrophic plan, one must understand that they are essentially self-insuring for routine and mid-level medical costs while outsourcing the “extreme” risk to the insurer. By maintaining a robust emergency fund and taking full advantage of the free preventive services provided, a policyholder can leverage catastrophic insurance to maintain financial liquidity and long-term stability in an unpredictable world.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.