Bills payment is an inescapable reality of modern life, a fundamental financial responsibility that touches nearly every individual and business. Far from being a mere transaction, it represents the backbone of financial stability, influencing everything from credit scores to access to essential services. Understanding “what is bills payment” goes beyond knowing how to remit funds; it delves into strategic financial management, budget adherence, and securing long-term financial health. This article will explore the multifaceted world of bills payment, offering insights into its significance, methods, and best practices for effective management within the realm of personal and business finance.

The Fundamentals of Bills Payment

At its core, bills payment is the act of remitting money to a service provider or lender in exchange for goods, services, or to fulfill a financial obligation. This seemingly simple act is a critical component of economic ecosystems, ensuring that businesses can operate, services can be maintained, and individuals can live comfortably with access to necessities.

Defining Bills and Their Purpose

A “bill” is essentially an invoice or statement of charges for services rendered, goods purchased, or money borrowed. These obligations can range from essential utilities to luxury subscriptions. The purpose of paying these bills is twofold: first, to compensate the provider for their offering, thereby maintaining access to that service or product; and second, to fulfill contractual agreements, avoiding penalties and preserving one’s financial standing. Common examples include monthly rent or mortgage payments, utility bills (electricity, water, gas), internet and phone bills, loan repayments (car, student, personal), credit card statements, insurance premiums, and various subscription services.

The Importance of Timely Payments

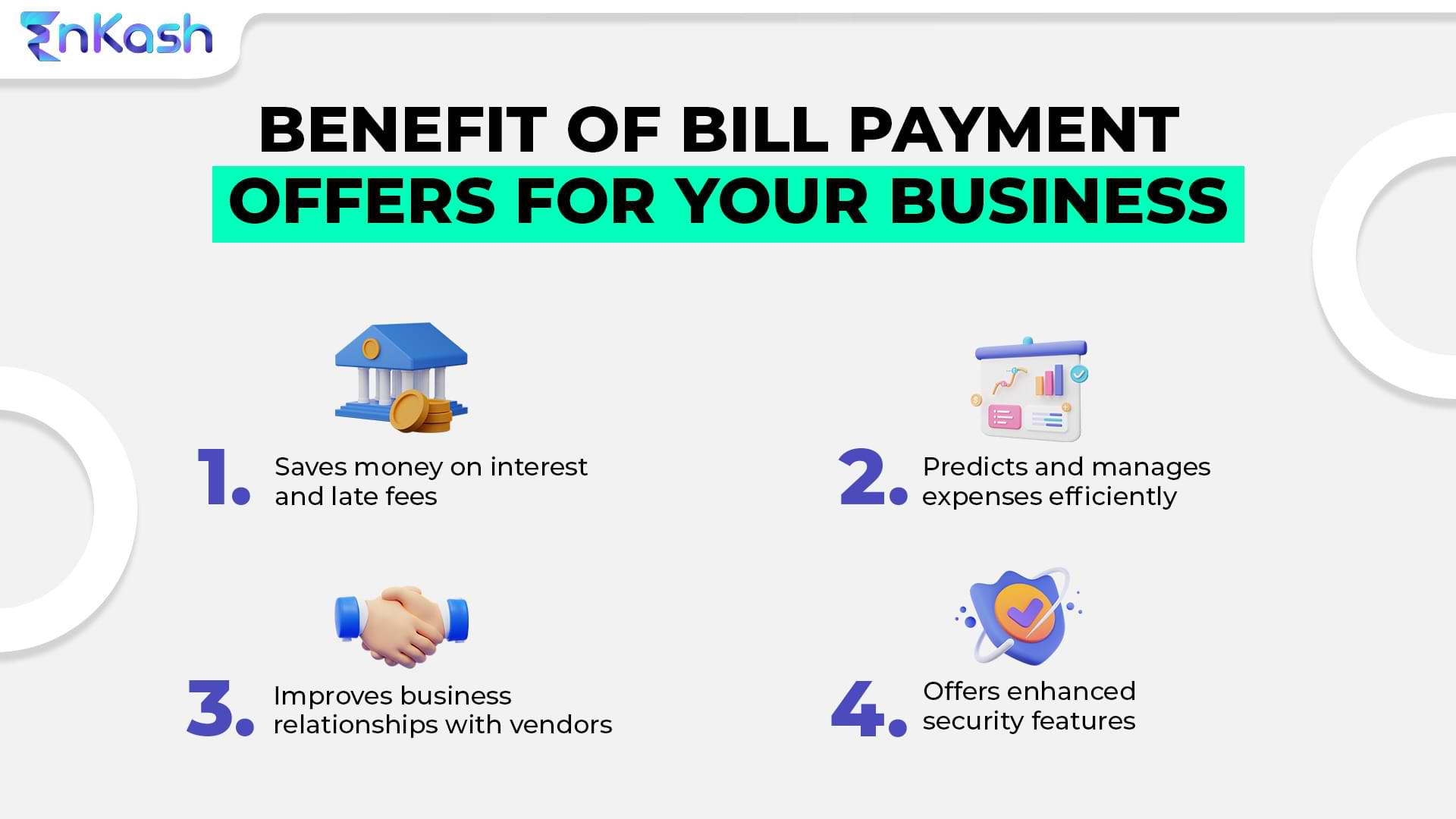

The adage “a stitch in time saves nine” holds profound truth in the context of bills payment. Timely payment is paramount for several reasons. Firstly, it prevents late fees and penalties, which can quickly accumulate and erode one’s financial resources. These fees are often substantial and can turn an affordable bill into a burdensome expense. Secondly, for obligations like loan repayments and credit cards, timely payments are crucial for maintaining a positive credit score. A strong credit score is vital for accessing future financing, securing favorable interest rates, and even for certain rental agreements or job applications. Thirdly, consistent payments ensure uninterrupted access to essential services like electricity, water, internet, and phone service, which are integral to daily life and business operations. Lastly, it significantly reduces financial stress and anxiety, fostering a sense of control over one’s finances.

Common Types of Bills

Bills can be broadly categorized in several ways, helping individuals and businesses to better understand and manage their financial outflow.

- Fixed vs. Variable Bills: Fixed bills, such as rent/mortgage payments, loan installments, and many subscription services, typically remain the same amount each month, making them easier to budget for. Variable bills, like utility bills (electricity, water, gas) or credit card statements, fluctuate based on usage or spending, requiring more dynamic budgeting.

- Recurring vs. One-time Bills: Most bills are recurring, appearing monthly, quarterly, or annually. One-time bills might include a repair service, a medical co-pay, or a specific purchase.

- Essential vs. Discretionary Bills: Essential bills cover necessities for living (housing, utilities, transportation, basic communication), while discretionary bills are for non-essential services or luxuries (streaming services, gym memberships, entertainment subscriptions). Prioritizing essential bills is a key budgeting strategy.

Traditional vs. Modern Methods of Bills Payment

The landscape of bills payment has undergone a significant transformation, evolving from manual, paper-based processes to highly automated digital solutions. This evolution has brought about unprecedented convenience and efficiency, fundamentally altering how individuals and businesses manage their financial obligations.

Traditional Approaches

For decades, traditional methods were the standard. Paying bills often involved mailing a physical check, visiting a bank branch or dedicated payment center, or making a phone payment. While still available and preferred by a segment of the population, particularly for reasons of familiarity or lack of digital access, these methods present several drawbacks. They are time-consuming, involve physical trips, carry risks like mail delays or lost checks, and often provide less immediate proof of payment. For businesses, handling numerous paper checks manually can be an administrative burden.

Modern Digital Solutions

The advent of the internet and mobile technology has revolutionized bills payment. Modern digital solutions offer unparalleled convenience, speed, and security features.

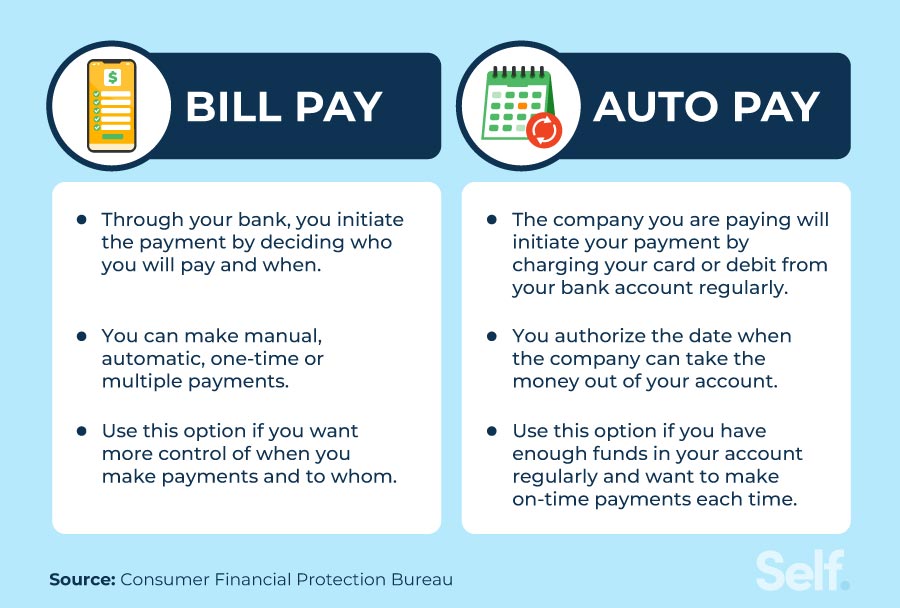

- Online Banking Portals: Most financial institutions provide robust online platforms where customers can view bills, schedule payments, and manage payees. This allows for direct debit from a checking or savings account.

- Direct Debit/Auto-Pay: This highly automated method authorizes the biller to automatically withdraw the payment amount from your bank account on the due date. It minimizes the risk of missed payments and late fees, offering peace of mind. However, it requires careful monitoring to ensure sufficient funds are available and to catch any erroneous charges.

- Mobile Payment Apps: Many banks and third-party financial apps now offer mobile bill payment functionalities, allowing users to pay bills directly from their smartphones, often with features like bill reminders and payment tracking.

- Third-Party Payment Platforms: Services like PayPal, Venmo (for certain billers), or dedicated bill payment services (e.g., Doxo, often for a fee) consolidate various bills into a single platform, offering a unified payment experience.

The shift to digital solutions offers numerous advantages: convenience of paying anytime, anywhere; faster processing; enhanced security features like encryption and fraud monitoring; and easily accessible digital records for financial tracking and reconciliation.

The Shift Towards Automation

Automation, primarily through direct debit and auto-pay, represents a significant stride in financial management. For individuals, it frees up mental bandwidth, ensuring critical bills are never forgotten. For businesses, it streamlines accounts payable, reducing administrative overhead and ensuring continuity of services. However, this convenience comes with a caveat: diligent oversight is still necessary. Automated payments should be regularly reviewed to check for incorrect charges, subscription services that are no longer needed, or changes in bill amounts that might signal an issue. Without this oversight, automation can lead to paying for services unnecessarily or overlooking billing errors.

Strategic Bills Payment for Financial Health

Effective bills payment is not merely a reactive task; it’s a proactive strategy for cultivating robust financial health. By integrating bill management into broader financial planning, individuals and businesses can optimize cash flow, protect assets, and build a secure financial future.

Budgeting and Bills Integration

A core principle of sound financial management is budgeting, and bills must be meticulously integrated into this framework. For individuals, this means allocating specific portions of income to cover all recurring expenses, ensuring that funds are available when payments are due. Techniques like the 50/30/20 rule (50% for needs, 30% for wants, 20% for savings/debt repayment) or zero-based budgeting can help. For businesses, bills payment is a critical component of cash flow management, requiring precise forecasting to ensure liquidity and avoid operational disruptions. Prioritization is key; essential bills (housing, utilities) should always take precedence over discretionary spending.

Avoiding Late Fees and Penalties

The financial cost of late fees and penalties can be surprisingly high, acting as a drain on resources that could otherwise be saved or invested. Strategies to avoid these include:

- Setting Reminders: Utilize calendar apps, financial planning tools, or simple sticky notes to remind you of upcoming due dates.

- Using Auto-Pay: As discussed, this is highly effective for recurring bills, but always monitor the account.

- Creating a Payment Calendar: Dedicate a specific day or two each month to review and pay all bills. This routine ensures nothing is missed.

- Contacting Billers: If you anticipate difficulty making a payment, proactively contact the biller. Many are willing to offer extensions or alternative payment arrangements rather than letting an account go into default.

Impact on Credit Score

For personal finance, consistent and timely payments, especially for credit cards, loans (mortgage, auto, student, personal), and sometimes utilities, have a direct and significant impact on one’s credit score. A strong payment history is the most crucial factor in building a positive credit profile. Conversely, missed or late payments can severely damage a credit score, making it harder and more expensive to borrow money in the future. A good credit score is a valuable financial asset, enabling access to better interest rates on loans, favorable insurance premiums, and even smoother rental application processes.

Managing Cash Flow

Effective bills payment is central to managing cash flow, both personally and for businesses. For individuals, it means structuring payments in a way that aligns with income cycles, ensuring there are always sufficient funds in the bank account to cover upcoming expenses without overdrawing. This might involve scheduling certain bills for the first half of the month and others for the second, depending on when paychecks arrive. For businesses, optimizing payment schedules can mean negotiating payment terms with suppliers, taking advantage of early payment discounts, or strategically delaying payments (within terms) to maintain healthy working capital and improve liquidity. The goal is to avoid periods of cash scarcity while still meeting all obligations.

Tools and Best Practices for Efficient Bills Management

In an increasingly complex financial world, leveraging the right tools and adopting smart practices can transform bills payment from a chore into a seamless aspect of financial life.

Financial Planning Software & Apps

The market is rich with digital tools designed to simplify financial management. Applications like Mint, YNAB (You Need A Budget), Personal Capital, or even specialized budgeting features within banking apps, can help track expenses, categorize spending, set budgets, and crucially, provide bill reminders. These tools offer a consolidated view of one’s financial landscape, making it easier to identify trends, potential issues, and areas for improvement. For businesses, accounting software like QuickBooks or Xero integrates accounts payable modules that streamline bill processing and payment.

Creating a Bills Payment System

Beyond relying on apps, developing a personal or business bills payment system is a best practice. This could be as simple as a dedicated spreadsheet where you list all recurring bills, their due dates, amounts, and payment methods. The goal is to establish a routine: for example, dedicating the 1st and 15th of each month to reviewing and paying bills. This systematic approach reduces the likelihood of oversights and fosters a sense of control. For businesses, standard operating procedures for invoice processing and payment authorization are essential.

Emergency Funds and Bills

An often-overlooked but critical aspect of bills payment is the role of an emergency fund. Life is unpredictable; unexpected expenses (medical emergencies, car repairs) or income disruptions (job loss, business slowdown) can suddenly make it difficult to pay regular bills. A robust emergency fund, typically covering 3-6 months of essential living expenses (including bills), acts as a financial safety net, providing a buffer during challenging times and preventing a cascade of late payments and financial distress.

Reviewing Bills Regularly

Simply paying bills isn’t enough; regular review is essential. This means scrutinizing each statement for errors, understanding usage patterns (especially for variable bills like utilities), and identifying opportunities for savings. Are you paying for a streaming service you no longer use? Can you negotiate a better rate with your internet provider? Is there a billing error that needs to be disputed? Proactively reviewing bills can uncover significant savings and ensure you’re not paying more than necessary or for services you don’t receive.

Conclusion

“What is bills payment?” is a question that leads to a comprehensive understanding of a foundational financial process. It is the steady heartbeat of personal and business finance, influencing solvency, creditworthiness, and peace of mind. By embracing timely payments, leveraging modern digital tools, integrating bill management into a broader financial strategy, and maintaining diligent oversight, individuals and businesses can transform this essential responsibility into a powerful lever for achieving enduring financial stability and prosperity. Effective bills payment is not just about moving money; it’s about building a resilient and secure financial future.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.