In the intricate world of global commerce and business finance, the seamless flow of goods and services relies heavily on robust financial instruments that guarantee payment and manage risk. Among these, the “Bill of Exchange” stands as one of the most venerable and essential tools. Despite the rise of digital banking and blockchain-based smart contracts, the Bill of Exchange remains a cornerstone of international trade and short-term financing.

This article explores the mechanics of the Bill of Exchange, its strategic importance in corporate liquidity, and how it serves as a bridge between buyers and sellers across the globe.

1. The Anatomy of a Bill of Exchange

At its core, a Bill of Exchange (BoE) is a written, unconditional order used primarily in international trade that binds one party to pay a fixed sum of money to another party on demand or at a predetermined future date. Unlike a promissory note, which is a promise to pay, a bill of exchange is an order to pay.

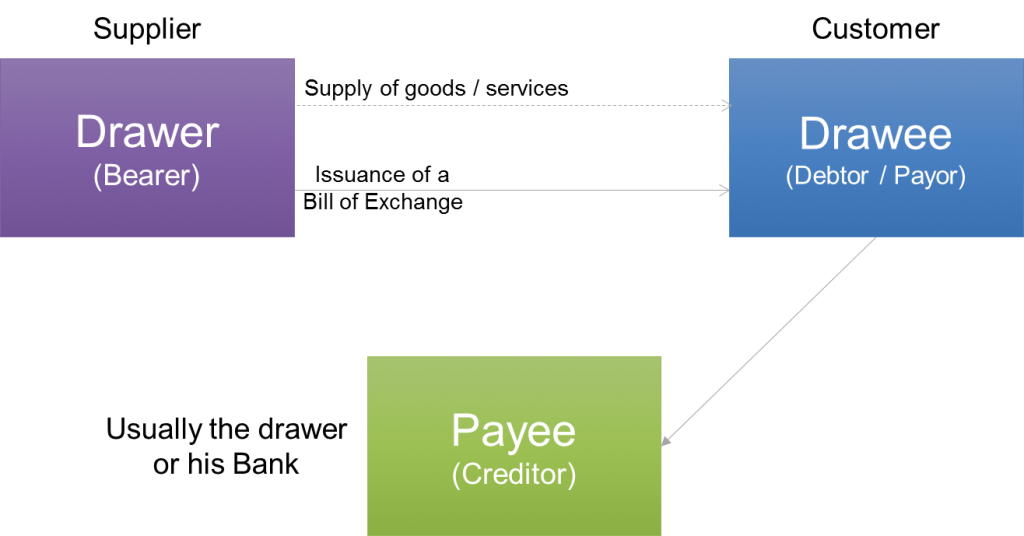

The Three Essential Parties

To understand how a Bill of Exchange functions within business finance, one must first identify the three primary stakeholders involved in the instrument:

- The Drawer: This is the party that issues or “draws” the bill. In a typical trade transaction, the drawer is the seller or exporter who is owed money for goods provided.

- The Drawee: This is the party to whom the order to pay is directed. In trade, this is usually the buyer or importer. Once the drawee signs the bill, they become the “acceptor,” legally committing to the debt.

- The Payee: This is the party who will receive the payment. While the drawer and the payee are often the same person (the seller), the drawer can designate a third party, such as a bank, to be the payee.

Key Components of a Valid Instrument

For a Bill of Exchange to be legally binding and negotiable in the financial markets, it must contain specific elements. These include a clear statement that it is a “Bill of Exchange,” the exact sum of money to be paid, the date of maturity (when payment is due), the signature of the drawer, and the name of the drawee. Because it is a “negotiable instrument,” it can be transferred to other parties, making it a liquid asset in a company’s portfolio.

2. How the Bill of Exchange Facilitates Global Trade

The primary utility of a Bill of Exchange lies in its ability to mitigate risk and bridge the trust gap between parties who may be operating in different legal jurisdictions. In the “Money” niche of international finance, it acts as a formalization of credit.

The Acceptance Process

A Bill of Exchange is often “unaccepted” when it is first sent along with shipping documents. The transaction becomes legally binding once the drawee (the buyer) writes “accepted” across the face of the document and signs it. This transformation from a mere request to a legal obligation allows the seller to treat the document as an asset. In many cases, a bank may act as the drawee (a Banker’s Acceptance), adding its own creditworthiness to the document, which significantly reduces the risk of default.

Bridging the Trust Gap in International Commerce

In international trade, sellers are often hesitant to ship goods without payment, while buyers are hesitant to pay before receiving goods. The Bill of Exchange, often used in conjunction with a Letter of Credit, solves this dilemma. It provides the seller with a document that can be legally enforced or even sold for cash before the buyer actually pays, while allowing the buyer a credit period to receive and sell the goods before the bill matures.

3. Categorizing Bills of Exchange in Business Finance

Not all Bills of Exchange are created equal. Depending on the geographical location of the parties and the timing of the payment, they fall into several distinct categories that financial managers must understand.

Inland vs. Foreign Bills

An Inland Bill is drawn and payable within the same country, or drawn upon a resident of that country even if payable elsewhere. Conversely, a Foreign Bill is used for international transactions where the parties are located in different countries. Foreign bills are typically drawn in sets of three to ensure that at least one reaches the destination despite potential postal delays or losses.

Demand vs. Time (Usance) Bills

The timing of payment is a critical factor in cash flow management. A Demand Bill (or Sight Bill) is payable immediately upon presentation to the drawee. There is no grace period. A Time Bill (or Usance Bill), however, specifies a future date for payment—for example, “90 days after sight.” This gives the buyer time to generate revenue from the purchased goods to cover the cost of the bill.

Trade vs. Accommodation Bills

Most bills arise from genuine commercial transactions involving the sale of goods; these are known as Trade Bills. However, there is a unique financial tool known as an Accommodation Bill. This is drawn and accepted not because of a debt owed, but to provide financial assistance to one of the parties. Essentially, it is a way for two parties to “lend” their credit to each other to raise funds from a bank.

4. Strategic Financial Advantages: Liquidity and Discounting

For a business, a Bill of Exchange is more than just a piece of paper; it is a tool for working capital management. In the realm of business finance, the ability to turn a future payment into immediate cash is invaluable.

Discounting for Immediate Working Capital

One of the most powerful features of a Bill of Exchange is Discounting. If a seller holds a Time Bill due in 90 days but needs cash immediately to pay suppliers or payroll, they can take the accepted bill to a bank. The bank will purchase the bill at a price slightly lower than its face value (the “discount”). The difference represents the interest the bank earns for advancing the funds. This allows the business to maintain liquidity without waiting for the credit period to expire.

Negotiation and Endorsement

Because these are negotiable instruments, they can be used to settle debts between multiple parties. A seller can “endorse” a bill (sign the back) and pass it to their own creditor to settle a debt. This “negotiability” makes the Bill of Exchange a form of private currency within the business community, facilitating a chain of transactions without the immediate need for liquid cash.

5. Risk Management and Legal Frameworks

While the Bill of Exchange is a powerful tool, it carries inherent risks, primarily the risk of non-payment. Financial professionals must be adept at handling “dishonored” bills and understanding the legal protections available.

Handling the Dishonor of a Bill

A bill is “dishonored” if the drawee refuses to accept it or fails to pay it upon maturity. When this happens, the holder must follow a strict legal process to maintain their right to sue the drawer or previous endorsers. This usually involves “Noting” and “Protesting.” A Notary Public officially records the refusal to pay, providing legal evidence of the dishonor. This step is crucial for businesses looking to recover funds through the judicial system.

Comparing Bills of Exchange with Promissory Notes

In business finance, it is common to confuse Bills of Exchange with Promissory Notes. While both are negotiable instruments, the Bill of Exchange involves three parties and is an order to pay, whereas a Promissory Note involves two parties and is a promise to pay. From a creditor’s perspective, a Bill of Exchange is often preferred in trade because it can be “accepted” by a bank, significantly elevating its security and marketability compared to a private promise from an individual buyer.

Conclusion

The Bill of Exchange remains a fundamental instrument in the “Money” and business finance sector. Its ability to provide security, facilitate credit, and offer immediate liquidity through discounting makes it an indispensable tool for companies engaged in both domestic and international trade. By mastering the nuances of drawers, drawees, and discounting, financial managers can better navigate the complexities of global commerce, ensuring that their organizations remain liquid, solvent, and ready for growth. Whether you are a small business owner or a corporate treasurer, understanding the mechanics of this instrument is key to effective financial strategy.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.