The term “bi-monthly” is one of the most frequently misunderstood concepts in personal and business finance. Because the prefix “bi-” can imply both “twice per” and “every two,” it often leads to confusion regarding when money is actually changing hands. In the context of finance, payroll, and billing cycles, understanding the cadence of these payments is essential for effective cash flow management, budgeting, and debt repayment strategies.

Deciphering the Bi-Monthly Schedule

At its core, a bi-monthly payment schedule signifies that a transaction occurs twice a month. While this might seem straightforward, the lack of a standardized interval creates nuances that can impact how you balance your checkbook or plan your business expenses.

The Standard Twice-a-Month Model

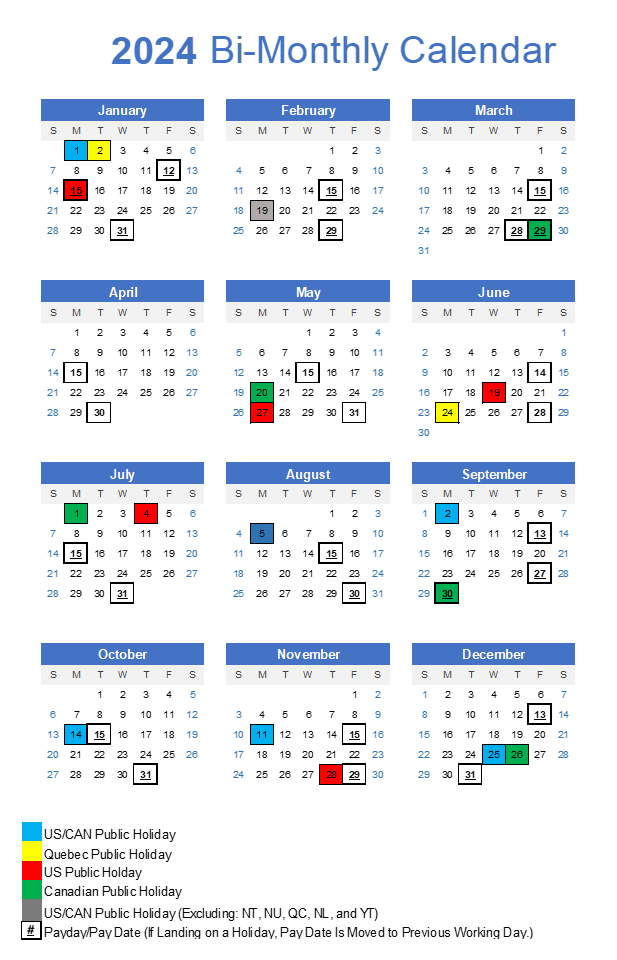

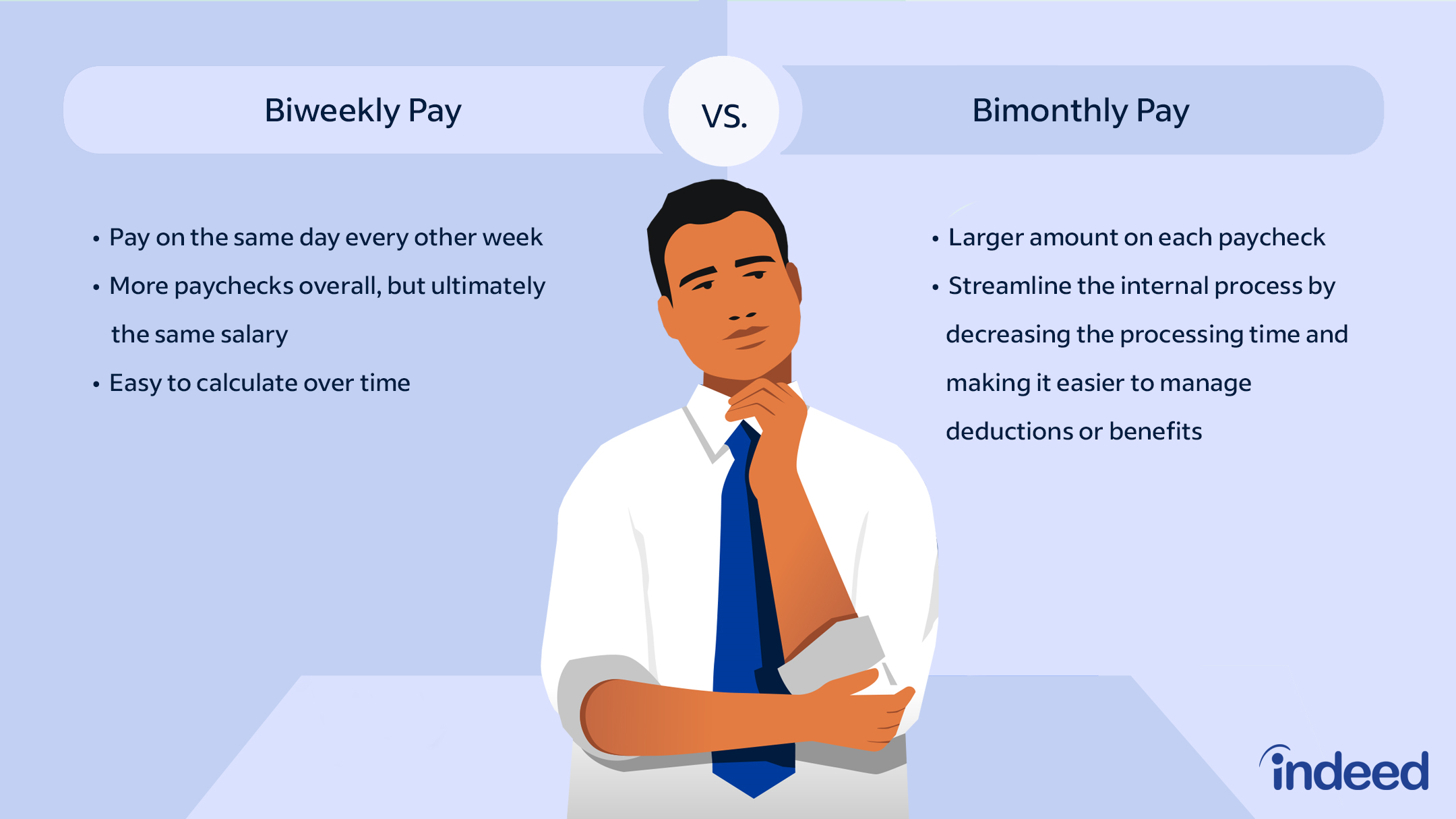

In most payroll and billing systems, a bi-monthly payment schedule is defined by two specific dates within the month—for example, the 1st and the 15th, or the 15th and the 30th. This is distinct from “bi-weekly” payments, which occur every two weeks, resulting in 26 pay periods per year. A true bi-monthly schedule typically results in exactly 24 payments per year.

Why the Distinction Matters

Confusing bi-monthly with bi-weekly is a common pitfall. If you are an employer setting up a payroll system or a consumer automating a loan payment, choosing the wrong interval can lead to significant discrepancies. A bi-weekly schedule results in two months out of every year where three pay periods occur, whereas a bi-monthly schedule provides a consistent, predictable two payments every month, regardless of the number of weeks in that month.

Financial Implications for Individuals

For the average consumer, understanding your payment frequency is the foundation of a healthy budget. Whether you are paying down a mortgage, managing a subscription service, or receiving a salary, knowing exactly when money leaves or enters your account allows for proactive rather than reactive financial management.

Impact on Debt Repayment

Many lenders offer bi-monthly payment options to help borrowers pay off loans faster. By splitting a monthly mortgage or auto loan payment into two, you technically make one full payment per month, but the timing can be leveraged to reduce the interest accrued on the principal balance. However, if the lender requires the full payment to be held until the second half is received, the interest savings may be negligible. It is vital to read the terms of service to ensure that your bi-monthly payments are applied to the principal as soon as they are received.

Cash Flow and Budgeting

When your income follows a bi-monthly schedule, your budgeting strategy should align with those specific dates. For instance, if your rent is due on the 1st, but your second payment of the month arrives on the 15th, you are left with a 15-day gap where your liquidity is at its lowest. Mapping your fixed expenses—utilities, rent, insurance—to your bi-monthly pay dates prevents “account bloat” or accidental overdrafts. By aligning your outflows with these two distinct income spikes, you ensure that you aren’t spending money that is effectively “earmarked” for a bill due later in the month.

Business and Payroll Considerations

For business owners and human resources departments, the bi-monthly pay cycle (often referred to as semi-monthly) is a popular choice for balancing administrative workload with employee satisfaction.

Administrative Advantages

Compared to weekly or bi-weekly payroll, the semi-monthly (bi-monthly) model is often preferred by accounting departments because it aligns perfectly with the calendar month. It simplifies the calculation of monthly benefits, taxes, and year-end reporting. Since every month has 24 pay periods, the salary amount remains constant, making it easier to project cash flow and manage overhead costs without the complexity of “three-paycheck months” that occur in bi-weekly systems.

Employee Perception

While employers favor the predictability of 24 pay periods, employees sometimes feel differently. Because there are only two paychecks per month, the interval between payments is longer than it would be in a weekly or bi-weekly structure. This can lead to difficulties for employees living paycheck to paycheck, as they must stretch their resources over a longer period. Companies choosing this frequency should ensure that their compensation packages remain competitive and consider offering financial wellness resources to help staff manage the longer wait times between paydays.

Compliance and Tax Reporting

The Internal Revenue Service (IRS) and other tax authorities operate on a monthly and quarterly basis. A bi-monthly payment schedule is highly compatible with these tax cycles. Businesses can easily withhold and remit payroll taxes twice a month, aligning their internal ledger with external tax obligations. This reduces the margin for error and simplifies the reconciliation process when filing quarterly returns, ultimately saving time and reducing the cost of accounting services.

Strategic Financial Planning with Payment Cycles

Whether you are managing your personal finances or running a corporation, the “bi-monthly” label is a tool to be wielded with precision. Mastering the timing of your money is just as important as the amount of money you have.

Maximizing Efficiency

To maximize the benefits of a bi-monthly system, consider the following strategies:

- Synchronization: Sync your automated bill payments to occur 24 to 48 hours after your income deposits. This “just-in-time” approach prevents funds from sitting stagnant and reduces the temptation to overspend.

- Buffer Creation: Use the consistency of the 24-payment-per-year model to build a “buffer” account. Since you know exactly how many payments you will receive, you can calculate the variance between your total monthly income and your total monthly expenses. Any surplus should be diverted into a high-yield savings account or an investment vehicle immediately upon receipt.

- Emergency Planning: If you encounter a situation where expenses exceed your twice-monthly income, the bi-monthly schedule allows you to clearly identify which specific payment window is underfunded. This clarity makes it much easier to adjust your discretionary spending rather than guessing where the budget is failing.

Avoiding Common Pitfalls

The biggest mistake individuals and businesses make is assuming that all “bi-” terms are interchangeable. Always check your contracts and payroll agreements to confirm the frequency. If a vendor states “bi-monthly,” ask for specific dates. If a loan agreement mentions a “bi-monthly payment option,” clarify whether those payments are applied to the principal immediately or held in a suspense account.

By treating the bi-monthly payment schedule as a structured rhythm rather than a vague approximation, you gain significant control over your financial narrative. You shift from a state of wondering when your next infusion of capital will arrive to one of precise, calendar-based execution.

Ultimately, money is a tool, and like any tool, its effectiveness depends on the precision with which it is used. Whether you are optimizing a payroll department, paying down a mortgage, or simply balancing your household accounts, the bi-monthly payment framework offers a reliable, steady, and manageable cadence. By understanding the underlying mechanics of this schedule, you can eliminate the anxiety of “end-of-month” crunches and move toward a more stable and strategic financial future.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.