In the rapidly evolving landscape of digital commerce, the ability to process payments is the lifeblood of any business. However, for a significant segment of entrepreneurs, securing a reliable payment gateway is not as simple as signing up for a standard merchant account. Many businesses find themselves categorized as “high-risk” by traditional financial institutions, leading to frozen funds, sudden account closures, and rejected applications. This is where Bankful enters the frame.

Bankful is a sophisticated financial technology platform designed specifically to bridge the gap between complex business models and the banking systems required to sustain them. Formerly known as Pinwheel, Bankful has rebranded and expanded its capabilities to provide robust, secure, and flexible payment processing solutions. This guide explores the intricacies of Bankful, its role in the financial ecosystem, and how it empowers businesses that traditional banks often overlook.

Understanding Bankful: The Bridge Between High-Risk Merchants and Financial Stability

To understand what Bankful is, one must first understand the problem it solves. Traditional payment processors like Stripe, PayPal, and Square have strict terms of service and automated risk assessment algorithms. If a business operates in an industry with high chargeback rates, complex legal regulations, or perceived reputational risk, these “aggregator” services will often terminate the merchant’s account with little to no notice.

From Pinwheel to Bankful: A Brief History

The transition from Pinwheel to Bankful was more than just a name change; it was a strategic pivot toward becoming a comprehensive financial suite. While Pinwheel was primarily known as a gateway that integrated with Shopify to allow high-risk transactions, Bankful has evolved into a full-scale payment orchestration platform. This evolution reflects the growing need for merchants to have more control over their financial data and a more direct relationship with multiple acquiring banks.

The Core Mission: Solving the “High-Risk” Dilemma

Bankful’s primary mission is to provide “frictionless” commerce for industries that typically face significant friction. By leveraging deep relationships with a global network of banks, Bankful allows merchants to diversify their risk. Instead of being dependent on a single processor, Bankful users can route transactions through various channels, ensuring that even if one banking partner changes its policy toward a specific industry, the business remains operational. This redundancy is a cornerstone of modern business finance for any non-traditional enterprise.

Key Features and Financial Infrastructure

Bankful is not merely a middleman; it is a sophisticated piece of financial infrastructure that provides tools for scaling, security, and global expansion. For a business owner, the platform acts as a command center for all incoming revenue streams.

Seamless E-commerce Integrations

One of the most significant hurdles for high-risk merchants is the lack of compatibility between specialized payment gateways and popular e-commerce platforms. Bankful solves this by offering deep, native-like integrations with Shopify, WooCommerce, Magento, and BigCommerce. For example, Shopify’s internal payment processor (Shopify Payments) prohibits various products, ranging from supplements to certain digital goods. Bankful allows these merchants to continue using Shopify’s powerful storefront tools while bypassing the restrictive payment limitations.

Advanced Fraud Protection and Security Protocols

In the world of high-risk finance, fraud is the most significant threat to a merchant’s “good standing” with a bank. High chargeback ratios can lead to heavy fines or the permanent loss of a merchant account. Bankful addresses this through an integrated suite of fraud mitigation tools.

- 3D Secure 2.0: This protocol provides an additional layer of authentication for credit and debit card transactions, significantly reducing the likelihood of fraudulent “card-not-present” transactions.

- Real-time Monitoring: The platform uses machine learning to identify suspicious purchasing patterns, allowing merchants to void or refund risky orders before they result in a formal dispute.

Multi-Currency Support for Global Scaling

For businesses looking to maximize their online income, the ability to sell internationally is vital. Bankful provides multi-currency support, allowing customers to pay in their local currency while the merchant receives settlements in their preferred denomination. This feature is crucial for businesses in the digital goods or travel sectors, where the customer base is inherently global. By handling the complexities of currency conversion and international banking regulations, Bankful simplifies the financial logistics of global expansion.

Why Traditional Banks Say No and Bankful Says Yes

![]()

A common question among entrepreneurs is why their business is labeled “high-risk” in the first place. Understanding this categorization is essential for managing a company’s financial health and long-term viability.

Defining High-Risk Industries

The financial sector categorizes businesses as high-risk based on two main factors: financial risk (high chargeback rates) and regulatory risk (complex laws). Common industries served by Bankful include:

- Nutraceuticals and Supplements: These often face high return rates and strict FDA-related advertising rules.

- Digital Goods and Subscriptions: Because there is no physical “proof of delivery,” these transactions are more susceptible to “friendly fraud” where customers claim they never authorized the purchase.

- CBD and Hemp: Despite federal legalization in many jurisdictions, many banks remain wary of the shifting legal landscape.

- Gaming and Fantasy Sports: These industries involve complex state-by-state regulations that standard processors are unwilling to navigate.

The Risk Mitigation Engine

Bankful says “yes” where others say “no” because they employ a more nuanced underwriting process. While a company like Stripe uses broad algorithms to mass-filter merchants, Bankful looks at the individual business’s history, fulfillment processes, and chargeback management strategies. They provide the merchant with the tools to prove their reliability to the banking partners. Essentially, Bankful acts as a financial advocate, presenting the merchant’s data in a way that satisfies the risk departments of major acquiring banks.

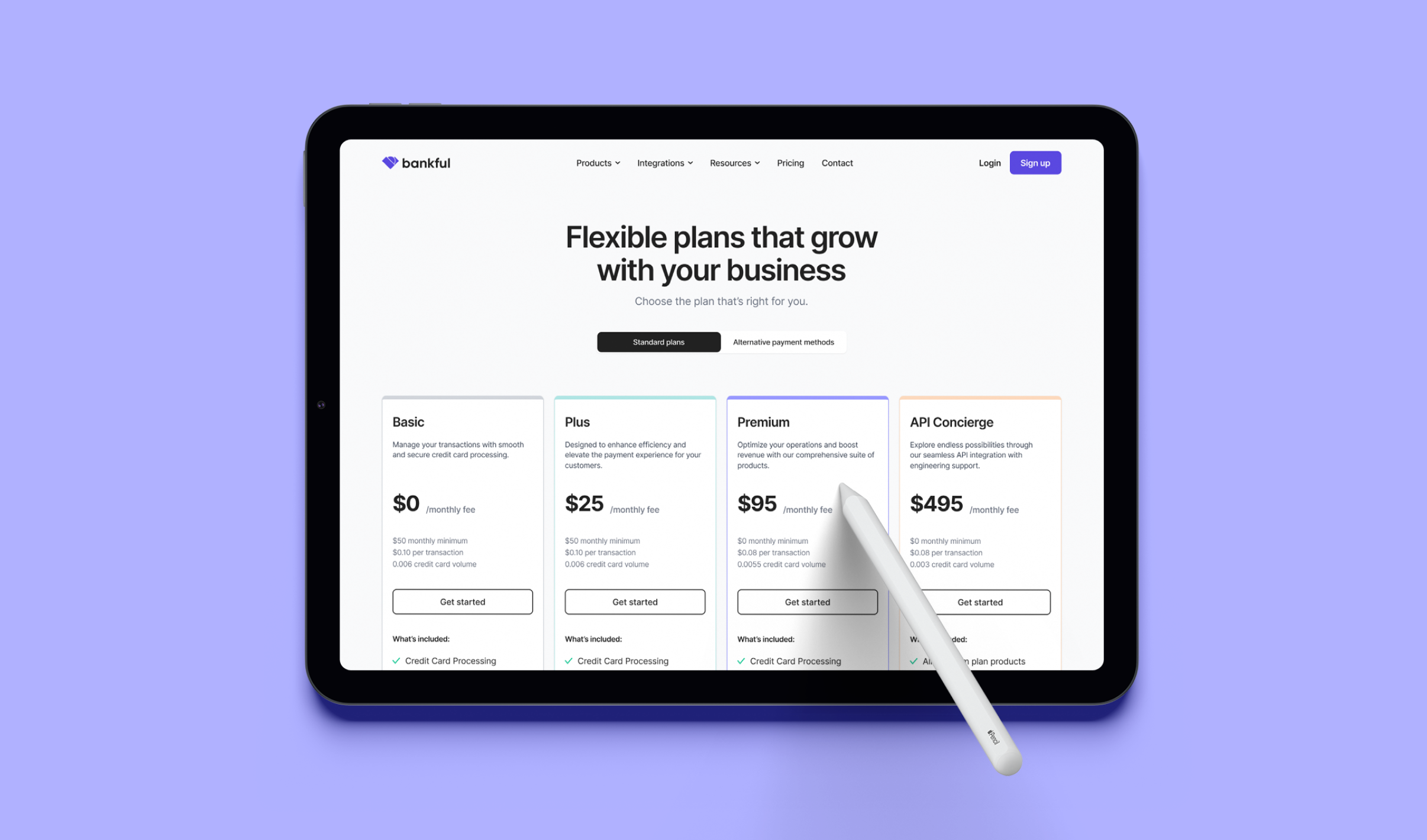

Navigating the Bankful Ecosystem: Pricing and Setup

Choosing a financial tool is as much about the “bottom line” as it is about features. In business finance, the cost of processing is a critical variable in calculating profit margins.

Transparent Fee Structures

It is a reality of the financial world that high-risk processing costs more than low-risk processing. Because the banks are taking on more perceived danger, they charge higher percentages per transaction. Bankful differentiates itself by offering more transparency than many “boutique” high-risk processors who often hide fees in complex contracts.

Bankful typically operates on a model that includes a monthly gateway fee, a per-transaction fee, and a percentage of the total sale. While these rates are higher than the standard 2.9% + $0.30 seen in the low-risk world, the value lies in the stability of the account. For a business owner, paying 4.5% for an account that stays open is infinitely better than paying 2.9% for an account that gets shut down and freezes $50,000 in capital for six months.

The Onboarding Process for New Businesses

Setting up a Bankful account is more involved than setting up a standard processor, reflecting the “due diligence” required in high-stakes finance. Applicants must provide:

- Business Documentation: Articles of incorporation and tax IDs.

- Processing History: Usually 3–6 months of previous processing statements to prove chargeback ratios are under control.

- Financial Statements: To ensure the business has enough liquidity to cover potential refunds.

- Operational Transparency: A clear look at the website’s refund policies, terms of service, and shipping timelines.

Once approved, the Bankful dashboard provides a centralized view of all financial activity, allowing for streamlined reconciliation and reporting.

The Future of High-Risk Business Finance

As the digital economy grows, the definition of “high-risk” is constantly shifting. Innovation often moves faster than regulation, meaning many legitimate, high-growth businesses will continue to find themselves outside the comfort zone of traditional banks.

Adapting to Regulatory Changes

The financial world is currently grappling with the rise of crypto-assets, evolving privacy laws, and new international trade agreements. Platforms like Bankful are positioned to act as a buffer for merchants. By staying ahead of compliance requirements—such as GDPR in Europe or the varying CBD laws in the US—Bankful ensures that its merchants don’t have to become legal experts just to accept a payment.

The Role of AI in Transaction Monitoring

Looking ahead, the integration of Artificial Intelligence into Bankful’s financial suite will likely be the next frontier. AI can move beyond simple “if/then” rules for fraud and begin to predict liquidity crises or identify untapped revenue opportunities based on transaction flow patterns. For the modern entrepreneur, Bankful is evolving from a mere payment gateway into a comprehensive financial partner that offers the stability needed to turn a “high-risk” venture into a long-term commercial success.

In conclusion, Bankful is an essential tool for the modern merchant operating in the “gray areas” of commerce. By providing a stable, secure, and highly integrated financial platform, it allows business owners to focus on what they do best: building their brand and serving their customers, without the constant fear of financial de-platforming. Whether you are selling specialized supplements or high-ticket digital services, understanding and utilizing a platform like Bankful is a strategic move toward financial resilience.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.