Navigating the complexities of a mortgage can be a daunting task for many homebuyers. Beyond the excitement of finding the perfect property, there’s a labyrinth of financial terms and figures to understand. Among the most crucial, yet often misunderstood, concepts is the Annual Percentage Rate (APR). While many focus solely on the interest rate, the APR offers a more comprehensive and standardized view of the true cost of borrowing for your home. It’s a vital tool designed to help consumers make informed decisions, ensuring transparency in the lending process. Understanding what APR represents, how it differs from the nominal interest rate, and what components contribute to its calculation is fundamental to selecting the right mortgage product for your financial future. This article will delve deep into the intricacies of APR in the context of mortgages, empowering you with the knowledge to confidently compare loan offers and secure the best possible terms for your homeownership journey.

Deconstructing the Annual Percentage Rate (APR)

The Annual Percentage Rate (APR) is more than just a number; it’s a regulatory standard designed to provide a comprehensive measure of the cost of borrowing money. While the interest rate tells you how much you’re paying on the principal amount, the APR aims to reflect the total cost over the loan’s term, incorporating various fees and charges that are often overlooked.

Beyond the Interest Rate: What APR Truly Represents

At its core, the APR is the true cost of your loan expressed as a yearly percentage. It’s a standardized metric that allows you to compare different loan offers on an “apples-to-apples” basis. The nominal interest rate is merely one component of this cost. Without the APR, a lender could advertise an attractively low interest rate, only to recoup their costs through exorbitant fees hidden in the fine print. The APR’s purpose is to pull back the curtain on these hidden costs, providing a more transparent picture of the financial commitment you’re undertaking. It essentially takes all the upfront costs associated with getting the loan and spreads them out over the life of the loan, adding them to the interest rate to give you a single, all-encompassing percentage.

Key Components Included in APR Calculation

To arrive at the APR, several elements are factored in, painting a holistic picture of borrowing expenses. These components typically include:

- The Interest Rate: This is the primary component and the most straightforward. It’s the percentage charged by the lender for the use of the borrowed money.

- Lender Fees: These are charges directly from the mortgage lender for processing and underwriting your loan. They can include origination fees (a percentage of the loan amount), underwriting fees, application fees, and processing fees.

- Mortgage Broker Fees: If you’re using a mortgage broker, their compensation fee is often included in the APR calculation.

- Discount Points (or Origination Points): These are optional upfront payments made to the lender in exchange for a lower interest rate. Each point typically costs 1% of the loan amount. If you pay points, they are factored into the APR.

- Private Mortgage Insurance (PMI) or FHA/VA Funding Fees: For conventional loans with less than a 20% down payment, PMI is usually required. Similarly, FHA loans have an upfront Mortgage Insurance Premium (MIP) and annual MIP, while VA loans have a funding fee. While the annual premiums are sometimes excluded from APR by some lenders, the upfront fees (like FHA’s upfront MIP or VA’s funding fee) are generally included as part of the overall cost.

It’s equally important to understand what is not typically included in the APR calculation. These usually consist of third-party closing costs such as title insurance, appraisal fees, credit report fees, attorney fees, recording fees, property taxes, and homeowner’s insurance premiums. While these are significant costs of buying a home, they are generally not considered “cost of borrowing” by regulatory standards for APR calculation.

Why APR is Crucial for Mortgage Borrowers

Understanding the APR is not just about crunching numbers; it’s about empowering borrowers to make sound financial decisions that can impact their wealth for decades. Its prominence in mortgage disclosures serves a critical purpose in promoting transparency and protecting consumers.

The “True Cost” Indicator

The most significant benefit of the APR is its ability to reveal the “true cost” of a mortgage. Imagine two lenders offering seemingly identical interest rates – say, 6.5%. Without the APR, you might assume their loans are equally good. However, one lender might have significantly higher origination fees, discount points, or other charges that dramatically increase the overall cost of the loan. The APR standardizes this comparison. If Lender A offers a 6.5% interest rate with an APR of 6.8%, and Lender B offers the same 6.5% interest rate but with an APR of 7.1%, it immediately becomes clear that Lender A’s offer is less expensive in the long run, even with the same nominal rate. This single percentage allows borrowers to quickly identify which loan is genuinely more affordable, helping them avoid being swayed by misleading low-interest rate advertisements.

Regulatory Mandate and Borrower Protection

The importance of APR is underscored by its regulatory requirement under the federal Truth in Lending Act (TILA), enacted in 1968. TILA mandates that lenders disclose the APR, along with other key loan terms, to consumers. This legislation was a landmark effort to ensure transparency in lending and protect borrowers from predatory practices where fees could be hidden or obscured. By requiring lenders to present the total cost of credit in a standardized, easily digestible format, TILA empowers consumers to compare offers from different financial institutions with confidence. This regulatory framework acts as a safeguard, ensuring that lenders are held accountable for fully disclosing the financial implications of their loan products.

Short-Term vs. Long-Term Loan Impact

The difference between the interest rate and the APR can be particularly pronounced and impactful depending on the loan term. For shorter-term loans, like a 15-year mortgage, even relatively small upfront fees can significantly inflate the APR compared to the interest rate. This is because the fixed fees are amortized over a shorter period, making their per-year impact higher. Conversely, on a longer-term loan, such as a 30-year mortgage, the same dollar amount of fees is spread out over a much longer period, resulting in a smaller difference between the interest rate and the APR. This insight is crucial when evaluating different loan durations. A low-fee, slightly higher interest rate 15-year mortgage might have a lower APR than a low-interest rate, high-fee 15-year mortgage. Understanding this dynamic helps borrowers evaluate whether paying upfront points or fees to lower the interest rate is truly beneficial given their expected tenure in the home and the loan term.

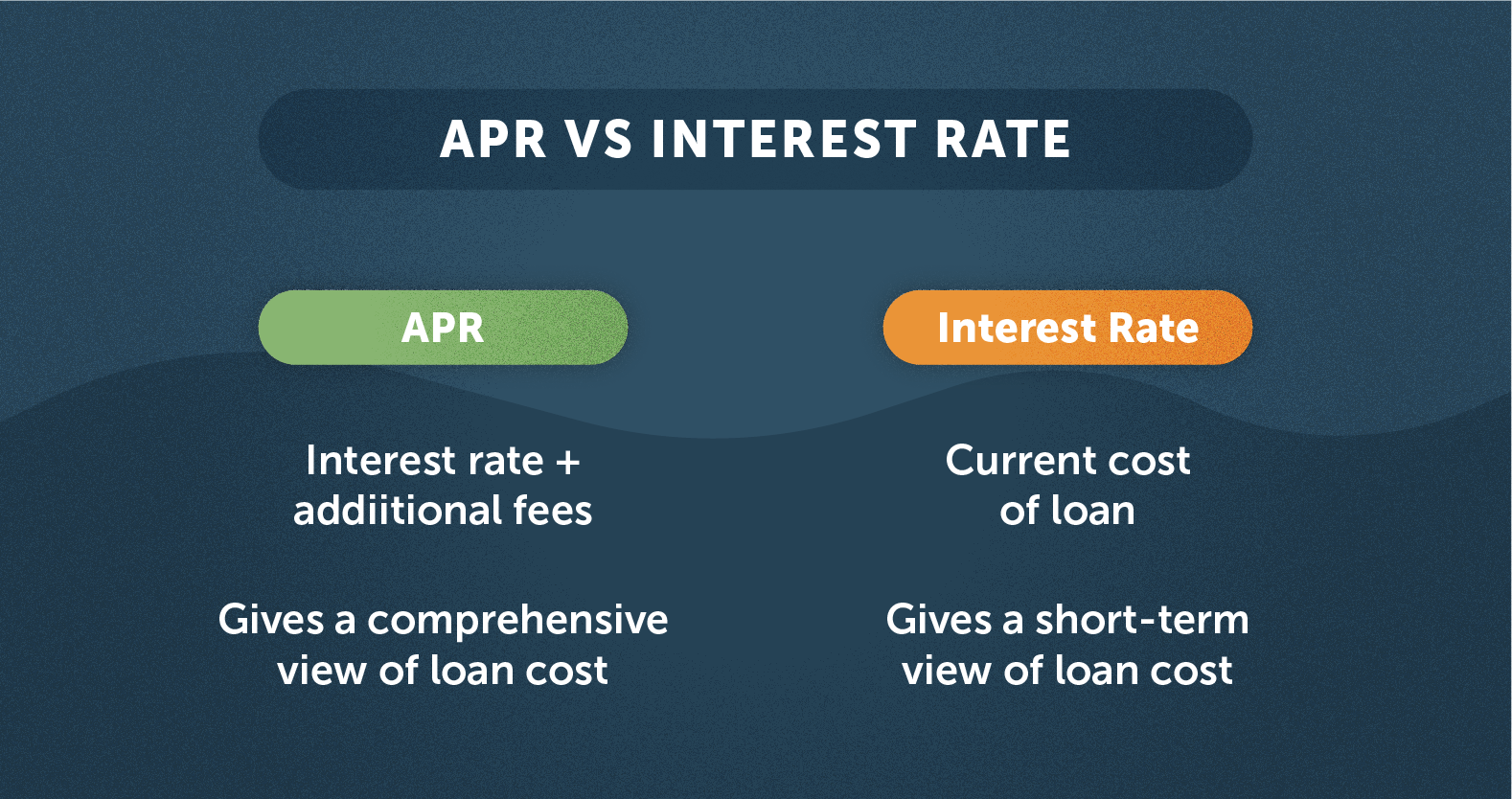

APR vs. Interest Rate: Understanding the Distinction

While often used interchangeably by the uninformed, the interest rate and the Annual Percentage Rate are distinct financial metrics, each serving a unique purpose in illustrating the cost of a mortgage. Grasping this distinction is paramount for any borrower looking to secure the best possible terms.

The Nominal Interest Rate: Cost of Borrowed Principal

The interest rate is the most straightforward and commonly cited figure in any loan discussion. It represents the percentage charged by the lender on the principal amount of money you borrow. When you make your monthly mortgage payment, a portion of that payment goes towards paying down the principal balance, and another portion goes towards covering the interest accrued on the remaining principal. This nominal interest rate dictates the size of your monthly payment for the pure cost of borrowing the money, separate from any fees involved in originating the loan itself. It’s the engine that drives the exponential growth of your total repayment over the life of the loan. For example, if you borrow $300,000 at a 6.0% interest rate, the interest rate is solely focused on the 6.0% charge on that $300,000 principal.

APR: The Holistic View of Borrowing Costs

In contrast to the interest rate, the APR offers a holistic perspective by incorporating the nominal interest rate plus many of the additional fees and charges associated with obtaining the mortgage. It effectively annualizes these upfront costs and adds them to the interest rate to provide a single, all-encompassing percentage that truly reflects the total expense of borrowing. Think of it this way: if the interest rate is the sticker price of the car, the APR is the sticker price plus the mandatory “documentation fee,” “dealer prep,” and “financing charge” that are necessary to drive the car off the lot, all expressed as an annual percentage.

For instance, if Lender A offers a 6.0% interest rate, but charges $5,000 in origination fees and discount points on a $300,000 loan, their APR might be 6.3%. Lender B, on the other hand, might also offer a 6.0% interest rate but charges only $2,000 in fees. In this scenario, Lender B’s APR could be 6.1%. Even though both lenders quote the same nominal interest rate, Lender B’s offer is demonstrably cheaper when the full cost of acquiring the loan is considered, as reflected by the lower APR. This comprehensive view ensures that borrowers aren’t blindsided by significant upfront costs that make a seemingly low-interest loan ultimately more expensive.

Factors Influencing Your Mortgage APR

The APR you’re offered on a mortgage is not a static figure; it’s a dynamic number influenced by a multitude of variables, ranging from your personal financial profile to broader market conditions and the specifics of the loan product itself. Understanding these influencing factors can help you position yourself for the most favorable terms.

Borrower-Specific Factors

Your individual financial health plays a critical role in determining the APR a lender is willing to offer. Lenders assess risk, and certain borrower characteristics indicate a lower risk, thus qualifying you for better rates and lower APRs.

- Credit Score: This is perhaps the most significant factor. A higher credit score (typically FICO scores above 740-760) signals to lenders that you are a responsible borrower with a history of timely payments, making you less of a risk. Borrowers with excellent credit generally qualify for the lowest interest rates and, consequently, the lowest APRs.

- Debt-to-Income (DTI) Ratio: Your DTI ratio compares your total monthly debt payments to your gross monthly income. A lower DTI indicates that you have ample income to manage your existing debts and a new mortgage payment, making you a more attractive borrower. Lenders typically prefer a DTI ratio below 43%, though this can vary.

- Down Payment Amount: The larger your down payment, the less money you need to borrow, and the less risk the lender assumes. A substantial down payment (e.g., 20% or more) can lead to a lower interest rate and APR. It can also help you avoid Private Mortgage Insurance (PMI) on conventional loans, further reducing your total cost of borrowing and, therefore, your APR.

- Loan-to-Value (LTV) Ratio: Directly related to the down payment, the LTV ratio compares the loan amount to the appraised value of the home. A lower LTV (meaning a higher down payment) suggests less risk for the lender, potentially resulting in better APRs.

Loan-Specific and Market Factors

Beyond your personal finances, the type of loan you choose and the prevailing economic environment also significantly shape your mortgage APR.

- Loan Type: Different mortgage products come with different risk profiles and pricing structures.

- Fixed-Rate Mortgages: Offer a stable interest rate for the life of the loan. Their APRs will reflect current market conditions and lender fees.

- Adjustable-Rate Mortgages (ARMs): Start with a lower, fixed interest rate for an initial period, which then adjusts periodically. ARM APRs are generally estimated based on the initial rate and a projected index, which can be less precise over the long term.

- Government-Backed Loans (FHA, VA, USDA): Often have more lenient qualification requirements and can offer competitive interest rates. However, they come with specific fees (like FHA’s MIP or VA’s funding fee) that will be incorporated into the APR calculation, which can sometimes make their APR higher than their nominal interest rate suggests.

- Loan Term: The length of your mortgage (e.g., 15-year vs. 30-year) influences the APR. Shorter terms typically come with lower interest rates (as lenders perceive less risk over a shorter period), which can translate to a lower APR, even if the upfront fees are the same. However, the monthly payments are higher.

- Market Interest Rates: The broader economic environment and the federal funds rate set by the Federal Reserve heavily influence market interest rates. When the Fed raises rates, mortgage rates and APRs tend to follow suit. Bond market performance also plays a significant role in mortgage pricing.

- Lender’s Profit Margins and Overheads: Each lender has its own operational costs and desired profit margins. These can subtly influence the fees they charge and, consequently, the APR they offer. Shopping around is crucial because these differences can accumulate.

- Discount Points: As mentioned earlier, paying discount points upfront allows you to “buy down” your interest rate. While this lowers the nominal interest rate, the cost of the points is factored into the APR. You need to calculate if the long-term savings from a lower interest rate outweigh the immediate cost of the points as reflected in the APR.

Navigating Mortgage Offers with APR in Mind

The power of the APR lies in its ability to standardize comparison. However, understanding its nuances and limitations is key to using it effectively as you evaluate different mortgage offers.

Comparing Apples to Apples

The primary utility of the APR is to enable a true “apples-to-apples” comparison between different mortgage products. When you receive loan offers from multiple lenders, focus intensely on the APR rather than just the advertised interest rate. A lender might entice you with a headline-grabbing low interest rate, only to load the loan with high origination fees or points, which would ultimately result in a higher APR. Always request a Loan Estimate from each lender, which is a standardized form that clearly outlines the interest rate, APR, and all associated costs. By comparing the APRs on these forms, you can objectively determine which loan is genuinely more affordable over its lifetime. Don’t hesitate to negotiate or question discrepancies; an informed borrower is a powerful borrower.

Understanding APR Limitations

While the APR is an invaluable tool, it’s important to recognize its limitations to avoid making decisions based on incomplete information.

- Assumptions on Loan Term: The APR calculation assumes you will hold the loan for its full term (e.g., 30 years). If you plan to refinance or sell your home much sooner (e.g., within 5-7 years), the impact of upfront fees on the APR might be overstated, as you wouldn’t be paying the lower interest rate for the full term that those fees “bought” you. In such cases, a loan with slightly higher interest but very low or no upfront fees might be more cost-effective.

- Exclusion of Third-Party Costs: As previously noted, the APR generally does not include all closing costs. Fees such as appraisal fees, title insurance, escrow fees, attorney fees, recording fees, and property taxes are typically paid by the borrower at closing but are not factored into the APR. These can add thousands of dollars to your upfront costs, so they must be considered alongside the APR. You’ll find these on your Loan Estimate under “Other Costs.”

- Adjustable-Rate Mortgage (ARM) APRs are Estimates: For ARMs, the APR is often an estimate based on the initial fixed rate and an assumption about how the rate might adjust in the future. Since future interest rates are unpredictable, the actual cost of an ARM over its life could be higher or lower than the initial APR suggests. For ARMs, it’s crucial to understand the cap structure (how much the rate can increase) and how often it adjusts.

The Importance of the Loan Estimate

The Loan Estimate (LE) is a critical document provided by lenders within three business days of applying for a mortgage. It clearly itemizes all the costs associated with your loan, including the interest rate, APR, closing costs, and projected monthly payments. This document is your best friend when comparing offers.

- Review Section A: Origination Charges: This section details the lender’s fees.

- Review Section B: Services You Cannot Shop For: Lists third-party services chosen by the lender.

- Review Section C: Services You Can Shop For: Lists services where you can choose your own provider (e.g., title insurance, pest inspection).

- Compare the “Total Loan Costs”: Located on the first page, this figure provides a quick snapshot.

- Crucially, compare the APR: Look for the “Comparisons” section on the second page of the LE. This section explicitly states the APR, allowing for direct comparison across different lenders.

By meticulously reviewing the Loan Estimate from several lenders and focusing on the APR, alongside other closing costs, you can make an informed decision that aligns with your financial goals and helps secure your dream home on the most advantageous terms.

In conclusion, while the nominal interest rate captures a significant piece of the mortgage puzzle, the Annual Percentage Rate (APR) provides the full picture, encompassing a broader range of fees and costs associated with borrowing. It is an indispensable tool mandated by law to protect consumers and foster transparency in the lending industry. By understanding its components, its distinctions from the interest rate, and the factors that influence it, borrowers can confidently navigate the complex mortgage landscape. Always prioritize comparing APRs across multiple lenders and thoroughly review your Loan Estimate to ensure you are selecting a mortgage that truly offers the best value for your long-term financial well-being. Don’t just look at the rate; look at the true cost.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.