In the landscape of American immigration, “AOS” or Adjustment of Status represents one of the most significant transitions an individual can undergo. While legal scholars view it as a procedural shift from a non-immigrant to an immigrant visa, for the savvy individual, it is fundamentally a high-stakes financial decision. AOS is the process used by eligible individuals already present in the United States to apply for lawful permanent resident status (a Green Card) without having to return to their home country for consular processing.

Navigating this path requires more than just legal compliance; it demands a robust financial strategy. From the initial capital outlay required for filing fees to the long-term wealth-building opportunities afforded by permanent residency, understanding AOS through the lens of personal finance is essential for any prospective applicant.

The Financial Landscape of Adjustment of Status (AOS)

The journey toward a Green Card through Adjustment of Status is paved with significant upfront costs. Unlike many other administrative processes, the U.S. Citizenship and Immigration Services (USCIS) operates largely on a fee-based model, meaning the applicant bears the weight of the agency’s operational expenses.

Understanding the Direct Costs: Filing Fees and Biometrics

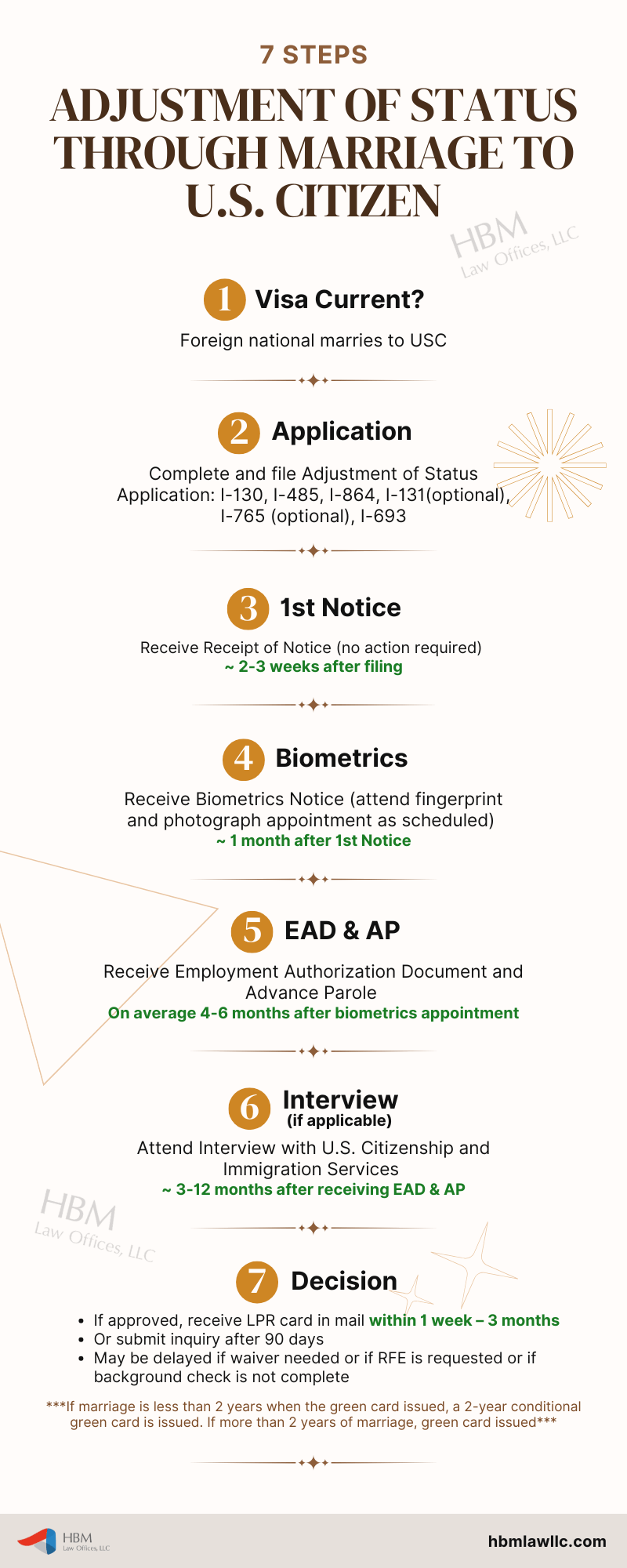

The most immediate hurdle in the AOS process is the Form I-485 filing fee. As of 2024, these fees have seen substantial adjustments. For most adult applicants, the cost of filing the I-485 is a four-figure investment. When you factor in the required biometrics fee—covering the cost of fingerprinting and background checks—the initial “entry price” can significantly impact a household’s liquid savings. It is vital to view these fees not just as a government tax, but as an investment in a “legal asset” that grants the right to live and work in the world’s largest economy.

Indirect Expenses: Medical Exams and Legal Counsel

Beyond the checks written to the Department of Homeland Security, the AOS process carries several “hidden” costs. Every applicant is required to undergo a medical examination by a civil surgeon designated by USCIS (Form I-693). These exams are not covered by standard health insurance and can range from $200 to $600 depending on the required vaccinations and the provider’s location.

Furthermore, while some choose the “DIY” route, many applicants hire immigration attorneys to ensure the precision of their filing. Legal fees can range from $2,500 to $7,500 or more. From a financial perspective, this is a risk-mitigation expense. A single error in an AOS application can lead to a Request for Evidence (RFE) or a denial, resulting in lost filing fees and potentially jeopardizing one’s ability to remain in the U.S. to earn an income.

Income Requirements and the Affidavit of Support

A central component of the AOS process—specifically for family-based applications—is the demonstration of financial self-sufficiency. The U.S. government seeks to ensure that new immigrants will not become a “public charge,” or a person who is primarily dependent on the government for subsistence.

Meeting the Federal Poverty Guidelines

To facilitate this, the petitioner (the person sponsoring the immigrant) must file Form I-864, the Affidavit of Support. This document is a legally binding contract with the U.S. government. The sponsor must demonstrate an annual income that is at least 125% of the Federal Poverty Guidelines for their household size. For a household of two, this typically requires an income in the mid-$20,000s, though this figure increases significantly with more dependents. This requirement ensures that the immigrant has a financial safety net, reducing the “financial liability” they might otherwise pose to the state.

The Role of Joint Sponsors in Financial Eligibility

In cases where the primary petitioner does not meet the income threshold, the AOS process allows for the inclusion of a joint sponsor. This individual must also meet the 125% income requirement and agrees to share the financial responsibility for the applicant. From a personal finance standpoint, being a joint sponsor is a serious commitment; it is a liability that remains in effect until the immigrant becomes a U.S. citizen or has worked 40 qualifying quarters (usually 10 years). Prospective applicants must manage these interpersonal financial relationships with transparency and care.

The Opportunity Cost of the AOS Timeline

One of the most overlooked aspects of AOS immigration is the “opportunity cost” associated with the processing timeline. Between the moment an application is filed and the moment it is approved, an applicant enters a state of “authorized stay,” but their ability to generate income may be temporarily restricted.

Employment Authorization and Income Potential

Typically, an AOS applicant also files for an Employment Authorization Document (EAD) via Form I-765. In the past, the “gap” between filing for AOS and receiving a work permit could last six months to a year. During this window, if the applicant does not have a prior valid work visa (like an H-1B or L-1), they are legally barred from working. This represents a significant loss of potential earnings. Financial planning for AOS must include an “emergency fund” or a “bridge fund” to cover living expenses during this period of forced unemployment.

Managing Cash Flow During the “Gap” Period

Because the timeline for AOS can be unpredictable—varying from 8 months to over 2 years depending on the service center—liquidity management is crucial. Applicants should avoid locking their capital into illiquid assets (like long-term CDs or real estate) just before filing. Having a high-yield savings account or a liquid brokerage account allows the applicant to weather the “waiting period” without accruing high-interest consumer debt.

Long-term ROI: The Wealth-Building Potential of Permanent Residency

While the costs of AOS are high, the Return on Investment (ROI) is unparalleled. Transitioning to a Green Card holder fundamentally changes an individual’s financial profile and opens doors to wealth-building tools that are often restricted for non-immigrants.

Access to Credit, Mortgages, and Low-Interest Loans

Many lenders are hesitant to provide long-term financing to individuals on temporary visas due to the risk of the borrower having to leave the country. Once an individual achieves AOS and receives their Green Card, their “creditworthiness” in the eyes of institutional lenders increases. Permanent residents have easier access to FHA loans, competitive mortgage rates, and business lines of credit. This shift allows for the transition from being a “renter” in the economy to being an “owner,” facilitating the accumulation of home equity and business assets.

Career Mobility and Salary Negotiation Power

Perhaps the greatest financial benefit of AOS is the “uncoupling” of one’s legal status from a specific employer. Many high-skilled workers on H-1B visas are functionally “locked” into their roles; changing jobs requires expensive and uncertain visa transfers. This lack of mobility often leads to “wage stagnation,” where the employee is paid less than the market rate.

With a Green Card in hand, the immigrant gains total career mobility. They can pivot to higher-paying roles, negotiate for better compensation packages, or launch their own startups. The ability to participate in the “free market” for labor often results in a 20% to 50% increase in lifetime earnings potential, far outweighing the initial $10,000 to $15,000 spent on the AOS process.

Tax Implications and Financial Planning for New Green Card Holders

Finally, achieving AOS marks a transition in how the individual is treated by the Internal Revenue Service (IRS). Permanent residents are considered “resident aliens” for tax purposes from the moment they are granted status, regardless of how many days they spend in the U.S.

Global Income Reporting and Compliance

The most significant change is that Green Card holders are taxed on their worldwide income. This means that any rental income, dividends, or business profits generated in the applicant’s home country must be reported to the IRS. Additionally, new permanent residents must comply with FBAR (Foreign Bank and Financial Accounts Reporting) requirements if the aggregate value of their foreign accounts exceeds $10,000 at any time during the year.

Strategic Financial Onboarding

New Green Card holders should engage in “financial onboarding” shortly after their AOS is approved. This includes updating their W-4 with their employer, reviewing their retirement contributions (401k/IRA), and perhaps most importantly, consulting with a tax professional who understands international treaties. Proper tax planning ensures that the immigrant does not fall victim to double taxation and can maximize the tax-advantaged growth of their U.S.-based investments.

In conclusion, “What is AOS Immigration?” is a question that yields two answers. Legally, it is a change of status. Financially, it is a complex, multi-year investment project. By understanding the direct costs, meeting the income benchmarks, managing the opportunity costs of the waiting period, and leveraging the long-term wealth-building benefits of residency, applicants can ensure that their transition to the United States is not just a legal success, but a cornerstone of their future financial prosperity.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.