In the complex landscape of personal and business finance, few phrases carry as much weight and potential for disruption as “outstanding judgment.” Far from a mere legal formality, an outstanding judgment represents a court’s official decree that one party (the debtor) owes a specific sum of money to another party (the creditor), and that this obligation remains unsettled. It signifies a transition from a simple debt or dispute into a legally enforced obligation, carrying with it a host of severe consequences for the debtor’s financial health, creditworthiness, and future opportunities. Understanding what an outstanding judgment is, how it arises, and its profound implications is crucial for anyone navigating the financial world, whether as a consumer, a business owner, or a diligent steward of their credit.

This article delves into the core definition of an outstanding judgment, dissecting its legal origins and the mechanisms through which it comes into being. We will explore the various reasons why a judgment might be issued and, critically, why it might remain “outstanding.” Beyond the legalities, we will scrutinize the far-reaching effects on credit scores, financial stability, and the aggressive collection tactics that often follow. Finally, we will provide actionable insights into how individuals and businesses can navigate, resolve, and most importantly, prevent the burden of an outstanding judgment.

The Anatomy of a Court Judgment

To comprehend what makes a judgment “outstanding,” we must first understand what a judgment itself entails. It’s not merely a bill or an overdue payment; it’s a formal declaration by a court of law.

What Constitutes a Judgment?

A judgment, in the financial and legal context, is a final order or decision by a court in a lawsuit, typically requiring one party to pay a monetary amount to another. It’s the culmination of a legal dispute where the court has determined liability and the extent of damages. For example, if a credit card company sues an individual for unpaid debt and wins, the court will issue a judgment stating the individual owes the company a specific sum, including the original debt, interest, and often court costs and attorney fees. This document legally establishes the debt and the creditor’s right to collect it.

The Path to Judgment: From Claim to Verdict

The journey to an outstanding judgment typically begins when a creditor, unable to collect a debt through conventional means, decides to sue the debtor. This involves filing a complaint or summons with the court, officially initiating a lawsuit. The debtor is then served with legal papers, informing them of the suit and requiring a response.

If the debtor fails to respond within the stipulated time frame, the court may issue a default judgment in favor of the creditor. This is a common scenario for many outstanding judgments, as debtors might be unaware of the lawsuit, fail to understand its gravity, or simply be unable to mount a defense. If the debtor does respond, the case proceeds through the legal system, potentially involving discovery, motions, and eventually a trial. If the court rules in favor of the creditor after a trial, a judgment is issued. Regardless of how it’s obtained, once issued, the judgment becomes a legally binding directive.

Distinguishing Judgment from Debt

It’s crucial to differentiate a judgment from a mere debt. Before a judgment, an overdue bill or loan is a contractual obligation. After a judgment, it transforms into a legal obligation with the full backing and enforcement power of the state. A judgment often comes with a longer statute of limitations for collection, accrues post-judgment interest (which can be significant), and grants the creditor access to powerful collection tools not available for ordinary debts. Essentially, a judgment elevates the debt from a private matter between parties to a public, court-sanctioned obligation that the debtor is legally compelled to satisfy.

Why a Judgment Becomes “Outstanding”

A judgment becomes “outstanding” when it has been issued by a court but has not yet been fully satisfied or paid by the debtor. This status is critical because it empowers the judgment creditor to pursue various legal avenues to collect the debt.

Unpaid Debts and Legal Enforcement

The primary reason a judgment remains outstanding is simply that the debtor has not paid the amount owed. This could be due to several factors:

- Financial Inability: The debtor may genuinely lack the funds or assets to pay the judgment.

- Dispute or Refusal: The debtor might still dispute the validity of the debt or judgment, even after a court ruling, and refuses to pay.

- Ignorance: In cases of default judgments, the debtor might not have been fully aware of the judgment or its implications, leading to inaction.

- Strategic Delay: Some debtors might attempt to delay payment, hoping the creditor will give up or that the statute of limitations will expire (though judgments typically have very long statutes of limitations, often renewable).

When a judgment is outstanding, the creditor gains the right to employ post-judgment collection actions. These actions are legally sanctioned methods to force payment and are far more aggressive than typical debt collection calls.

The Role of the Creditor and Debtor

The creditor, now a “judgment creditor,” holds a powerful legal instrument. Their role shifts from trying to persuade payment to legally enforcing it. They will actively seek information about the debtor’s assets, income, and property to identify targets for collection.

The debtor, now a “judgment debtor,” is legally obligated to satisfy the judgment. Their options are often limited to paying, negotiating a settlement, or, in some extreme cases, filing for bankruptcy. Ignoring an outstanding judgment is not a viable long-term strategy, as the judgment creditor typically has years, if not decades, to pursue collection.

Types of Debts Leading to Judgments

Almost any type of financial obligation can lead to a judgment if left unpaid and pursued legally. Common examples include:

- Credit Card Debt: One of the most frequent causes, as credit card companies are quick to sue for large outstanding balances.

- Personal Loans: Unsecured loans from banks or private lenders.

- Medical Bills: Large, unpaid medical expenses can lead healthcare providers or collection agencies to seek judgments.

- Business Debts: Unpaid invoices, breach of contract in business dealings, or defaulted business loans.

- Auto Loan Deficiencies: If a car is repossessed and sold, the difference between the sale price and the remaining loan balance can result in a deficiency judgment.

- Landlord-Tenant Disputes: Unpaid rent or damages to property can result in a judgment against a tenant.

In essence, any significant financial obligation that becomes delinquent and is pursued through the courts can culminate in an outstanding judgment, impacting both individuals and businesses.

The Far-Reaching Impact of an Outstanding Judgment

The consequences of an outstanding judgment extend far beyond the immediate obligation to pay. They cast a long shadow over one’s financial life, affecting credit, future opportunities, and peace of mind.

Credit Score Devastation

An outstanding judgment is one of the most damaging entries that can appear on a credit report. Once a judgment is filed, it becomes public record and is picked up by credit reporting agencies.

- Severe Drop in Score: Credit scores (like FICO and VantageScore) can plummet significantly, often by hundreds of points.

- Duration: Judgments typically remain on credit reports for seven years from the filing date, even if paid sooner in many states (though some states remove them sooner if paid). The impact, however, lessens over time if it’s the only negative mark.

- Lender Perception: Lenders view outstanding judgments as a major red flag, indicating high risk and a history of failing to meet financial obligations. This makes obtaining new credit extremely difficult.

Hindrances to Future Financial Endeavors

The negative impact on credit translates directly into significant obstacles for various financial activities:

- Loan and Mortgage Applications: Securing a mortgage, auto loan, or personal loan becomes nearly impossible or prohibitively expensive due to high-interest rates and strict terms.

- Renting Apartments: Landlords frequently check credit reports, and an outstanding judgment can lead to rejection or demands for larger security deposits.

- Employment Opportunities: For certain positions, especially those involving financial responsibilities or security clearances, employers may conduct credit checks. An outstanding judgment could be a barrier to employment.

- Business Operations: For entrepreneurs, an outstanding judgment against their business or even personally can hinder access to business loans, lines of credit, and even supplier relationships.

Aggressive Collection Tactics

A judgment creditor is not merely waiting for payment; they are legally empowered to enforce collection. This can involve intrusive and impactful measures:

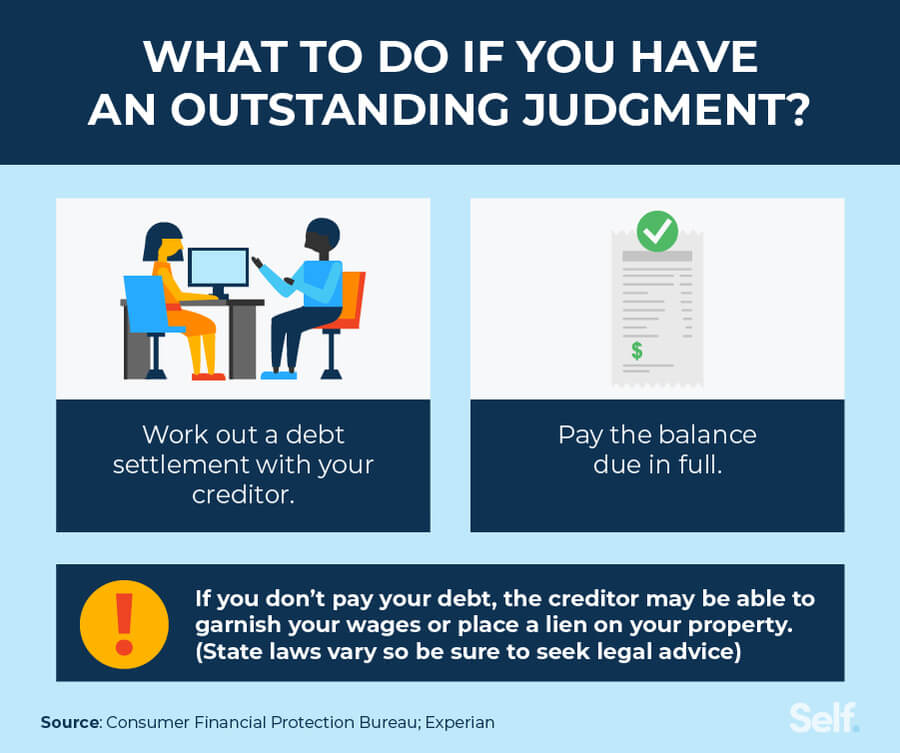

- Wage Garnishment: A court order directing an employer to withhold a portion of the debtor’s earnings and pay it directly to the creditor. State and federal laws limit the percentage that can be garnished, but it can still be a substantial deduction from a paycheck.

- Bank Levies (Account Garnishment): A court order allowing the creditor to seize funds directly from the debtor’s bank accounts. This can empty an account and disrupt essential bill payments.

- Property Liens: A legal claim against the debtor’s real estate (like a home or land). If the property is sold, the lien must typically be paid off from the proceeds before the debtor receives any funds. In some cases, creditors can force the sale of non-exempt property.

- Asset Seizure: Depending on state laws, certain non-exempt personal property (vehicles, valuable possessions) could be seized and sold to satisfy the debt.

Legal Ramifications and Public Record

Judgments are matters of public record. This means anyone can look up judgments filed against an individual or business. This lack of privacy can be embarrassing and can also be used by other potential creditors or even scam artists. Furthermore, failing to address a judgment can lead to further legal actions, such as motions to compel information about assets, contempt of court charges if court orders are ignored, or even further judgments for non-compliance.

Navigating and Resolving an Outstanding Judgment

While an outstanding judgment is a serious matter, it is not insurmountable. There are concrete steps debtors can take to address, negotiate, and ultimately resolve the situation.

Understanding Your Rights and Options

The first and most critical step is to seek legal counsel from an attorney specializing in debt collection defense or consumer law. An attorney can:

- Verify the Judgment’s Validity: Ensure the judgment was properly obtained and that the statute of limitations for collection has not expired.

- Understand State Laws: Laws regarding judgments, garnishment exemptions, and collection practices vary significantly by state.

- Identify Exempt Assets: Determine which of your assets (e.g., a portion of your wages, certain retirement accounts, homestead exemptions) are protected from collection under state and federal law.

- Review for Errors: Check for any errors in the judgment amount or legal process.

Strategies for Settlement

Often, creditors are open to negotiation, especially if it means recovering at least a portion of the debt without further legal hassle.

- Lump-Sum Payment: If possible, offering a lump-sum payment that is less than the full judgment amount (a “pay-for-delete” or “settlement in full”) can be an effective strategy. Creditors may accept 50-80% of the judgment amount to avoid continued collection efforts. Always get the agreement in writing before paying.

- Payment Plans: If a lump sum isn’t feasible, negotiate a structured payment plan with terms you can realistically meet. Again, ensure all terms are documented in writing.

- Consent Judgment: Sometimes, if a lawsuit is still pending, you might be able to negotiate a consent judgment where you agree to a judgment in exchange for a more manageable payment plan or a reduced amount.

Challenging the Judgment (If Applicable)

In specific circumstances, it may be possible to challenge or “vacate” a judgment:

- Default Judgment: If a default judgment was entered because you were never properly served with the lawsuit or had a legitimate reason for not responding (e.g., illness, fraud, mistaken identity), you might be able to file a motion to vacate the judgment. This reopens the case, allowing you to present a defense.

- Proving Payment: If you believe the judgment has already been paid or was based on a debt you don’t owe, you’ll need to provide clear documentation.

- Identity Theft: If the judgment is the result of identity theft, you must report it to the authorities and work to have it removed from your record.

The Process of Satisfaction and Release

Once a judgment is paid in full or settled, it’s crucial to ensure it is formally “satisfied” in the court records.

- Satisfaction of Judgment: The creditor is legally required to file a “Satisfaction of Judgment” (or similar document) with the court, which officially acknowledges that the debt has been paid.

- Obtain Documentation: Get a copy of this document for your records.

- Credit Reporting Agencies: Monitor your credit report to ensure the judgment is correctly reported as “satisfied” (or ideally, removed if part of a pay-for-delete agreement). This may not immediately remove it, but it shows it’s no longer outstanding.

Prevention: Avoiding Outstanding Judgments

The best strategy, of course, is to avoid a judgment altogether. Proactive financial management and timely action can significantly reduce this risk.

Proactive Debt Management

- Budgeting and Financial Planning: Maintain a clear budget to understand your income and expenses, ensuring you can meet your obligations.

- Emergency Fund: Build an emergency savings fund to cover unexpected expenses, reducing the likelihood of falling behind on payments.

- Debt Consolidation: If you have multiple high-interest debts, explore options like debt consolidation loans or balance transfers to simplify payments and potentially lower interest rates.

- Credit Counseling: If you’re struggling with debt, non-profit credit counseling agencies can help you develop a debt management plan.

Addressing Financial Disputes Promptly

- Communication with Creditors: If you anticipate difficulty making payments, contact your creditors immediately. Many are willing to work with you on payment arrangements before resorting to legal action.

- Mediation or Arbitration: For disputes, consider alternative dispute resolution methods like mediation or arbitration, which can resolve issues outside of court, saving time, money, and stress.

- Respond to Lawsuits: Never ignore a summons or legal complaint. Seek legal advice immediately and file a response to avoid a default judgment.

Legal Due Diligence in Contracts

- Read Before You Sign: Fully understand the terms and conditions of any loan, credit agreement, or contract before signing it.

- Seek Legal Advice for Complex Contracts: For significant financial agreements, consider having an attorney review the contract to ensure you understand your obligations and potential liabilities.

Conclusion

An outstanding judgment is a serious financial and legal hurdle, marking a significant escalation of debt into a legally enforceable obligation. Its presence on credit reports can devastate credit scores, hinder access to future financing, and trigger aggressive collection actions like wage garnishments and bank levies. Understanding the origins, impact, and pathways to resolution is not just theoretical knowledge; it’s essential for maintaining financial solvency and protecting one’s future.

While the consequences are severe, an outstanding judgment is not a permanent financial death sentence. Through informed legal counsel, diligent negotiation, and, when appropriate, challenging the judgment, individuals and businesses can navigate these turbulent waters. Ultimately, the most effective approach remains prevention: robust financial planning, proactive communication with creditors, and a diligent response to any legal proceedings can safeguard against the profound and lasting impact of an outstanding judgment, preserving both financial stability and peace of mind.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.