An ATV accident, in its most basic definition, is an unintended and often sudden collision, rollover, or operational mishap involving an All-Terrain Vehicle (ATV) that results in property damage, injury, or even fatality. While the immediate focus might be on the physical trauma or the mangled machinery, the true scope of an ATV accident extends far beyond the observable. From a financial perspective, an ATV accident is not merely an unfortunate incident; it is a complex web of direct and indirect costs, liabilities, and long-term financial repercussions that can significantly impact an individual’s or family’s economic well-being. Understanding “what” an ATV accident entails from a monetary standpoint is crucial for anyone engaging with these powerful recreational or utility vehicles. It necessitates a deep dive into the costs of medical care, property repair, legal battles, insurance implications, and the broader economic ripple effects that can follow such an event. This article will dissect the multifaceted financial landscape of an ATV accident, providing insights for enthusiasts, property owners, and anyone concerned with personal financial resilience.

The Hidden Costs of an ATV Accident: Beyond Immediate Damage

The initial shock of an ATV accident often blinds individuals to the extensive financial burden that is about to unfold. While visible damage to the ATV or apparent physical injuries are immediate concerns, a myriad of less obvious, yet equally substantial, costs can quickly accumulate, transforming a momentary lapse into a prolonged financial drain. These hidden costs often catch individuals unprepared, underscoring the importance of comprehensive financial planning and risk assessment.

Medical Expenses and Long-Term Care

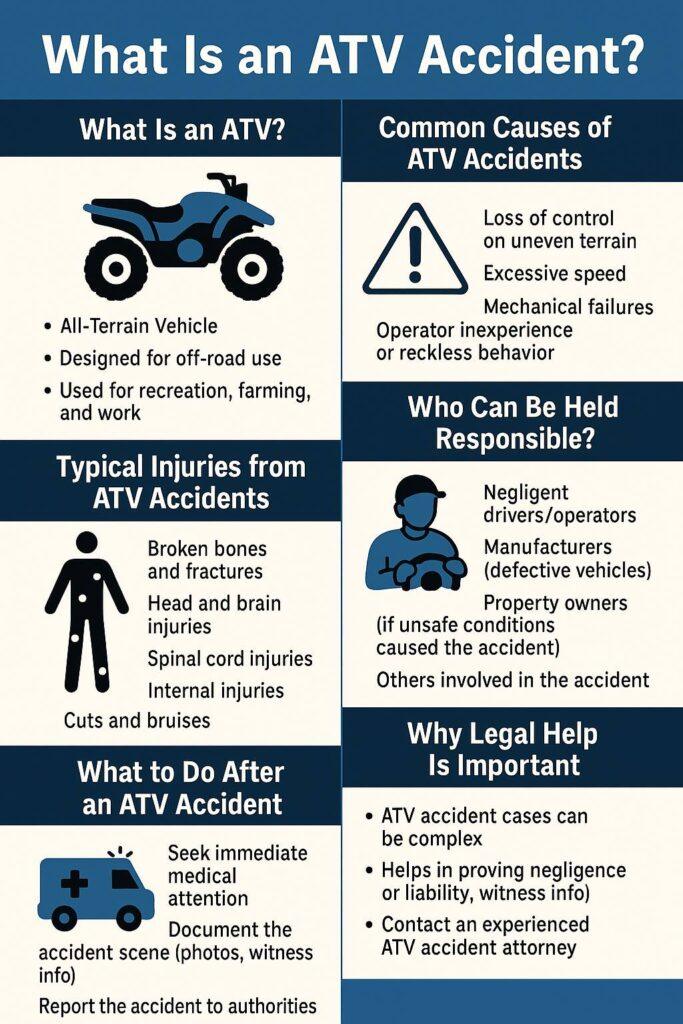

Perhaps the most significant financial hit stemming from an ATV accident involves medical expenses. Injuries sustained from ATV mishaps can range from minor scrapes and bruises to severe fractures, head trauma, spinal cord injuries, and internal organ damage. Each level of injury carries its own escalating price tag. Emergency room visits, ambulance services, diagnostic imaging (X-rays, MRIs), and surgical procedures represent just the tip of the iceberg. Post-operative care, hospital stays, and prescription medications can quickly deplete savings and challenge even robust health insurance plans.

Beyond immediate treatment, many ATV accident victims face the daunting prospect of long-term care. Rehabilitation services, including physical therapy, occupational therapy, and speech therapy, can extend for months or even years. For severe, life-altering injuries such as paralysis or traumatic brain injury, the need for ongoing specialized care, home modifications, assistive devices, and personal attendants can translate into costs running into hundreds of thousands or even millions of dollars over a lifetime. Furthermore, a severe injury can lead to a significant loss of income, either temporarily or permanently, impacting an individual’s ability to work and earn a living. This loss of earning capacity can profoundly affect household finances, retirement savings, and future financial stability, representing a colossal hidden cost that far outstrips initial medical bills.

Property Damage and Replacement Costs

The ATV itself is often a casualty of an accident, and the financial implications of its damage can be substantial. Depending on the severity of the incident, an ATV might require extensive repairs, parts replacement, or could be deemed a total loss. Repair costs can vary widely based on the make and model of the ATV, the availability of parts, and the labor rates of mechanics. Specialized components, particularly for newer or high-performance models, can be expensive and difficult to source. If the ATV is totaled, the owner faces the cost of replacement, which can be thousands of dollars for a new or even a used vehicle.

However, property damage is not always limited to the ATV. An accident can involve collisions with other vehicles, fences, utility poles, trees, or structures. Repairing or replacing these damaged assets can add significant financial burden. If the accident occurs on someone else’s property, the operator could be held liable for damages, including landscaping, outbuildings, or even environmental remediation if fuel or oil spills occur. Furthermore, the cost of towing and storage for a damaged ATV, especially from remote locations, can quickly add up, contributing to the often-overlooked expenses that accumulate in the aftermath of an accident.

Legal and Administrative Fees

In cases where liability is disputed, injuries are severe, or significant property damage occurs, an ATV accident can quickly escalate into a legal quagmire. Engaging legal counsel to navigate personal injury claims, property damage disputes, or wrongful death lawsuits incurs substantial costs. Attorney fees, which often involve retainers or contingency fees (a percentage of the settlement), can be significant. Beyond legal representation, there are court filing fees, expert witness fees (e.g., medical professionals, accident reconstructionists), deposition costs, and investigative expenses.

Even for less severe accidents, administrative fees can arise. These might include costs associated with police reports, medical records requests, insurance claim processing fees, and time spent away from work to handle these matters. The psychological toll and time investment required to deal with these administrative and legal complexities, while not directly monetary, indirectly contribute to financial strain by diverting focus and energy from productive activities. Navigating these complexities without proper legal and financial guidance can lead to unfavorable outcomes, further exacerbating the financial fallout.

The Role of Insurance in Mitigating Financial Risk

Given the extensive and often unforeseen costs associated with an ATV accident, insurance emerges as a critical financial tool for risk mitigation. Adequate insurance coverage can act as a buffer, protecting individuals from catastrophic financial losses. However, understanding the nuances of various policy types and the claims process is paramount to effectively leverage this financial safeguard.

Types of ATV Insurance Coverage

Just like auto insurance, ATV insurance offers several types of coverage, each designed to address specific financial risks.

- Liability Coverage: This is often the most fundamental type, protecting the insured if they are at fault for an accident that causes bodily injury or property damage to another party. It covers medical expenses for the injured party, lost wages, and repair or replacement costs for damaged property. Without sufficient liability coverage, a responsible party’s personal assets could be at risk.

- Collision Coverage: This pays for damages to the insured’s ATV resulting from a collision with another vehicle or object, regardless of who is at fault. This is crucial for protecting the investment in the ATV itself.

- Comprehensive Coverage: This protects against non-collision incidents such as theft, vandalism, fire, natural disasters (e.g., floods, hail), or hitting an animal. It provides a broad safety net for unforeseen circumstances.

- Uninsured/Underinsured Motorist Coverage: While less common for ATVs that are not road-legal, some policies offer this to protect the insured if they are involved in an accident with someone who has insufficient or no insurance. This can be particularly relevant in areas where ATVs are used on shared trails or private property with multiple users.

- Medical Payments Coverage: This covers medical expenses for the insured and any passengers, regardless of who is at fault. It can help bridge the gap before health insurance kicks in or cover deductibles and co-pays.

- Accessory Coverage: Given that many ATV owners invest in specialized gear, winches, plows, or other add-ons, this optional coverage protects these additional investments.

Selecting the right combination and level of coverage is a vital financial decision that should align with the value of the ATV, personal risk tolerance, and individual asset protection needs.

Navigating the Claims Process

Once an accident occurs, effectively navigating the insurance claims process is crucial for financial recovery. The first step involves thoroughly documenting the accident scene, including photographs of injuries, property damage, and the surrounding environment. Collecting contact information from witnesses and other involved parties is also critical. Promptly notifying the insurance company is essential, as delays can sometimes complicate the claim.

When filing a claim, honesty and accuracy are paramount. Policyholders must understand their policy limits, deductibles, and any exclusions that might apply. A deductible is the amount the insured must pay out-of-pocket before the insurance coverage kicks in. Higher deductibles typically result in lower premiums but mean a larger immediate financial outlay in case of an accident. The claims adjuster will investigate the incident, assess damages, and determine payouts based on policy terms. Having all relevant documentation, including medical bills, repair estimates, and police reports, readily available can expedite the process and ensure a fair settlement.

Impact on Premiums and Future Insurability

Filing an insurance claim, particularly for an at-fault accident, can have long-term financial implications in the form of increased insurance premiums. Insurers use a risk assessment model, and an accident history, especially one involving significant payouts, signals a higher risk profile for the policyholder. This can lead to higher annual premiums for several years, effectively increasing the ongoing cost of ATV ownership.

In some extreme cases, or with a history of multiple claims, an individual might find it challenging to obtain insurance coverage, or specific types of coverage, from certain providers. This phenomenon, known as affecting future insurability, can force individuals into higher-cost specialty insurance markets. Understanding this potential financial consequence can influence decisions regarding when to file a claim versus absorbing minor costs out-of-pocket, weighing the immediate financial relief against long-term premium increases.

Proactive Financial Strategies for ATV Enthusiasts

For ATV enthusiasts, enjoying the thrill of the ride responsibly extends beyond merely following safety guidelines; it encompasses adopting proactive financial strategies to safeguard against the inevitable risks. By integrating financial planning into their passion, individuals can protect their assets, maintain their financial stability, and ensure their enjoyment of ATVs doesn’t come at an unforeseen and unbearable cost.

Budgeting for Risk: Insurance and Emergency Funds

A cornerstone of responsible ATV ownership is budgeting not just for the purchase and maintenance of the vehicle, but specifically for the financial risks it presents. This means allocating sufficient funds for comprehensive insurance coverage. It’s often tempting to opt for the cheapest, bare-minimum policy, but understanding the potential financial liabilities outlined earlier reveals the fallacy of such an approach. Investing in robust liability limits, collision, comprehensive, and potentially medical payments coverage should be viewed as a necessary expenditure, not an optional luxury.

Beyond insurance, establishing a dedicated emergency fund specifically for unexpected ATV-related expenses is a prudent financial move. This fund can cover deductibles, minor repairs not covered by insurance, medical co-pays, or even temporary income loss. This financial safety net acts as a first line of defense, preventing reliance on credit cards or drawing from long-term savings in the immediate aftermath of an accident, thus preserving overall financial health.

Understanding Liability and Asset Protection

Every ATV operator faces the risk of personal liability in an accident, especially if they are deemed at fault for injuries to others or damage to property. Understanding this exposure is critical for asset protection. If insurance coverage is insufficient to cover a large settlement or judgment, personal assets such as savings accounts, investments, and even future earnings could be at risk.

Strategies for asset protection include not only maximizing insurance coverage but also considering an umbrella insurance policy. An umbrella policy provides additional liability coverage above and beyond the limits of primary policies like ATV or homeowner’s insurance, offering an extra layer of protection against significant claims. Consulting with a financial advisor or an attorney specializing in asset protection can help individuals structure their finances and estate in a way that minimizes vulnerability to large legal judgments arising from an accident.

Safety Investments as Financial Safeguards

While often perceived as an operational cost, investments in safety gear and training are, in essence, financial safeguards. High-quality helmets, protective eyewear, sturdy boots, gloves, and appropriate riding apparel significantly reduce the severity of injuries in the event of an accident. Reducing injury severity directly translates to lower medical bills, shorter recovery times, and less potential for lost income—all substantial financial benefits.

Similarly, enrolling in ATV safety courses and ongoing training programs, while an upfront expense, equips riders with crucial skills and knowledge to prevent accidents. Proper riding techniques, hazard recognition, and emergency maneuvers can significantly reduce the likelihood of an incident occurring. Viewing these expenditures as preventative financial investments, rather than mere expenses, highlights their long-term economic value in minimizing the costly aftermath of an ATV accident.

The Economic Ripple Effect: Broader Financial Consequences

The financial impact of an ATV accident extends beyond immediate costs and insurance claims; it can trigger a wider economic ripple effect that destabilizes an individual’s or family’s financial standing for years to come. These broader consequences highlight the profound interconnectedness of personal finance and the unexpected disruptions an accident can cause.

Impact on Personal Credit and Financial Standing

Large, uninsured, or underinsured costs resulting from an ATV accident can severely damage an individual’s personal credit and overall financial standing. If medical bills, legal fees, or property damage costs are not fully covered by insurance or an emergency fund, individuals may be forced to take on significant debt. This could involve high-interest personal loans, drawing from retirement accounts, or relying on credit cards. Accruing substantial debt, especially if payments are missed, will negatively impact credit scores, making it harder to secure loans for future endeavors like buying a home or a car, or even affecting interest rates on existing credit.

Furthermore, potential lawsuits and judgments can lead to wage garnishments or liens on property, further eroding financial stability. A severe accident can fundamentally alter an individual’s financial trajectory, shifting focus from wealth building to debt management and recovery, underscoring the long-term economic vulnerability.

Opportunity Costs and Long-Term Financial Goals

An ATV accident carries significant opportunity costs—the benefits an individual misses out on by choosing one alternative over another. Funds diverted to accident-related expenses, whether for medical treatment, repairs, or legal fees, are funds that can no longer be invested in education, retirement savings, real estate, or other wealth-generating opportunities. This diversion can delay or derail long-term financial goals, such as saving for a child’s college education, accumulating a down payment for a house, or achieving financial independence for retirement.

Moreover, if an injury leads to a prolonged inability to work, the loss of income is not just an immediate financial hit but also represents lost earning potential over many years. This could mean fewer contributions to 401(k)s, missed career advancement opportunities, and a reduced overall lifetime wealth accumulation. The long-term impact on financial independence and security can be profound, making an accident a setback that may take decades to recover from financially.

Estate Planning Considerations

While a grim consideration, severe ATV accidents can, unfortunately, result in fatality or severe incapacitation. In such devastating circumstances, proper estate planning becomes critically important to manage the financial aftermath. Without a clear will, trusts, or designated beneficiaries, the financial assets of the deceased or incapacitated individual could be subject to lengthy and costly probate processes, potentially leaving family members in a precarious financial situation.

Estate planning includes ensuring adequate life insurance coverage to provide for dependents, establishing powers of attorney for financial and medical decisions, and creating trusts to manage assets and distribute them according to one’s wishes. While not directly preventing an accident, robust estate planning mitigates the financial chaos and hardship that can befall surviving family members, serving as a vital financial safeguard for the future.

In conclusion, understanding “what is an ATV accident” from a purely financial lens reveals a landscape fraught with potential perils far beyond mere scrapes and dents. It is a potent reminder that responsible ATV engagement demands not just physical caution, but also meticulous financial foresight. From immediate medical bills and property damage to complex legal battles, insurance premium hikes, and long-term disruptions to personal credit and financial goals, the economic footprint of an ATV accident can be devastating. By prioritizing comprehensive insurance, establishing emergency funds, investing in safety, and engaging in proactive financial and estate planning, ATV enthusiasts can better safeguard their financial future, ensuring their passion remains a source of enjoyment rather than financial distress.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.