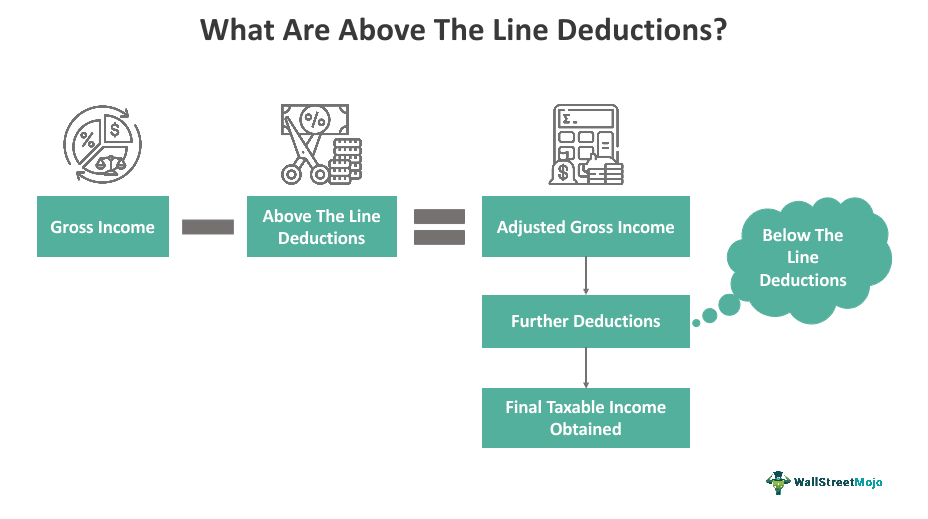

Understanding the nuances of tax deductions is crucial for maximizing your financial well-being. Among the various types of deductions available, “above-the-line” deductions hold a particular significance. These deductions, often referred to as “adjustments to income,” are valuable because they reduce your Adjusted Gross Income (AGI) directly. This reduction in AGI can have a ripple effect, potentially lowering your tax liability, qualifying you for other tax credits and deductions that are AGI-dependent, and even impacting your state tax obligations.

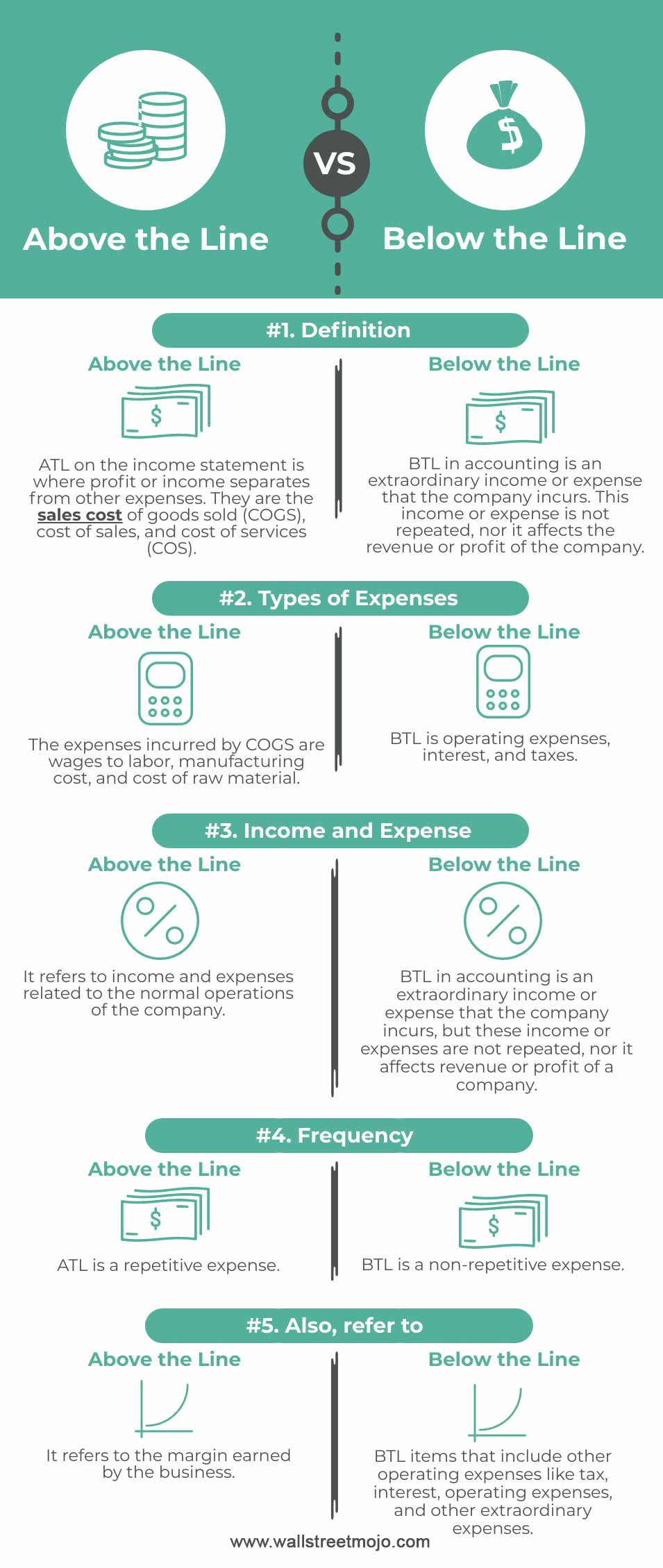

The term “above-the-line” originates from the structure of IRS Form 1040 (or its predecessor, Schedule 1). On this form, above-the-line deductions are listed before the calculation of AGI. In contrast, “below-the-line” deductions, also known as itemized deductions, are subtracted from AGI to arrive at taxable income. The implications of this distinction are profound, offering a more direct and often more beneficial route to tax savings for many individuals and businesses. This article will delve into the definition, characteristics, and common examples of above-the-line deductions, empowering you to leverage them effectively in your financial planning.

The Mechanics of Above-the-Line Deductions

At their core, above-the-line deductions represent specific expenses or contributions that the tax code allows you to subtract from your gross income. Unlike below-the-line deductions, which require you to choose between taking the standard deduction or itemizing your expenses, above-the-line deductions can generally be claimed in addition to either the standard deduction or itemized deductions. This flexibility makes them particularly attractive for taxpayers.

The Importance of Adjusted Gross Income (AGI)

The primary benefit of an above-the-line deduction lies in its direct impact on your Adjusted Gross Income (AGI). AGI is a critical figure on your tax return, serving as a stepping stone to calculating your final taxable income. A lower AGI can unlock a cascade of financial advantages.

- Reduced Tax Liability: The most immediate benefit is a lower overall tax bill. Since taxable income is derived from AGI after further deductions and exemptions, a reduced AGI directly translates to less income being subject to taxation.

- Eligibility for Tax Credits and Deductions: Many tax credits and deductions have income limitations. By lowering your AGI, above-the-line deductions can help you qualify for these beneficial provisions that you might otherwise be excluded from. For instance, certain education credits or deductions for retirement savings might become accessible with a lower AGI.

- Alternative Minimum Tax (AMT) Considerations: While less common for the average taxpayer, a reduced AGI can also influence your potential liability under the Alternative Minimum Tax (AMT).

- State Tax Implications: Many states use federal AGI as a starting point for calculating state income tax. Therefore, reducing your federal AGI can also lead to savings on your state tax returns.

Standard Deduction vs. Itemized Deductions: The Above-the-Line Advantage

The distinction between above-the-line and below-the-line deductions becomes clearer when contrasted with the two primary methods of reducing taxable income: the standard deduction and itemized deductions.

- Standard Deduction: This is a fixed dollar amount that reduces your taxable income. The amount varies based on your filing status (single, married filing jointly, etc.) and age. Most taxpayers opt for the standard deduction because it’s simpler and often more beneficial than itemizing.

- Itemized Deductions: If your eligible deductible expenses exceed the standard deduction amount, you can choose to itemize. Common itemized deductions include state and local taxes (SALT), mortgage interest, charitable contributions, and medical expenses (above a certain percentage of AGI).

The key differentiator is that above-the-line deductions are subtracted from gross income before AGI is calculated, regardless of whether you take the standard deduction or itemize. Below-the-line deductions, on the other hand, are subtracted from AGI to arrive at taxable income. This means above-the-line deductions are generally more universally beneficial, as they don’t force a choice between two other deduction strategies.

Common Above-the-Line Deductions for Individuals

The IRS recognizes several types of expenses that qualify as above-the-line deductions for individuals. Understanding these can help you identify opportunities to reduce your tax burden.

Retirement Savings Contributions

One of the most significant and widely used above-the-line deductions relates to contributions made to certain retirement savings accounts.

- Traditional IRA Contributions: Contributions you make to a Traditional Individual Retirement Arrangement (IRA) are often deductible. The deductibility may be limited if you are covered by a retirement plan at work and your income exceeds certain thresholds. However, for many individuals, these contributions provide immediate tax savings.

- SEP IRAs and SIMPLE IRAs: If you are self-employed or own a small business, you can establish and contribute to Simplified Employee Pension (SEP) IRAs or Savings Incentive Match Plan for Employees (SIMPLE) IRAs. Contributions to these plans are typically deductible as business expenses, effectively reducing your taxable income.

Educator Expenses

Teachers and other eligible educators incur significant out-of-pocket expenses for their classrooms. The IRS provides a deduction to help offset these costs.

- Qualified Expenses: Eligible educators can deduct up to a certain amount (adjusted annually for inflation) for unreimbursed expenses they paid for books, supplies, equipment, and other materials used in their teaching. This deduction is specifically for K-12 educators.

Health Savings Account (HSA) Deductions

HSAs offer a triple tax advantage for individuals with high-deductible health plans (HDHPs). Contributions made to an HSA are deductible above the line.

- Tax-Deductible Contributions: Any money you contribute to your HSA is deductible from your gross income. This reduces your taxable income, and the funds grow tax-free. Withdrawals for qualified medical expenses are also tax-free.

Self-Employment Tax Deductions

For individuals who are self-employed, a portion of their self-employment taxes can be deducted.

- Deducting Half of Self-Employment Tax: Self-employment tax covers Social Security and Medicare taxes for individuals who work for themselves. You are generally allowed to deduct one-half of the self-employment taxes you pay. This deduction helps to level the playing field between employees (who have these taxes withheld and paid by their employer, with the employer portion being a deductible business expense) and self-employed individuals.

Student Loan Interest Deduction

The cost of higher education often comes with the burden of student loans. The interest paid on qualified student loans can be deducted.

- Interest Paid on Qualified Loans: You can deduct the interest you paid during the tax year on qualified education loans. There are income limitations for this deduction, meaning your ability to claim it may be reduced or eliminated if your AGI is above a certain level.

Alimony Paid

For divorce or separation agreements executed before January 1, 2019, alimony payments were deductible by the payer and includible as income by the recipient.

- Pre-2019 Agreements: If you are paying alimony under a pre-2019 agreement, these payments can be deducted above the line. It’s crucial to review the specific terms of your divorce decree or separation agreement and the tax laws in effect at the time it was executed.

Above-the-Line Deductions for Businesses

Beyond individual tax returns, businesses also benefit from above-the-line deductions, which are typically categorized as business expenses. These deductions reduce a business’s taxable income and can significantly impact its profitability.

Business Expenses for the Self-Employed

As mentioned earlier, self-employed individuals can deduct a variety of expenses related to their business operations. These are often referred to as “above-the-line” deductions because they reduce gross business income before calculating net earnings from self-employment.

- Operating Expenses: This includes costs such as rent for an office or workspace, utilities, supplies, advertising, professional development, and other ordinary and necessary expenses incurred in running your business.

- Depreciation: Businesses can deduct the cost of assets they use in their operations over their useful life through depreciation. This allows for a gradual deduction of the asset’s value.

- Business Insurance Premiums: Premiums paid for business liability insurance, health insurance for self-employed individuals (subject to limitations), and other business-related insurance policies are often deductible.

- Home Office Deduction: If you use a portion of your home exclusively and regularly as your principal place of business, you may be able to deduct a portion of your home expenses, such as mortgage interest, property taxes, utilities, and insurance. Strict rules apply to qualify for this deduction.

Deductions for Business Owners

For business owners, particularly those operating as sole proprietorships, partnerships, or S-corporations, certain expenses are deducted directly from their business revenue.

- Employee Wages and Benefits: Businesses can deduct wages paid to their employees, as well as the cost of employee benefits like health insurance, retirement contributions, and paid time off.

- Cost of Goods Sold (COGS): For businesses that sell products, the cost of acquiring or producing those goods is a significant deduction. This is an “above-the-line” deduction that directly reduces gross profit.

- Business Interest Expense: Interest paid on loans used for business purposes is generally deductible.

Strategic Considerations for Maximizing Above-the-Line Deductions

Effectively utilizing above-the-line deductions requires careful planning and an understanding of your financial situation. It’s not simply about knowing what deductions exist, but about strategically incorporating them into your financial life.

Proactive Planning and Record Keeping

The most effective way to benefit from above-the-line deductions is through proactive planning. This means anticipating potential deductions throughout the year and maintaining meticulous records.

- Track All Eligible Expenses: Whether it’s contributions to your IRA, student loan interest payments, or business-related expenditures, keep detailed records of all qualifying expenses. This includes receipts, invoices, and statements.

- Understand Contribution Deadlines: For retirement accounts, be aware of the deadlines for making contributions that can be deducted in a given tax year. Often, you can make contributions up to the tax filing deadline of the following year.

- Consult a Tax Professional: For complex situations or if you’re unsure about the eligibility of certain expenses, consulting with a qualified tax advisor or Certified Public Accountant (CPA) is highly recommended. They can provide personalized guidance and ensure you’re taking advantage of all available deductions.

Evaluating Your Financial Goals

Above-the-line deductions often align with broader financial goals, particularly those related to saving for retirement or managing education costs.

- Retirement Savings: Prioritizing contributions to tax-advantaged retirement accounts like Traditional IRAs, SEP IRAs, or SIMPLE IRAs can provide significant tax benefits now and secure your financial future.

- Debt Management: Deducting student loan interest can make managing education debt more financially feasible.

- Business Growth: For entrepreneurs, leveraging business expense deductions is crucial for reinvesting profits and fostering sustainable growth.

Staying Informed About Tax Law Changes

Tax laws are subject to change. What is deductible today may not be in the future, and new deductions may be introduced.

- Regularly Review Tax Law Updates: Stay informed about changes in tax legislation that could affect your eligibility for above-the-line deductions. The IRS website and reputable financial news sources are good places to find this information.

- Adapt Your Strategy: Be prepared to adjust your financial planning and tax strategies in response to legislative changes.

By understanding the mechanics, identifying common examples, and adopting a strategic approach, you can effectively leverage above-the-line deductions to reduce your tax liability, improve your financial health, and achieve your financial goals.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.