In the rapidly evolving landscape of the digital economy, the way we handle money has shifted from physical wallets to digital interfaces. Among the most innovative tools to emerge in recent years is the virtual prepaid card. While traditional banking once relied on plastic cards and brick-and-mortar branches, the rise of fintech has introduced a more flexible, secure, and efficient way to manage personal and business finances.

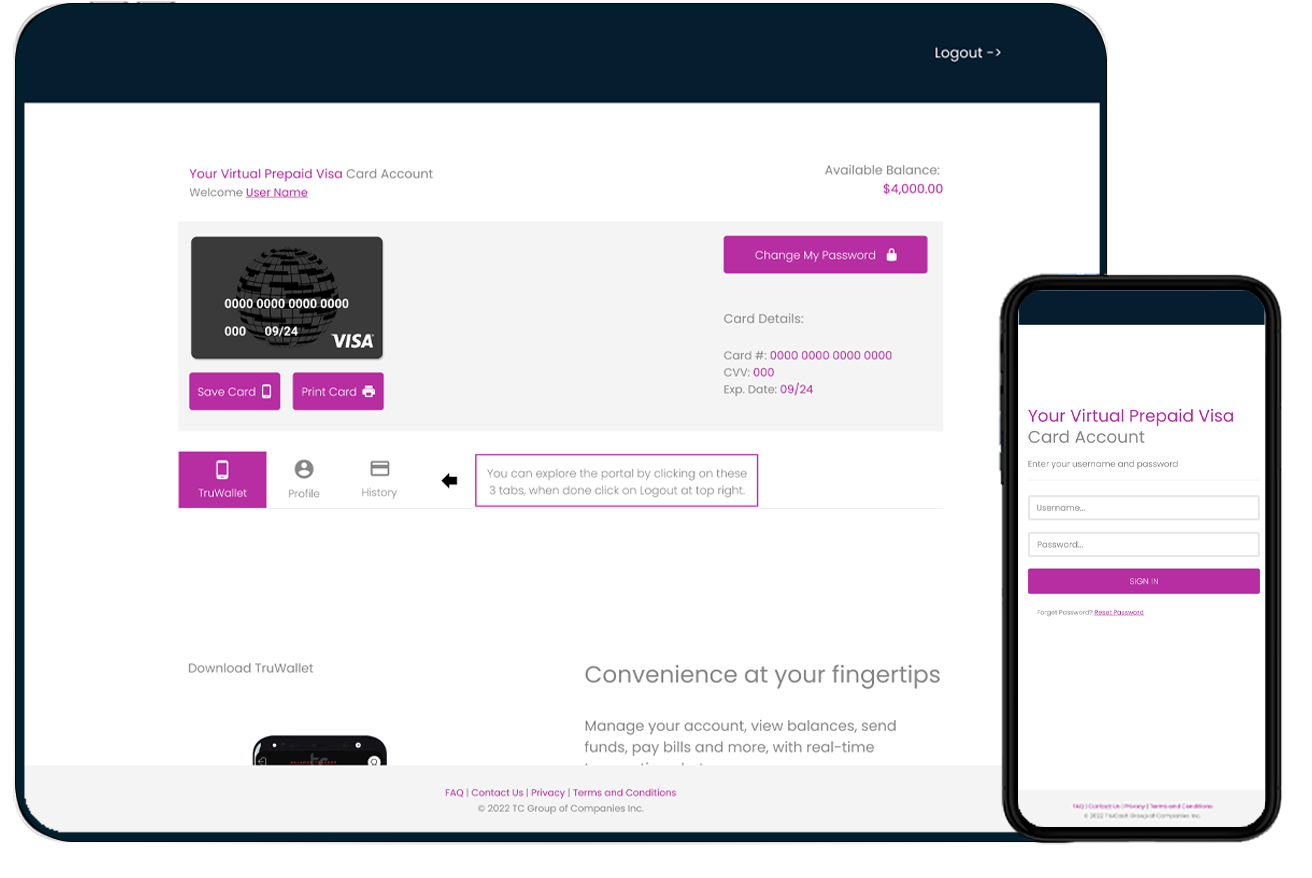

A virtual prepaid card is essentially a digital version of a standard prepaid Visa or Mastercard. It exists entirely online, consisting of a 16-digit card number, an expiration date, and a CVV code, but without the physical plastic. Because it is “prepaid,” it is not linked to a credit line; instead, you load it with a specific amount of funds before use. This guide explores the mechanics of virtual prepaid cards, their strategic role in personal finance, and why they have become an essential tool for the modern consumer.

Understanding the Mechanism of Virtual Prepaid Cards

To fully appreciate the value of a virtual prepaid card, one must understand how it functions within the global payment ecosystem. Unlike a traditional debit card linked to a checking account, or a credit card that relies on a borrowed limit, a virtual prepaid card acts as an isolated financial reservoir.

How Virtual Cards Differ from Physical Ones

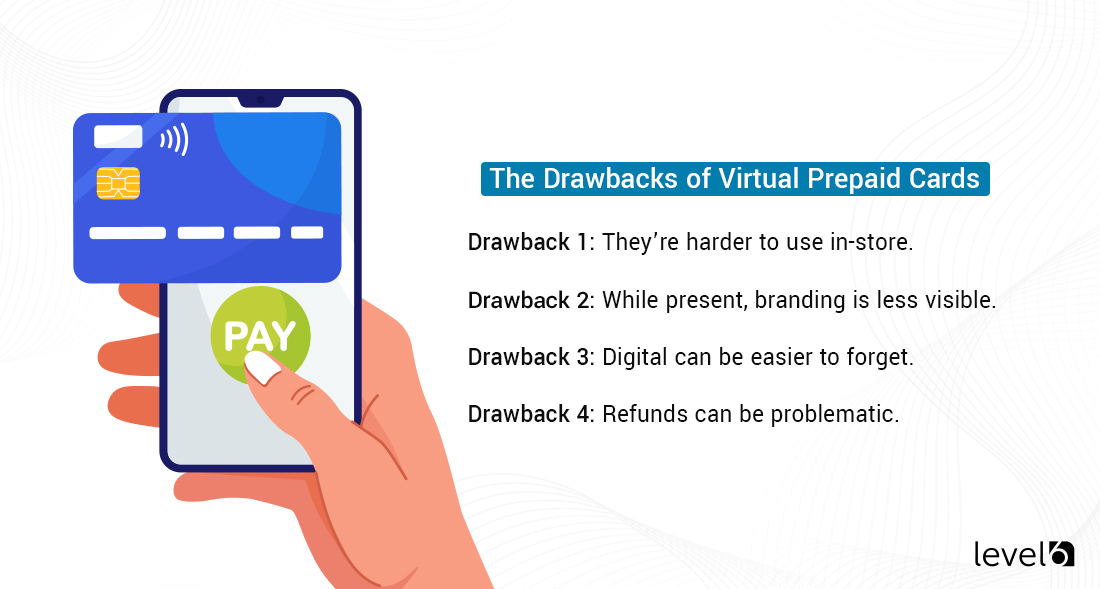

The primary difference between a physical and virtual card is the medium of existence. While a physical card can be used for “card-present” transactions—such as swiping at a grocery store—a virtual card is designed specifically for “card-not-present” transactions. These include online shopping, subscription services, and in-app purchases.

Furthermore, virtual cards offer a level of agility that physical cards cannot match. A physical card can take 7 to 10 business days to arrive in the mail. In contrast, a virtual prepaid card can be generated instantly through a mobile app or web portal. Once the card is issued and funded, it is ready for immediate use, making it an ideal solution for urgent financial needs or spontaneous online purchases.

The Technology Behind Instant Issuance

The “instant” nature of virtual cards is powered by sophisticated financial APIs (Application Programming Interfaces). When a user requests a card, the issuing platform communicates with payment networks like Visa or Mastercard to generate a unique set of credentials. These credentials are encrypted and stored within a secure digital wallet. Because there is no manufacturing or shipping involved, the cost of issuance is significantly lower, which often results in fewer fees for the end-user.

The Strategic Role of Virtual Cards in Personal Finance

In the realm of personal finance, control is the cornerstone of success. Virtual prepaid cards provide a level of granular control that traditional bank accounts often lack. By separating specific pools of money from your primary savings or checking account, you create a “firewall” for your budget.

Budgeting and Controlled Spending

One of the most effective ways to use a virtual prepaid card is as a budgeting tool. For example, if you allocate $400 a month for “discretionary spending” or “dining out,” you can load exactly that amount onto a virtual card. Once the funds are exhausted, the card will decline any further transactions. This prevents the “lifestyle creep” or accidental overspending that often occurs when using a primary debit card where the entire balance of a checking account is accessible.

This “envelope method” of digital budgeting allows users to categorize their spending. You might have one virtual card specifically for groceries, another for entertainment, and another for gas. By viewing the balances of these individual cards, you gain an instantaneous, real-time snapshot of your financial health in each category.

Eliminating Over-Subscription and Hidden Fees

The “subscription economy” has made it incredibly easy to sign up for services but notoriously difficult to manage them. From streaming platforms to software-as-a-service (SaaS) products, many consumers find themselves paying for forgotten subscriptions.

Virtual prepaid cards solve this through “merchant-locked” features or by simply limiting the balance. If you sign up for a free trial that requires a card, using a virtual card with a $0 or $1 balance ensures that you won’t be hit with a surprise “auto-renewal” fee if you forget to cancel. For active subscriptions, you can load only the exact monthly fee, ensuring the service cannot draw more than authorized.

Enhancing Security in the Digital Economy

As online commerce grows, so does the risk of data breaches and identity theft. Using a primary debit or credit card for every online transaction exposes your most sensitive financial data to potential hackers. Virtual prepaid cards serve as a vital layer of digital security.

Protecting Your Primary Bank Account

When you use a virtual prepaid card, the merchant never sees your actual bank account details. If a website you shopped at suffers a data breach, the hackers only gain access to a card number that is likely low on funds or can be deleted instantly. This isolation is critical; it ensures that a compromised virtual card does not lead to a drained checking account or a compromised identity.

Most virtual card providers allow users to “freeze” or “delete” a card with a single click in an app. If you suspect suspicious activity, you can kill the card immediately and generate a new one, avoiding the hassle of calling a bank to cancel a physical card and waiting two weeks for a replacement.

Single-Use vs. Multi-Use Virtual Cards

Many financial platforms now offer “Single-Use” or “Burner” virtual cards. These cards are designed to expire automatically after one transaction. This is the ultimate security measure for shopping on unfamiliar websites. Once the payment is processed, the card number becomes invalid, making it useless to any bad actors who might attempt to use it again. Multi-use virtual cards, on the other hand, are better suited for recurring payments like Netflix or utilities, where you want the convenience of a stable number but the security of a limited balance.

Integrating Virtual Cards into Business and Side Hustles

For entrepreneurs, freelancers, and small business owners, virtual prepaid cards are more than just a convenience—they are a tool for operational efficiency. Managing business expenses requires a high degree of organization and a clear paper trail for tax purposes.

Managing Corporate Expenses and Freelance Tools

Freelancers often juggle multiple software subscriptions, domain renewals, and advertising costs. By using dedicated virtual cards for different projects or business functions, it becomes much easier to track overhead. For small business owners with employees, virtual cards can be issued to staff members with pre-set spending limits. This eliminates the need for reimbursement cycles and gives the owner complete oversight of company spending in real-time.

Global Payments and Currency Conversion

Many virtual prepaid card providers are built for the global market, offering competitive exchange rates and low foreign transaction fees. For those earning an online income in different currencies—such as a freelancer getting paid in USD while living in Europe—virtual cards can be a cost-effective way to hold and spend multiple currencies without being penalized by traditional bank conversion markups.

How to Choose and Set Up Your First Virtual Prepaid Card

Getting started with a virtual prepaid card is a straightforward process, but it requires a bit of due diligence to ensure you are choosing a provider that aligns with your financial goals.

Key Features to Look For

When evaluating virtual card providers, consider the following:

- Fee Structure: Does the provider charge a monthly maintenance fee, a loading fee, or an issuance fee? Look for transparent pricing.

- App Interface: Since virtual cards are managed digitally, the mobile app should be intuitive and offer real-time notifications.

- Spending Limits: Ensure the card allows for the transaction volumes you anticipate.

- Security Features: Does the provider offer two-factor authentication (2FA) and the ability to freeze cards instantly?

- Compatibility: Check if the card can be added to Apple Pay, Google Pay, or Samsung Pay for use at physical NFC terminals.

A Step-by-Step Guide to Getting Started

- Select a Provider: Choose a reputable fintech company or a digital bank that offers virtual card services.

- Verification: Complete the “Know Your Customer” (KYC) process, which usually involves providing a form of ID and verifying your email or phone number.

- Link a Funding Source: Connect your primary bank account, debit card, or even a crypto wallet to load funds onto the platform.

- Create Your Card: Within the app, select the option to “Create a Virtual Card.” You can often customize the name (e.g., “Amazon Card” or “Marketing Expenses”).

- Set a Limit: Decide how much money to move from your main platform balance to the specific virtual card.

- Start Shopping: Use the 16-digit number, expiry, and CVV just as you would with a physical card.

In conclusion, the virtual prepaid card is a powerful financial instrument that addresses the unique challenges of the 21st-century consumer. Whether you are looking to tighten your budget, protect your identity from hackers, or manage a growing side hustle, virtual cards offer a level of flexibility and security that traditional banking cannot match. By integrating these digital tools into your financial routine, you take a significant step toward smarter, safer, and more intentional money management.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.