A Venmo account serves as a pivotal tool in the modern personal finance landscape, fundamentally altering how individuals manage peer-to-peer (P2P) payments and handle shared expenses. At its core, Venmo is a mobile payment service designed to simplify the transfer of money between friends, family, and even some businesses, acting as a digital wallet and a social financial platform. Understanding a Venmo account means recognizing its utility in managing everyday financial interactions, from splitting dinner bills to contributing to group gifts, all while maintaining a digital record of these transactions. It integrates seamlessly into the financial habits of millions, providing a convenient alternative to cash or traditional bank transfers for smaller, frequent financial exchanges.

Venmo’s Role as a Personal Financial Tool

Venmo has carved out a significant niche as an indispensable financial tool, particularly for personal money management. Its design prioritizes ease of use and instant gratification, which are crucial attributes for financial tools aimed at facilitating day-to-day transactions. For many, a Venmo account is synonymous with quick and hassle-free financial interactions, underpinning its status as a primary conduit for informal money transfers.

Simplifying Peer-to-Peer Payments

The most prominent function of a Venmo account is to simplify peer-to-peer payments. In an increasingly cashless society, the need for an efficient method to transfer small sums of money among individuals has grown exponentially. Venmo addresses this by allowing users to send and receive funds directly from their mobile devices with just a few taps. This functionality eliminates the need for carrying cash or dealing with the complexities and delays often associated with traditional bank transfers or checks. From a personal finance perspective, this simplification means better liquidity for immediate needs and reduced friction in social or communal financial arrangements. Users can quickly settle debts, pay back loans to friends, or contribute to shared costs without the inconvenience of physical money or the cumbersome process of exchanging banking details. The speed of these transactions, often instantaneous, is a key financial benefit, ensuring that funds are available when needed.

Managing Shared Expenses

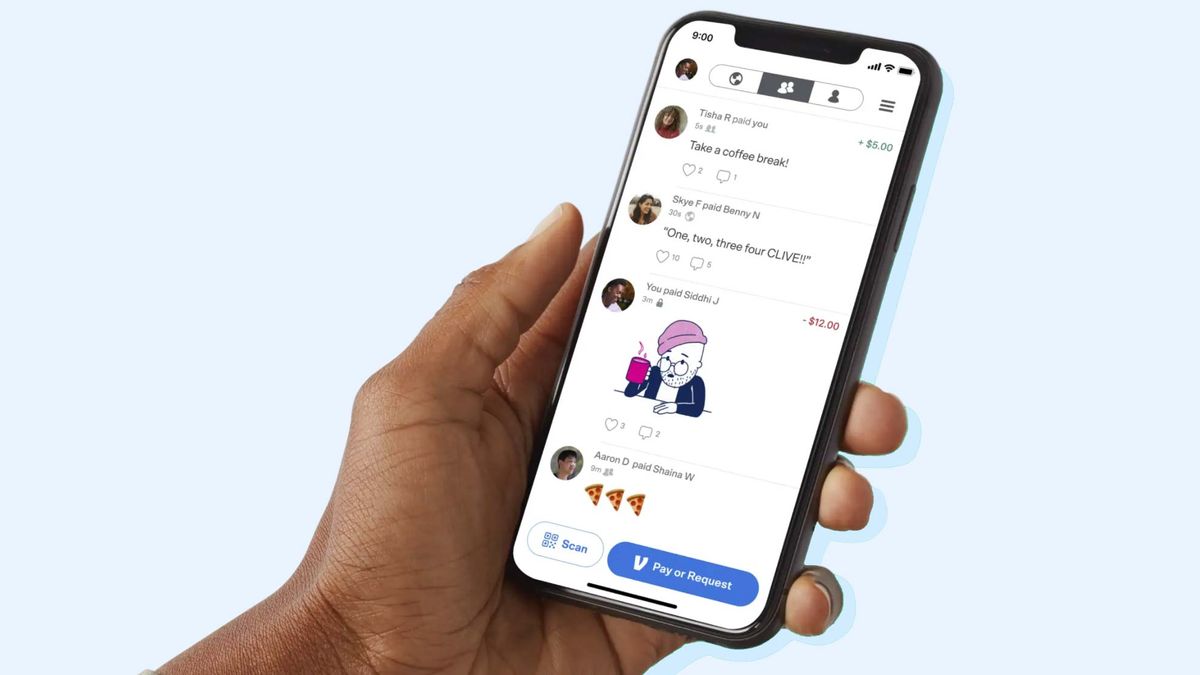

Beyond simple P2P transfers, a Venmo account excels in managing shared expenses, making it an invaluable tool for budgeting and communal financial planning. Whether it’s splitting rent among roommates, dividing the cost of a group vacation, or sharing the bill at a restaurant, Venmo provides an intuitive way to track and settle these financial obligations. The platform’s social feed, while optional, also serves as a light record of transactions, offering a glance at recent financial movements among trusted contacts. For individuals seeking to maintain clear financial boundaries and avoid awkward conversations about money, Venmo offers a neutral and efficient mechanism. This feature supports better personal financial hygiene by enabling prompt settlement of shared costs, thereby preventing the accumulation of small debts that can complicate personal budgets. From a financial planning standpoint, using Venmo for shared expenses can help individuals adhere to spending limits by making it easier to track and recover their share of costs, ensuring that personal funds are not disproportionately absorbed by group activities.

Setting Up and Funding Your Financial Transactions

Establishing and managing a Venmo account involves a straightforward process, but understanding the financial implications of account setup and funding sources is crucial for effective money management. The integration of personal banking information with a third-party payment application necessitates a keen awareness of how funds move into and out of your Venmo balance.

Account Creation and Verification for Financial Security

Creating a Venmo account is the initial step to leveraging its financial capabilities. This process typically involves downloading the app, providing basic personal information such as your name, email address, and phone number, and creating a secure password. Crucially, Venmo requires users to link a financial instrument, predominantly a bank account or debit card, to their profile. This linking process is not merely for convenience; it’s a fundamental aspect of financial security and regulatory compliance. Venmo, like other financial tools, verifies user identities to prevent fraud, money laundering, and other illicit financial activities. This often involves micro-deposit verification (sending small, refundable amounts to your linked bank account for you to confirm) or direct credential verification. For personal finance, this verification step is a safeguard, ensuring that transactions are tied to legitimate financial identities, which in turn protects users from unauthorized access and potential financial losses. A verified account also typically comes with higher transaction limits, providing greater flexibility for managing larger sums of money.

Linking Funding Sources and Managing Your Venmo Balance

Once an account is created and verified, users can link various funding sources to their Venmo profile, which is key to facilitating financial transactions. The primary funding methods include a bank account, debit cards, and credit cards. Each method has distinct financial implications. Transfers sent using a linked bank account or debit card are generally free of charge for standard transactions. However, transactions funded by a credit card typically incur a 3% fee, a crucial consideration for personal budgeting and avoiding unnecessary costs. This fee structure encourages users to prioritize debit or bank account transfers to maximize their financial resources.

Your Venmo balance represents the total amount of money you have available within the app, whether received from other users or added from your linked accounts. Managing this balance effectively is a core component of using Venmo as a financial tool. Funds can be held in your Venmo balance for future payments, or they can be transferred out to a linked bank account. Standard transfers to a bank account are free but may take 1-3 business days to process. For immediate access to funds, Venmo offers an instant transfer option, which typically incurs a small fee (e.g., 1.75% with a minimum and maximum fee). Understanding these options and their associated costs is vital for managing cash flow and ensuring financial liquidity, allowing users to make informed decisions about when and how to move their money.

Understanding Transaction Fees and Financial Considerations

Navigating the financial landscape of Venmo involves a clear understanding of its fee structure. While many core functionalities are free, certain transactions carry costs that can impact personal budgeting and overall financial planning. Awareness of these fees empowers users to make economically sound choices when utilizing their Venmo account.

Costs Associated with Instant Transfers and Credit Card Payments

One of the most significant financial considerations for Venmo users relates to instant transfers. While the convenience of immediately moving funds from your Venmo balance to a linked bank account is undeniable, this expedited service comes at a cost. Venmo typically charges a percentage fee (e.g., 1.75% as of recent updates, with minimum and maximum caps) for instant transfers. For individuals who frequently need immediate access to their funds, these small fees can accumulate over time, incrementally affecting their available balance. It’s a trade-off between speed and cost, and savvy financial management dictates weighing the urgency of access against the expense.

Similarly, funding payments using a linked credit card incurs a transaction fee, generally around 3% of the payment amount. This fee is a critical factor for users to consider. While using a credit card might offer rewards points or extend payment flexibility, the additional 3% charge means that every dollar spent via credit card on Venmo effectively costs $1.03. From a personal finance perspective, this makes credit card funding a less economical option for routine P2P payments, especially when a free alternative (debit card or bank account) is available. Users aiming to minimize transaction costs should prioritize funding payments directly from their bank account or a debit card.

The Free Nature of Standard Transfers and Debit Card Usage

Despite the fees associated with instant transfers and credit card payments, a substantial portion of Venmo’s core financial services remains free, offering significant value to users. Standard transfers from your Venmo balance to a linked bank account, which typically process within 1-3 business days, are entirely free. This option provides a cost-effective way to move money out of your Venmo account without incurring additional charges, making it ideal for non-urgent financial transfers.

Furthermore, sending money to others using a linked bank account or a debit card does not incur any fees. This zero-cost model for the most common P2P transactions is a major draw for Venmo users. It allows individuals to seamlessly split bills, repay friends, or contribute to group funds without worrying about hidden charges eroding their contributions or receipts. This free usage greatly enhances Venmo’s utility as a cost-efficient financial tool for everyday money management, reinforcing its position as a go-to platform for many personal financial interactions. Understanding these free options is key to leveraging Venmo for optimal financial benefit while avoiding unnecessary expenses.

Ensuring Financial Security and Privacy for Your Money

In the realm of digital financial tools, the security and privacy of personal funds are paramount concerns. A Venmo account, while offering unparalleled convenience, also demands user awareness regarding the measures in place to protect financial assets and personal information. Understanding these safeguards and exercising due diligence are crucial for maintaining a secure financial profile.

Safeguarding Transactions and Account Access

Venmo employs a multi-layered approach to safeguard transactions and protect account access, similar to established financial institutions. This includes data encryption, fraud monitoring, and user authentication processes. All financial transactions are encrypted to protect sensitive information from unauthorized interception. Venmo’s fraud detection algorithms continuously monitor activity for suspicious patterns, flagging and often preventing potentially fraudulent transactions. For users, account security starts with strong password practices and enabling multi-factor authentication (MFA). MFA, which typically involves verifying login attempts through a registered phone number or email, adds an essential layer of protection, making it significantly harder for unauthorized individuals to access your account even if they somehow obtain your password.

From a personal finance standpoint, actively utilizing these security features is a critical step in risk management. Regularly reviewing transaction history for any unfamiliar activity, being cautious of phishing attempts, and promptly reporting any suspicious behavior are all responsibilities that fall on the account holder. Venmo also offers purchase protection for eligible transactions, providing a layer of financial recourse in disputes with certain approved merchants, further bolstering financial security for some types of payments. Educating oneself about these measures empowers users to manage their financial risk effectively within the Venmo ecosystem.

Navigating Privacy Settings for Financial Discretion

Beyond transactional security, Venmo offers robust privacy settings that allow users to control the visibility of their financial activities. By default, many Venmo transactions have a social component, appearing in a public feed. However, users have the option to adjust the privacy level of each transaction to “friends only” or “private.” For individuals who prefer to keep their financial movements discreet, setting all transactions to “private” by default is a recommended financial practice. This prevents personal financial dealings from being publicly visible, maintaining a higher degree of financial privacy.

The choice of privacy settings reflects a personal decision regarding the balance between social transparency and financial discretion. While the public feed can foster a sense of community and simplify tracking shared expenses among close contacts, many users prioritize keeping their financial data confidential. Venmo’s flexibility in this area ensures that account holders can tailor their experience to match their comfort level with financial visibility. Understanding and actively managing these privacy settings is integral to safeguarding personal financial information and ensuring that one’s financial interactions remain as private as desired, aligning with broader personal finance principles of data protection and confidentiality.

Expanding Venmo’s Utility in Your Financial Ecosystem

A Venmo account has evolved beyond simple P2P payments, now offering features that integrate more deeply into a user’s broader financial ecosystem. These expanded utilities position Venmo not just as a casual payment app, but as a more comprehensive financial tool capable of supporting various financial needs, from business transactions to more traditional banking services.

Utilizing Venmo for Business Transactions and Income

For entrepreneurs, freelancers, and small businesses, a Venmo account can serve as a streamlined method for managing income and expenses. Venmo offers business profiles, which allow users to accept payments from customers for goods and services. While personal Venmo accounts are primarily for P2P transfers among friends and family, business profiles are designed to handle commercial transactions, often with different fee structures (e.g., a small percentage fee per transaction for the seller). This functionality makes Venmo a convenient financial tool for micro-businesses or individuals seeking to monetize side hustles without the complexities of traditional merchant accounts.

From a financial management perspective, using Venmo for business transactions provides a clear digital record of income, simplifying bookkeeping and tax preparation for smaller operations. It offers a low-barrier entry point for accepting digital payments, which can be crucial for expanding customer reach in an increasingly digital economy. Understanding the fees associated with business transactions and the tax implications of reported income is essential for anyone utilizing Venmo in this capacity, ensuring compliance and effective financial planning.

Exploring Additional Financial Products

Venmo has broadened its product offerings to include more traditional financial tools, further integrating into users’ financial lives. These include the Venmo Debit Card and the Venmo Credit Card. The Venmo Debit Card, linked directly to your Venmo balance, allows users to spend funds from their Venmo account anywhere Mastercard is accepted. This effectively turns the Venmo balance into a fully functional checking account substitute for everyday purchases, offering cash-back rewards on eligible spending. This provides a direct financial utility for the funds held within the app, removing the need for frequent transfers to an external bank account.

The Venmo Credit Card, issued by Synchrony Bank, offers cashback rewards on top spending categories, which are automatically deposited into the user’s Venmo account. This product positions Venmo not just as a payment app, but as a participant in the credit market, offering a way for users to earn rewards on their spending and build credit history. For financially savvy individuals, these products offer opportunities to optimize spending, earn rewards, and manage their cash flow more efficiently, provided they are used responsibly. Understanding the terms, fees, and rewards structures of these additional financial products is crucial for leveraging them effectively within one’s personal finance strategy.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.