Navigating the world of personal finance can often feel like venturing into uncharted territory. For many, the desire to achieve financial goals, whether it’s securing a comfortable retirement, planning for a child’s education, or optimizing investment portfolios, leads them to seek professional guidance. This is where financial advisors come into play. However, a crucial question that arises for anyone considering their services is: “What is a typical fee for a financial advisor?” Understanding advisor compensation models is not just about knowing the cost; it’s about comprehending how their interests are aligned with yours, ensuring you receive valuable advice that truly serves your best financial interests.

The fee structure of a financial advisor can be complex, with various models and variations that can significantly impact the overall cost of their services. These fees are not a one-size-fits-all proposition and depend on several factors, including the advisor’s experience, the scope of services offered, the complexity of your financial situation, and the specific firm they represent. For clients, demystifying these fees is essential for making an informed decision and ensuring they get the most value from their financial partnership. This article will delve into the common fee structures employed by financial advisors, explain how these fees are calculated, and provide insights into what constitutes a “typical” fee, empowering you to make a more confident choice.

Understanding the Landscape of Financial Advisor Fees

The compensation of a financial advisor is a critical aspect of the client-advisor relationship. It’s not just about the bottom line; it’s about understanding the incentives and potential conflicts of interest that can arise from different fee models. Advisors are compensated in a variety of ways, and each method carries its own implications for both the advisor and the client. Recognizing these structures is the first step in evaluating the true cost of financial advice and ensuring that the advisor’s motivations are squarely aligned with your financial well-being.

Fee-Only Advisors: A Fiduciary Standard

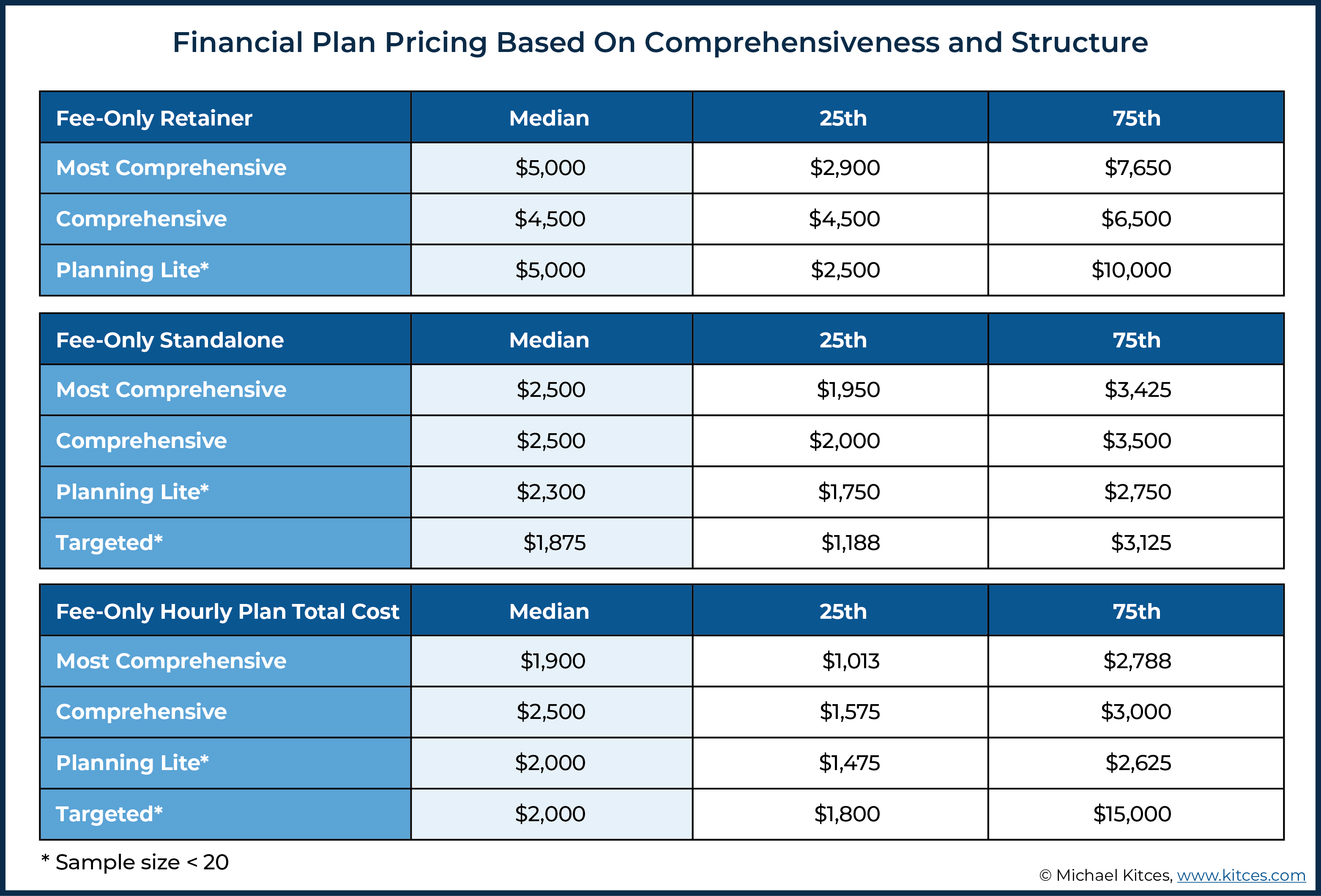

One of the most transparent and often preferred models is the fee-only compensation structure. Fee-only advisors are compensated solely by their clients. This means they do not receive any commissions or incentives from selling financial products like mutual funds, insurance policies, or annuities. This independence is crucial because it removes the potential for conflicts of interest. When an advisor is solely paid by you, their primary motivation is to provide objective advice that best suits your needs, rather than recommending products that might generate a commission for them.

-

Hourly Fees: Some fee-only advisors charge by the hour. This model is suitable for clients who need specific, project-based advice, such as reviewing an investment portfolio, creating a budget, or getting guidance on a particular financial decision. Hourly rates can vary significantly, typically ranging from $100 to $400 per hour or even more for highly specialized advisors or those in high-cost-of-living areas. The total cost depends entirely on the time spent addressing your needs.

-

Project-Based Fees (Flat Fees): For clearly defined services, such as developing a comprehensive financial plan, a fee-only advisor might charge a flat fee. This provides cost certainty for the client, as they know the exact price upfront. A financial plan might cost anywhere from $1,000 to $5,000 or more, depending on the complexity of the client’s situation and the depth of the analysis provided. This can be an efficient option for individuals seeking a detailed roadmap for their financial future.

-

Assets Under Management (AUM) Fees: This is perhaps the most common fee-only model for ongoing financial planning and investment management. Advisors charge a percentage of the total assets they manage on your behalf. Typical AUM fees range from 0.5% to 1.5% annually. For example, if you have $500,000 invested and the advisor charges a 1% AUM fee, you would pay $5,000 per year. Fee schedules often include breakpoints, meaning the percentage fee decreases as your assets increase, rewarding larger clients with a lower overall rate. This model aligns the advisor’s compensation directly with the growth and preservation of your wealth.

Commission-Based Advisors: Product Sales and Potential Conflicts

Commission-based advisors, often referred to as brokers, earn their income through commissions generated by selling financial products. When a commission-based advisor recommends a specific investment product, such as a mutual fund, annuity, or insurance policy, they receive a portion of the sales charge or commission paid by the product provider. This model can be appealing to some clients who may perceive it as “free” advice, as there are no direct fees paid by the client upfront.

However, this model inherently creates a potential for conflicts of interest. An advisor compensated by commission might be incentivized to recommend products that offer higher commissions, even if they are not the absolute best option for the client. This doesn’t mean all commission-based advisors act unethically; many strive to provide good advice. But the structure itself introduces a layer of scrutiny that clients must be aware of. It’s crucial for clients to understand that when an advisor is compensated by commission, the cost is indirectly passed on through the product’s fees or expenses, which can erode investment returns over time.

Fee-Based Advisors: A Hybrid Approach

The “fee-based” model can be the most confusing, as it combines elements of both fee-only and commission-based compensation. Fee-based advisors are registered to sell investment products and may earn commissions on these sales, while also charging fees for their advisory services, such as AUM fees or financial planning fees. This hybrid approach can sometimes obscure where the advisor’s loyalties lie.

For instance, a fee-based advisor might charge a lower AUM fee than a purely fee-only advisor but also earn commissions on specific products they recommend. This can create a scenario where the advisor benefits from both the client’s assets and the sale of financial products. When considering a fee-based advisor, it is paramount to have a frank discussion about their compensation structure, understand all potential revenue streams, and ensure they are always acting in your best fiduciary interest, even when commissions are involved. The regulatory landscape surrounding fee-based advisors is complex, and transparency is key to building trust.

Factors Influencing Financial Advisor Fees

Beyond the compensation model, several other factors play a significant role in determining the typical fee you might encounter when hiring a financial advisor. Understanding these variables will help you set realistic expectations and identify advisors who offer services that align with your financial needs and budget.

Scope of Services and Advisor Expertise

The breadth and depth of the services a financial advisor provides will directly impact their fees. A client seeking a comprehensive financial plan, including retirement planning, estate planning, tax strategies, and investment management, will naturally incur higher costs than someone looking for advice on a single, specific financial goal. Advisors who offer a more holistic approach often charge more because they are providing a wider range of expertise and ongoing support.

Furthermore, the advisor’s experience, credentials, and specialization also influence their fees. An advisor with decades of experience, advanced certifications (such as Certified Financial Planner™ or CFP®), and a proven track record of success may command higher fees than a newly licensed advisor. Specialized expertise in niche areas, like working with small business owners, high-net-worth individuals, or those navigating complex tax situations, can also justify higher compensation.

Client’s Financial Situation and Assets

The complexity of a client’s financial situation is a direct driver of the advisor’s fee. Individuals with intricate financial lives, including multiple investment accounts, diverse income streams, significant debt, or unique tax circumstances, will require more time and specialized knowledge from their advisor. This complexity often translates into higher fees, particularly for advisors who charge based on assets under management (AUM) or offer project-based financial planning.

For AUM-based fees, the total amount of assets the advisor manages for you is the primary determinant of their compensation. While the percentage might remain the same, a larger asset base will result in a higher dollar amount paid to the advisor. Conversely, clients with simpler financial needs or fewer assets may find advisors with hourly or flat-fee structures more cost-effective. Some advisors also have minimum asset requirements, meaning they may not take on clients with less than a certain amount of investable assets, which can indirectly influence the typical fee you encounter based on your wealth.

What Constitutes a “Typical” Fee?

Defining a “typical” fee for a financial advisor is challenging due to the wide array of compensation models and service offerings. However, by examining the common structures, we can provide a general range and outline what most clients can expect to pay. It’s crucial to remember that these figures are averages and can fluctuate significantly based on the factors discussed earlier.

Fee-Only Advisor Fees: A Closer Look

For fee-only advisors, the “typical” fee is best understood by their different charging methods:

-

AUM Fees: As mentioned, this is a prevalent model. A common range for AUM fees is 0.75% to 1.25% annually. This means for every $100,000 managed, you might pay between $750 and $1,250 per year. Many advisors offer tiered pricing, where the percentage decreases as your assets grow. For example, the first $250,000 might be charged at 1%, the next $500,000 at 0.8%, and assets above $750,000 at 0.6%. This structure encourages long-term relationships and incentivizes wealth accumulation.

-

Hourly Fees: Clients seeking specific advice without ongoing management might opt for an hourly rate. Typical rates for fee-only financial planners can range from $150 to $350 per hour. A single financial planning session or a review of your current strategy might take anywhere from 2 to 10 hours, leading to a total cost between $300 and $3,500 for that engagement.

-

Flat Fees: For comprehensive financial planning, a flat fee offers predictability. These fees can range widely, from $1,000 for a basic plan to $5,000 or more for a detailed, complex plan covering numerous financial aspects. This is a good option for individuals who want a detailed roadmap and are comfortable with a one-time upfront cost.

Commission-Based and Fee-Based Advisor Costs

For commission-based advisors, the cost is embedded within the products they sell. This can manifest as upfront sales charges (loads) on mutual funds, ongoing expense ratios that are higher than no-load funds, or internal costs of annuities and insurance policies. These embedded costs can significantly impact long-term returns and are often difficult for consumers to precisely quantify upfront.

Fee-based advisors present a blended picture. They might charge a lower AUM fee, perhaps 0.5% to 1%, but then earn commissions on recommended products. The total cost can be harder to calculate precisely because it depends on the products chosen and the commissions generated. It’s essential to ask for a clear breakdown of all potential revenue streams and how they align with your best interests.

Making an Informed Decision: Questions to Ask Your Financial Advisor

When you’ve identified potential financial advisors and are ready to discuss their services, asking the right questions is paramount to ensuring you understand their compensation and how it aligns with your financial goals. Transparency is the bedrock of a strong client-advisor relationship, and proactive inquiry can prevent misunderstandings and potential conflicts down the line.

Clarifying Compensation Structures

The first and most critical step is to clearly understand how the advisor is compensated. Don’t hesitate to ask direct questions.

-

“How are you compensated for your services?” This question should elicit a clear explanation of their fee structure (fee-only, commission-based, or fee-based). If they are fee-based, ask for a detailed breakdown of how they earn money from both fees and commissions.

-

“Are you a fiduciary?” A fiduciary is legally obligated to act in your best interest. Fee-only advisors are typically fiduciaries. If an advisor is not a fiduciary, they are held to a “suitability” standard, meaning their recommendations only need to be suitable for you, not necessarily the absolute best option. Clarifying this status is vital.

-

“What are your specific fees for the services I need?” Ask for exact percentages, hourly rates, or flat fees. Understand if there are any additional charges or hidden costs. For AUM fees, ask about any breakpoints or tiered pricing structures.

-

“Can you provide me with a sample of your ADV Part 2 brochure or Firm Brochure?” This document is required by regulators and provides detailed information about the advisor’s services, fees, business practices, and any potential conflicts of interest.

Evaluating Value and Services Rendered

Beyond the fee itself, consider the value proposition the advisor offers. What are you actually paying for, and does it meet your expectations?

-

“What specific services are included in your fee?” Ensure you have a clear understanding of what you will receive. This might include financial planning, investment management, tax planning, estate planning, insurance review, and regular progress meetings.

-

“How often will we meet or communicate, and what will be the format of these interactions?” Understanding the frequency and nature of communication helps set expectations for ongoing engagement and support.

-

“What is your investment philosophy and approach?” This is crucial, especially if you are seeking investment management. Ensure their philosophy aligns with your risk tolerance and financial objectives.

-

“Can you provide references or testimonials from clients with similar financial situations to mine?” While not always available or permissible due to privacy, asking can sometimes provide valuable insights into their client service and success.

By diligently asking these questions and thoroughly reviewing any provided documentation, you can gain a comprehensive understanding of the fees associated with a financial advisor and make an informed decision that aligns with your financial goals and peace of mind. Remember, the most important aspect is finding an advisor whose interests are aligned with yours, ensuring you receive objective, valuable advice.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.