A trade option, commonly referred to simply as an “option,” is a versatile financial derivative instrument that grants the buyer the right, but not the obligation, to buy or sell an underlying asset at a predetermined price on or before a specified date. This contract-based investment tool is distinct from directly owning the underlying asset, offering investors leverage, hedging capabilities, and various strategic opportunities in the financial markets. Understanding options is crucial for anyone looking to navigate beyond basic stock and bond investments, as they form a fundamental component of sophisticated financial strategies, whether for risk management or speculative profit generation.

The Mechanics of Options Trading

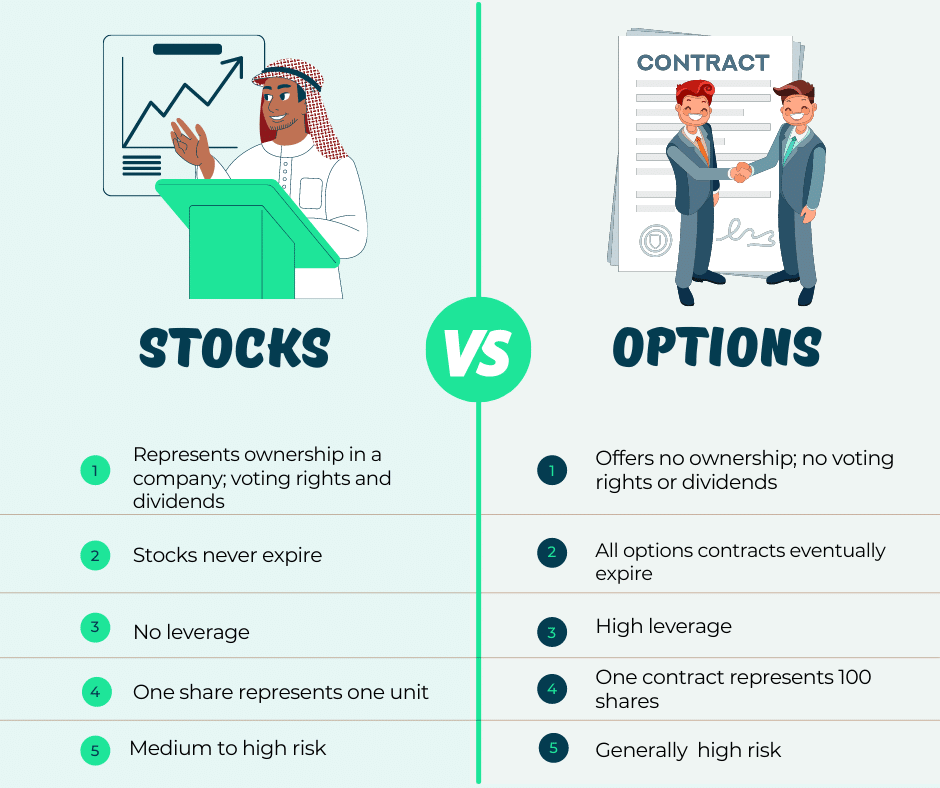

At its core, an option contract derives its value from an underlying asset, which can be stocks, exchange-traded funds (ETFs), commodities, currencies, or even market indexes. Each option contract represents 100 shares of the underlying asset in the equity markets. The interaction between buyers and sellers, coupled with specific contract terms, dictates the potential outcomes of an option trade.

Call Options vs. Put Options

The fundamental distinction in options trading lies between call options and put options:

- Call Option: A call option gives the holder the right to buy the underlying asset at a specified price (the strike price) on or before the expiration date. Investors typically buy call options when they anticipate that the price of the underlying asset will increase significantly above the strike price. If the asset’s price rises, the call option’s value will increase, allowing the holder to either sell the option for a profit or exercise it to buy the underlying shares at the lower strike price. Conversely, call sellers (writers) expect the price to remain stagnant or fall, hoping the option expires worthless so they can keep the premium.

- Put Option: A put option grants the holder the right to sell the underlying asset at a specified price (the strike price) on or before the expiration date. Investors buy put options when they expect the price of the underlying asset to decline below the strike price. If the asset’s price falls, the put option’s value will increase, enabling the holder to sell the option for a profit or exercise it to sell shares at the higher strike price. Put sellers (writers) anticipate the price to remain stable or rise, aiming for the option to expire worthless.

Buyers (Holders) vs. Sellers (Writers)

Every option transaction involves a buyer and a seller, each with distinct risk and reward profiles:

- Buyers (Holders): Pay a premium to acquire the option contract. Their maximum potential loss is limited to the premium paid. Their profit potential, particularly for call options, can be theoretically unlimited as the underlying asset’s price rises. For put options, profit potential is substantial as the asset price can fall to zero. Buyers choose to exercise their right only if it is profitable.

- Sellers (Writers): Receive the premium from the buyer. Their maximum potential profit is limited to the premium received. However, their risk profile varies significantly depending on whether the option is “covered” or “naked.” For a “naked” (uncovered) call option, the potential loss is theoretically unlimited if the underlying asset’s price skyrockets. For an uncovered put, the maximum loss is substantial, as the asset price can fall to zero, obligating the seller to buy shares at the strike price.

Key Terminology

Navigating options requires familiarity with specific terms that define the contract:

- Underlying Asset: The security, commodity, or index upon which the option contract is based.

- Strike Price (Exercise Price): The predetermined price at which the underlying asset can be bought (for a call) or sold (for a put) if the option is exercised.

- Expiration Date: The last day the option contract is valid and can be exercised. After this date, the option becomes worthless if not exercised. Options can be American-style (exercisable any time before expiration) or European-style (exercisable only at expiration). Most equity options in the US are American-style.

- Premium: The price paid by the option buyer to the option seller for the right granted by the contract. It is determined by factors such as the underlying asset’s price, strike price, time to expiration, volatility, and interest rates.

- In-the-Money (ITM), At-the-Money (ATM), Out-of-the-Money (OTM): These describe the option’s current profitability relative to the underlying asset’s price and the strike price.

- Call ITM: Underlying price > Strike price.

- Put ITM: Underlying price < Strike price.

- ATM: Underlying price = Strike price.

- Call OTM: Underlying price < Strike price.

- Put OTM: Underlying price > Strike price.

- Intrinsic Value: The immediate profit an option would yield if exercised (difference between underlying price and strike price when ITM). OTM options have zero intrinsic value.

- Time Value (Extrinsic Value): The portion of an option’s premium that exceeds its intrinsic value. It represents the value investors place on the chance that the option will move further into the money before expiration. Time value erodes as the expiration date approaches, a phenomenon known as “time decay” or “theta decay.”

Why Do Investors Use Options?

Options are powerful tools that offer a diverse range of applications for investors, extending beyond simple directional bets on asset prices. They are employed for managing risk, generating income, and speculating on market movements with significant leverage.

Hedging (Risk Management)

One of the primary uses of options is to hedge existing portfolios against adverse market movements, effectively acting as an insurance policy:

- Protecting Against Downside Risk: An investor holding shares of a stock can buy put options on that stock. If the stock’s price falls below the put’s strike price, the gain from the put option can offset some or all of the loss on the stock shares. This strategy is known as a “protective put.”

- Limiting Upside Risk: Conversely, investors can write “covered calls” against stock they own. While this strategy generates income from the premium received, it also caps the potential upside profit if the stock price rises significantly above the call’s strike price, as the shares may be called away.

Speculation (Profit Generation)

Options provide a highly leveraged way to speculate on price movements, allowing investors to control a large block of shares with a relatively small amount of capital:

- Leverage: Because an option contract controls 100 shares of the underlying asset for a fraction of the cost of buying the shares outright, a small percentage move in the underlying asset can result in a much larger percentage gain or loss for the option holder. This magnification of returns (or losses) is a key attractive feature for speculators.

- Profiting from Volatility: Strategies like straddles (buying both a call and a put with the same strike and expiration) or strangles (buying an OTM call and an OTM put) allow investors to profit from significant price movements in either direction, without necessarily predicting the specific direction.

- Generating Income: Selling options (like covered calls or cash-secured puts) allows investors to collect premiums, generating income from their portfolios, albeit with associated risks.

Portfolio Enhancement

Beyond direct hedging and speculation, options can be integrated into broader portfolio strategies:

- Generating Income from Existing Holdings: Writing covered calls against shares an investor already owns is a common strategy to generate recurring income, especially in flat or mildly bullish markets.

- Acquiring Stocks at a Discount: Selling cash-secured put options allows an investor to potentially buy shares of a company they wish to own at a lower price (the strike price) if the option is assigned. If the option expires worthless, the investor keeps the premium as income.

Risks and Considerations in Options Trading

While options offer compelling opportunities, their complexity and inherent leverage introduce significant risks that demand careful consideration and a thorough understanding before engaging.

Complexity and Learning Curve

Options trading is not for the faint of heart or the uninitiated. It involves a steep learning curve:

- Sophisticated Concepts: Understanding how various factors (underlying price, strike, time to expiration, volatility, interest rates) influence an option’s premium requires a grasp of quantitative models and market dynamics.

- Diverse Strategies: There are dozens of options strategies, ranging from simple directional plays to complex multi-leg combinations, each with unique risk-reward profiles. Mastering these requires extensive study and practice.

- Brokerage Requirements: Most brokers require investors to apply for and be approved for specific options trading levels, indicating their understanding and risk tolerance.

High-Risk, High-Reward Nature

The leverage that makes options attractive for profit also amplifies potential losses:

- Time Decay (Theta): For option buyers, time is an enemy. The time value portion of an option’s premium continuously erodes as it approaches expiration, meaning an option can lose value even if the underlying asset’s price remains stable or moves slightly in the desired direction.

- Magnified Losses: While a buyer’s maximum loss is limited to the premium paid, this premium can be lost entirely and quickly if the market moves unfavorably. For sellers of “naked” (uncovered) options, particularly calls, losses can be theoretically unlimited, potentially leading to substantial financial distress.

- Volatility Impact: Sudden spikes or drops in implied volatility can significantly impact option premiums, often against the position of the trader.

Liquidity and Spreads

Not all options are created equal in terms of market activity:

- Bid-Ask Spreads: Options on less popular or highly volatile underlying assets may have wide bid-ask spreads, making it difficult to enter or exit positions at favorable prices. This effectively increases the cost of trading.

- Early Exercise Risk: While less common for American-style equity options, there is always a possibility of early exercise, particularly for deeply in-the-money options where the underlying stock is about to pay a dividend. Sellers need to be aware of this potential obligation.

Common Options Strategies

Options trading encompasses a wide array of strategies, tailored to different market outlooks and risk tolerances.

Basic Strategies

These are foundational strategies often used by those starting in options or for straightforward market views:

- Buying Calls: A bullish strategy where the investor expects the underlying asset’s price to rise significantly. Limited risk (premium paid), theoretically unlimited profit.

- Buying Puts: A bearish or hedging strategy where the investor expects the underlying asset’s price to fall. Limited risk (premium paid), substantial profit potential.

- Selling Covered Calls: A neutral to mildly bullish/bearish strategy for income generation. An investor owns the underlying shares and sells call options against them, collecting the premium. If the stock rises above the strike, the shares may be called away.

- Selling Cash-Secured Puts: A neutral to mildly bullish strategy where an investor sells put options and simultaneously sets aside enough cash to buy the shares if the option is assigned. If the stock falls below the strike, the investor is obligated to buy shares at that price but keeps the premium. If the stock stays above the strike, the option expires worthless, and the investor keeps the premium.

More Advanced Strategies

Experienced traders often employ more complex strategies to capitalize on specific market conditions or create nuanced risk profiles:

- Spreads: Involve buying and selling options of the same type (calls or puts) on the same underlying asset with different strike prices or expiration dates. Examples include vertical spreads (bull call spread, bear put spread) designed to profit from directional moves within a limited range.

- Straddles and Strangles: Volatility strategies that involve buying (or selling) both a call and a put on the same underlying asset. Straddles use the same strike price and expiration date, while strangles use different strike prices. These profit from significant price movement (straddle/strangle buyer) or lack thereof (straddle/strangle seller).

- Iron Condors: A complex, neutral strategy designed to profit from an underlying asset remaining within a defined price range, limiting both profit and loss.

In conclusion, a trade option is a sophisticated financial instrument offering unparalleled flexibility for investors. From protecting existing portfolios through hedging to generating income or speculating on market movements with leverage, options provide a diverse toolkit. However, this versatility comes with increased complexity and risk. Success in options trading demands diligent education, a clear understanding of market dynamics, careful risk management, and a well-defined strategy. Investors new to options should start with basic strategies, thoroughly educate themselves, and consider professional advice to navigate these powerful financial tools effectively.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.