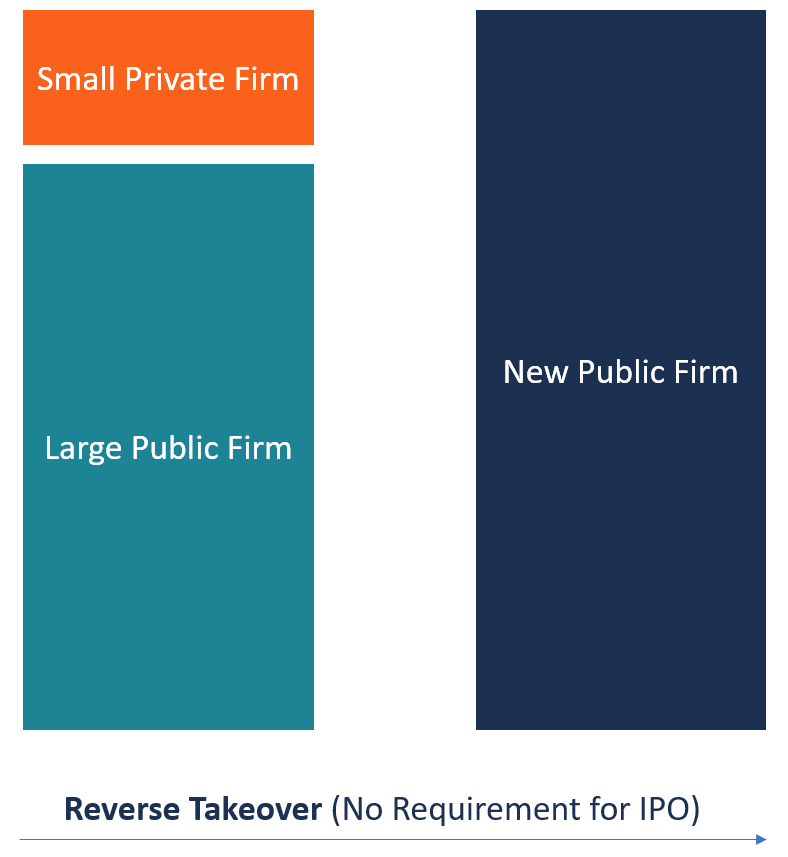

In the intricate landscape of corporate finance and public markets, the traditional path to going public—the Initial Public Offering (IPO)—is often characterized by lengthy due diligence, extensive regulatory hurdles, and substantial underwriting fees. However, there exists a strategic, albeit complex, alternative known as the reverse takeover (RTO). An RTO, frequently referred to as a “reverse merger,” allows a private company to bypass the conventional IPO process by acquiring a publicly traded company. By effectively folding into an existing public entity, the private firm gains instant access to the capital markets, drastically shortening the timeline for going public.

Understanding the mechanics of a reverse takeover requires looking past the common narrative of corporate acquisitions. While a traditional merger sees a large company absorbing a smaller one, a reverse takeover flips the power dynamic. It is a strategic maneuver where the private entity effectively takes control of the public vehicle, inheriting its ticker symbol, shareholder base, and regulatory status.

The Mechanics: How a Reverse Takeover Functions

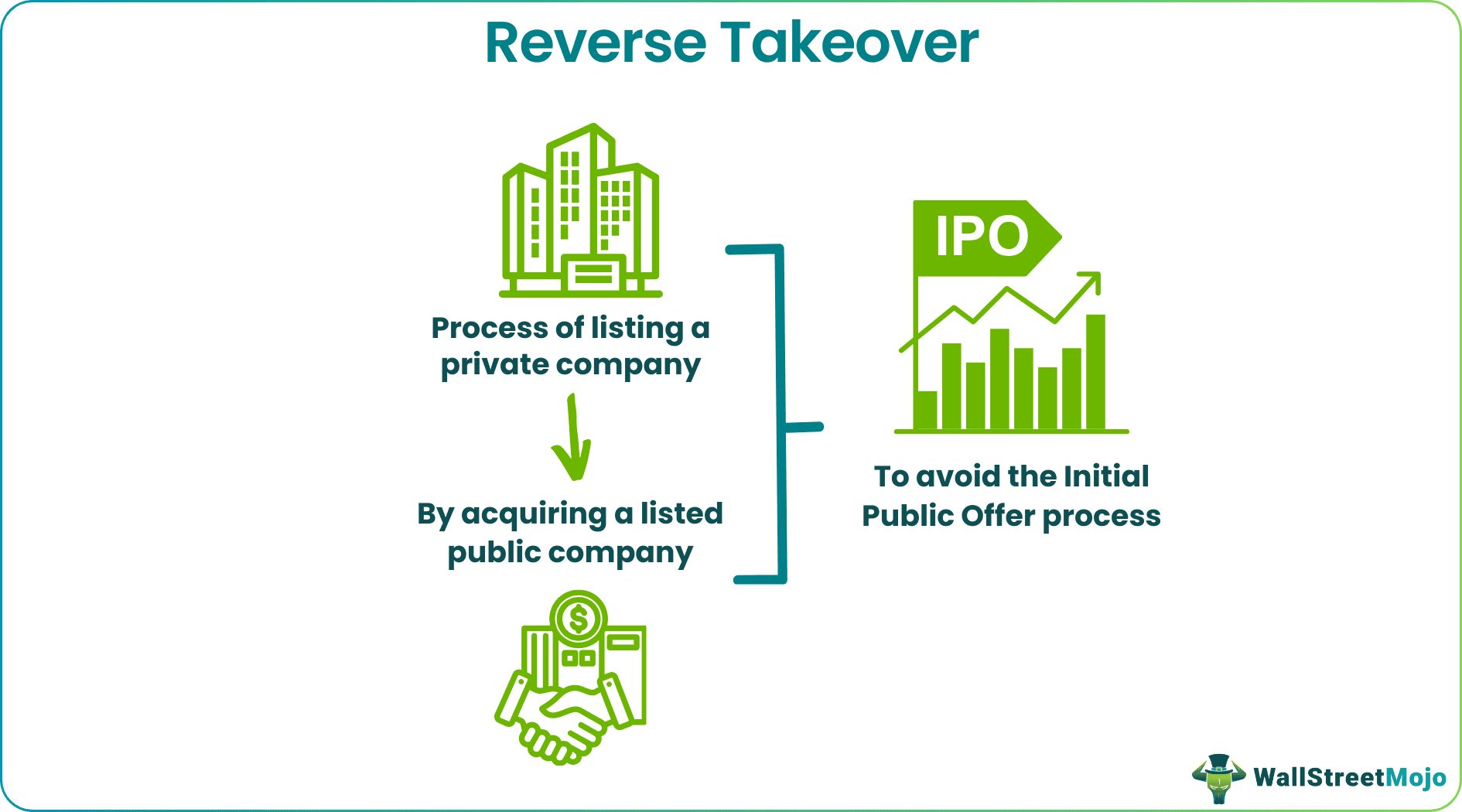

At its core, a reverse takeover is a transaction that allows a private company to trade on a public stock exchange without the rigors of an IPO. To execute this, the private company identifies a “shell company”—an existing publicly traded firm that often has little to no active business operations or assets. This shell company provides the necessary legal vehicle to achieve public status.

Structuring the Acquisition

The process begins with the private company acquiring a majority stake in the public shell company. Through a reverse triangular merger or a direct share swap, the shareholders of the private company exchange their shares for a majority of the shares in the public company. Once the transaction is finalized, the former shareholders of the private company hold the controlling interest in the combined entity.

Crucially, the board of directors and management team of the private company typically replace the shell company’s existing leadership. The assets and business operations of the private company are then integrated into the public entity, and the shell company’s original business—if any—is either liquidated or sidelined. The end result is a functioning business that is now publicly traded, governed by the same regulatory standards as any other listed corporation.

The Role of the Shell Company

The “shell” is not merely a placeholder; it is a tactical asset. These entities, sometimes known as Special Purpose Acquisition Companies (SPACs) or simply “clean” public shells, are specifically sought out for their existing listing status. By utilizing a company that is already compliant with the listing requirements of an exchange, the private firm avoids the exhaustive SEC registration process, which can take eighteen months or longer. Instead, they can often achieve public status in a fraction of that time, provided the transaction meets the exchange’s “back-door listing” requirements.

Strategic Motivations and Benefits

Why would a company opt for a reverse takeover instead of an IPO? The primary drivers are speed, cost-effectiveness, and market access. In volatile market conditions where the window for an IPO might close suddenly, an RTO offers a degree of certainty that the traditional route lacks.

Speed to Market and Regulatory Efficiency

The IPO process is an endurance test. It involves months of preparation, roadshows to attract institutional investors, and a highly regimented review by regulatory bodies like the Securities and Exchange Commission (SEC). For a company that needs to raise capital quickly to fund expansion, research, or debt restructuring, this timeline is often prohibitive. A reverse takeover truncates this period significantly, allowing management to focus on business operations rather than the administrative burden of an IPO filing.

Cost Considerations

An IPO is an expensive undertaking. Underwriters often charge high fees—frequently reaching 7% or more of the capital raised—on top of significant legal, accounting, and printing costs. A reverse takeover, while still involving legal and advisory fees, generally avoids the heavy underwriting commissions associated with primary share offerings. This makes it a compelling option for smaller or mid-market companies that might find the high fixed costs of an IPO to be a barrier to entry.

Access to Capital and Liquidity

By becoming a public company, the firm gains a currency—its stock—which can be used for future acquisitions, employee stock option plans (ESOPs), and as collateral for debt financing. Furthermore, being public provides an “exit strategy” for early-stage investors and venture capitalists who require liquidity to provide returns to their limited partners. The secondary market trading of shares offers the transparency and price discovery that private companies simply cannot provide.

Risks and Regulatory Scrutiny

Despite the efficiency of the reverse takeover, the path is fraught with reputational risks and stringent regulatory hurdles. Because RTOs were historically associated with “pump and dump” schemes and low-quality companies, regulators and stock exchanges have significantly tightened their oversight.

The Stigma of Reverse Takeovers

Historically, many reverse takeovers involved companies that could not meet the rigorous financial reporting or disclosure standards required by a traditional IPO. Consequently, the term “reverse merger” often carried a negative connotation in the eyes of institutional investors and analysts. Even today, a company that chooses the RTO route may face a “liquidity discount,” where its stock trades at a lower valuation than its IPO-born peers due to investor skepticism regarding the lack of a formal vetting process by investment banks.

Enhanced Disclosure Requirements

In response to historical abuses, exchanges have implemented stricter rules. Today, when a company engages in an RTO, the regulatory body often requires the company to file a “Super 8-K” or a comprehensive information circular that provides the same level of disclosure—audited financial statements, operational history, risk factors, and management discussions—that would have been required in an IPO registration statement. This effectively narrows the regulatory advantage of an RTO; while it may be faster, the disclosure burden remains high.

The Challenge of Investor Relations

Without the backing of a large investment bank acting as an underwriter, a company undergoing an RTO does not have the benefit of an established institutional “sales force” to pitch the stock to investors. The company must shoulder the burden of building investor interest from scratch. It is not uncommon for firms that go public via RTO to find themselves with a lack of analyst coverage and thin trading volumes, which can lead to volatility and difficulty in raising subsequent rounds of capital. Success, therefore, relies heavily on the quality of the management team’s communication and their ability to demonstrate long-term value to the public markets.

Evaluating the Suitability of an RTO

Not every company is a candidate for a reverse takeover. It is a tool best suited for firms with a solid operational foundation, transparent financials, and a clear, sustainable business model. For firms that lack these qualities, an RTO can quickly turn into a liability, leading to delisting or legal scrutiny.

When is an RTO the Right Choice?

An RTO is most effective for companies that have reached a stage where public currency is essential for growth, but where the company is not yet ready to endure the exhaustive pressures of a traditional roadshow. If a company already has a strong balance sheet and audited financials, it is much better positioned to successfully navigate the scrutiny that follows an RTO.

Final Considerations for Stakeholders

Before proceeding with an RTO, management must perform a deep audit of the shell company to ensure there are no “hidden” liabilities. It is not enough to find a clean shell; one must ensure that the shell company is free of legal baggage or tax issues that could inheritively become the problem of the new entity. Professional advisory services—including legal counsel with expertise in securities law and auditors familiar with public company reporting—are non-negotiable.

Ultimately, a reverse takeover is a legitimate and powerful financial instrument, but it is not a shortcut to credibility. The market is discerning; it will eventually value a company based on its revenue, growth prospects, and governance, regardless of how it arrived on the public exchange. For the well-prepared organization, an RTO serves as a catalyst, providing the necessary infrastructure to scale operations, attract institutional talent, and compete on the global stage.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.