In the intricate world of finance, where every decision carries an inherent degree of risk and potential reward, a guiding principle is essential for rational investment choices. This principle is encapsulated in a fundamental concept known as the Required Rate of Return (RRR). Far from being an abstract academic construct, the RRR is a practical benchmark that underpins nearly every sound financial decision, from an individual’s retirement planning to a multinational corporation’s capital expenditure projects. It represents the minimum acceptable return an investor or company expects to receive for undertaking an investment, considering its specific risk profile and the prevailing market conditions.

At its core, the RRR serves as a filter. It helps investors, whether they are savvy institutional funds or everyday individuals, distinguish between viable opportunities and those that fall short of their financial objectives. Without a clearly defined RRR, investment decisions can become arbitrary, leading to suboptimal outcomes and potential capital loss. It’s the gatekeeper, ensuring that the compensation for taking on risk is deemed adequate.

The significance of the RRR extends across the broad spectrum of financial activities covered by our platform: “Money” (personal finance, investing, business finance), “Tech” (software, AI tools, digital security relevant to financial operations), and “Brand” (evaluating brand-building investments). Understanding and correctly applying the RRR is paramount for anyone looking to grow wealth, evaluate business ventures, or strategize for long-term financial health in an increasingly complex and technology-driven landscape. It’s not just about what you hope to earn, but what you must earn to justify the investment.

The Foundation of Smart Investment Decisions

Every investment, by its very nature, involves foregoing present consumption or alternative opportunities in the hope of greater future value. This trade-off necessitates a clear standard against which potential returns can be measured. The Required Rate of Return provides this crucial standard, acting as the bedrock for all rational investment decision-making.

Why RRR Matters for Individuals and Businesses

For individuals, the RRR is often implicitly used, even if not formally calculated. When you decide to invest in a stock, a mutual fund, or even a savings account, you’re making a judgment call about whether the potential return is sufficient given the risk involved and what you could earn elsewhere. For instance, a young professional saving for retirement might require a higher rate of return from their investments to reach their financial goals within a specific timeframe, especially if they are comfortable with higher risk. Similarly, someone investing in real estate might set an RRR that factors in rental income, potential property appreciation, and the costs associated with ownership, comparing it against other investment avenues.

For businesses, the RRR is a critical component of capital budgeting. Companies constantly evaluate projects—be it developing a new software product, expanding into a new market, upgrading manufacturing facilities, or launching a massive marketing campaign to build brand equity. Each of these initiatives requires capital, and each carries a certain level of risk. The RRR, often referred to as the hurdle rate in a corporate context, ensures that only projects expected to generate returns exceeding this minimum threshold are approved. This rigorous selection process is vital for maximizing shareholder wealth and ensuring the long-term viability of the enterprise.

Distinguishing RRR from Expected Return

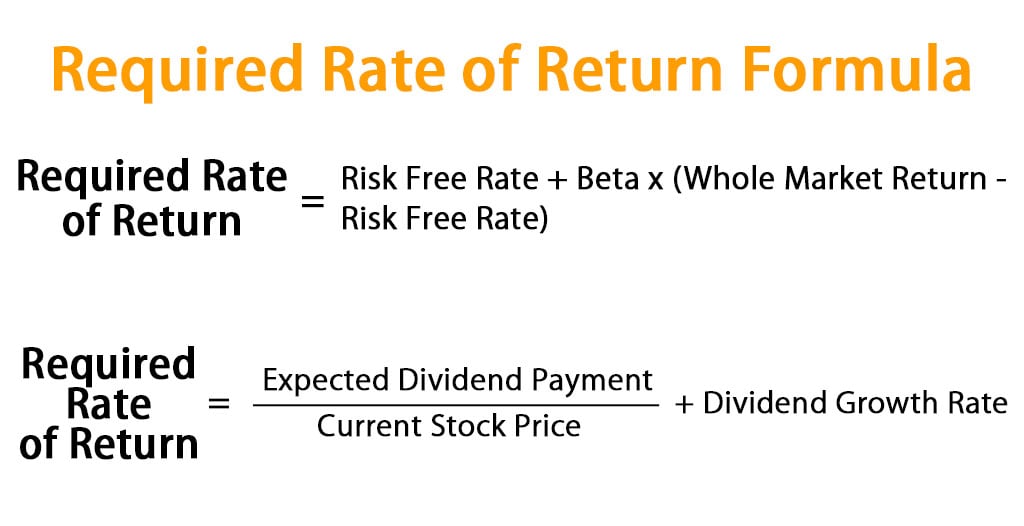

It’s crucial to differentiate the Required Rate of Return from the Expected Rate of Return. The expected return is the anticipated return on an investment based on various projections and historical data. It’s what an investor thinks they will earn. The RRR, conversely, is the minimum return an investor demands to undertake that investment.

The decision-making rule is simple:

- If Expected Rate of Return > Required Rate of Return, the investment is generally considered attractive.

- If Expected Rate of Return < Required Rate of Return, the investment should typically be rejected.

- If Expected Rate of Return = Required Rate of Return, the investment is marginally acceptable, fulfilling the minimum criteria.

This distinction ensures that expectations are not just optimistic guesses but are rigorously compared against a justifiable minimum threshold that accounts for risk and opportunity cost.

Unpacking the Components: What Drives Your RRR?

The Required Rate of Return is not a fixed number; it’s dynamic and influenced by several key factors. These components collectively determine the minimum compensation an investor demands for parting with their capital.

Risk-Free Rate: The Baseline

At the foundation of any RRR calculation is the risk-free rate. This is the theoretical return an investor could earn on an investment with absolutely no risk of default. In practice, the yield on government securities, such as U.S. Treasury Bills or Bonds, is often used as a proxy for the risk-free rate, especially for short to medium-term investments. These instruments are considered to have negligible default risk because governments can typically print more money or raise taxes to meet their obligations.

The risk-free rate serves as the opportunity cost of investing. If you can earn, say, 3% from a risk-free government bond, then any other investment you consider must offer at least 3% (and preferably more) to compensate you for tying up your capital and potentially taking on additional risks.

Risk Premium: Compensating for Uncertainty

While the risk-free rate provides a baseline, most investments involve some level of uncertainty, or risk. The risk premium is the additional return an investor demands above the risk-free rate to compensate for taking on this specific risk. The greater the perceived risk of an investment, the higher the risk premium will be, and consequently, the higher the RRR.

Risk can be categorized in various ways:

- Systematic Risk (Market Risk): This is the risk inherent in the overall market or economy, affecting all investments to some degree. It cannot be diversified away. Factors like interest rate changes, recessions, or geopolitical events contribute to systematic risk.

- Unsystematic Risk (Specific Risk): This risk is specific to an individual company or industry. Examples include management changes, product recalls, or specific industry regulations. Unsystematic risk can often be reduced through diversification by investing in a variety of assets.

- Other Risks: This can include liquidity risk (difficulty selling an asset quickly without a significant price reduction), inflation risk (the risk that inflation erodes the purchasing power of future returns), and political risk, among others.

The equity risk premium, for instance, is the additional return investors demand for holding equities over risk-free assets, reflecting the higher volatility and uncertainty associated with stock ownership. Accurately assessing and quantifying the appropriate risk premium is often the most challenging, yet critical, aspect of determining an RRR.

Inflation and Opportunity Cost: Hidden Factors

Beyond the explicit risks, two often-understated factors significantly influence the RRR:

- Inflation: Inflation erodes the purchasing power of money over time. If your investment only returns a nominal 5% but inflation is running at 3%, your real return is only 2%. A prudent RRR must account for expected inflation to ensure that the actual purchasing power of future returns meets the investor’s objectives. Many investors think in terms of “real” returns, which are returns adjusted for inflation.

- Opportunity Cost: This refers to the value of the next best alternative that was not chosen. When you invest in Project A, you forgo the potential returns from Project B. Your RRR effectively incorporates this opportunity cost, ensuring that the chosen investment is not just marginally profitable but also the most lucrative option available for a given risk level. If there are other attractive investment opportunities with similar risk profiles offering higher returns, your RRR for the current consideration implicitly adjusts upwards.

Together, these components—the risk-free rate, various risk premiums, and consideration of inflation and opportunity cost—form a robust framework for establishing a logically sound Required Rate of Return.

Calculating Your Hurdle: Key Methodologies

While the underlying principles remain constant, the actual calculation of RRR can vary depending on the context, type of investment, and the sophistication of the investor. Several widely accepted methodologies provide structured ways to derive this crucial benchmark.

The Capital Asset Pricing Model (CAPM): A Cornerstone

For many investors, especially those dealing with publicly traded equities, the Capital Asset Pricing Model (CAPM) is a foundational tool for calculating the RRR. CAPM provides a formula that links an asset’s expected return to its systematic risk.

The CAPM formula is:

RRR = Risk-Free Rate + Beta * (Market Risk Premium)

Where:

- Risk-Free Rate: As discussed, the return on a risk-free asset (e.g., U.S. Treasury Bond).

- Beta (β): A measure of an asset’s volatility in relation to the overall market. A beta of 1 means the asset moves in line with the market. A beta greater than 1 indicates higher volatility (more systematic risk), while a beta less than 1 suggests lower volatility.

- Market Risk Premium: The difference between the expected return on the overall market and the risk-free rate. It represents the additional return investors demand for investing in the broad market compared to a risk-free asset.

CAPM is particularly useful for assessing the RRR for individual stocks or portfolios of stocks, guiding investors on whether a stock’s expected return justifies its systematic risk. It’s a cornerstone in financial analysis and portfolio management.

Weighted Average Cost of Capital (WACC): For Corporate Decisions

When a company evaluates large-scale projects, acquisitions, or strategic initiatives, it often uses the Weighted Average Cost of Capital (WACC) as its Required Rate of Return. WACC represents the average rate of return a company expects to pay to all its capital providers (shareholders and creditors). It is the average cost of financing a company’s assets.

The WACC formula incorporates the cost of both equity and debt, weighted by their proportion in the company’s capital structure:

WACC = (E/V) * Re + (D/V) * Rd * (1 – Tc)

Where:

- Re: Cost of Equity (often calculated using CAPM for publicly traded firms).

- Rd: Cost of Debt (interest rate the company pays on its debt).

- E: Market Value of the Company’s Equity.

- D: Market Value of the Company’s Debt.

- V: Total Market Value of the Company’s Financing (E + D).

- Tc: Corporate Tax Rate (the cost of debt is tax-deductible, hence the (1 – Tc) factor).

WACC is a highly effective RRR for corporate capital budgeting because it reflects the blended cost of financing new projects, making it a suitable hurdle rate for investment decisions that aim to maximize overall firm value.

Simplified Approaches for Personal Investing

While CAPM and WACC are robust, they can be complex for the average personal investor. Simpler methods are often employed, especially for less formal investment decisions.

A common simplified approach is to start with a risk-free rate and add a personalized risk premium based on the investor’s risk tolerance and the perceived risk of the asset. For example:

Personal RRR = Risk-Free Rate + Personal Risk Premium + Inflation Premium

- Risk-Free Rate: Current yield on a government bond.

- Personal Risk Premium: A subjective addition based on how much additional return the investor demands for the perceived risk (e.g., 5-10% for a growth stock, 2-4% for a less volatile bond fund).

- Inflation Premium: An estimate of future inflation to protect purchasing power.

Another simplified approach is using a “desired return” based on financial goals, then adjusting for risk. For instance, if an individual needs an average annual return of 7% to reach their retirement goal in 20 years, that 7% effectively becomes their personal RRR for their retirement portfolio. While less mathematically rigorous, these simplified methods help individuals make practical investment choices aligned with their financial objectives and risk comfort levels.

RRR Across the Financial Landscape

The applicability of the Required Rate of Return stretches across diverse financial domains, proving its versatility and indispensable nature in various investment scenarios.

Personal Finance: Saving, Retirement, Real Estate

For individuals, the RRR dictates crucial decisions regarding wealth accumulation and protection. When saving for retirement, individuals often set a target annual return. This target acts as their RRR, guiding their asset allocation strategy. If their RRR is 8%, they will select a portfolio mix of stocks, bonds, and other assets that collectively have an expected return of at least 8%, accepting the associated risk.

In real estate, investors analyze the potential rental income, property appreciation, and associated costs against their RRR. A property with a projected cap rate (Net Operating Income / Property Value) lower than the investor’s RRR might be deemed unattractive. Similarly, for purchasing a house, the RRR can indirectly influence the decision by considering the cost of financing (mortgage interest), property taxes, and potential appreciation versus simply renting and investing the down payment elsewhere. Every major financial commitment, from funding a child’s education to starting a side hustle that requires initial capital, implicitly or explicitly benefits from an RRR calculation.

Business Finance: Capital Budgeting & Project Evaluation

In the corporate world, RRR, often in the form of WACC or a specific hurdle rate, is central to capital budgeting decisions. Companies use it to evaluate potential projects, such as investing in new equipment, developing a new product line, or acquiring another company. A project’s expected Internal Rate of Return (IRR) or Net Present Value (NPV) is compared against the RRR. If a project’s IRR is higher than the RRR, or its NPV is positive when discounted at the RRR, the project is considered value-adding and is typically approved. This rigorous framework ensures that a company’s resources are allocated to initiatives that generate sufficient returns to cover the cost of capital and enhance shareholder value. It prevents the firm from undertaking ventures that are economically unviable or dilutive to existing equity.

Venture Capital and Startup Investments

The world of venture capital (VC) and startup investments presents a unique application of RRR. Early-stage companies are inherently risky; many fail. Consequently, venture capitalists demand extremely high Required Rates of Return—often 20% to 50% or even higher for seed-stage investments. This high RRR compensates for the significant risk of failure and the illiquidity of startup investments. VCs understand that out of ten investments, only one or two might deliver the outsized returns needed to cover the losses from the others and still meet their overall portfolio RRR. The investment thesis for a tech startup, for instance, hinges on its potential to generate explosive growth and market disruption, justifying these exceptionally high RRR expectations. These demanding RRR targets drive the need for innovative technologies and scalable business models that can deliver exponential returns.

Leveraging RRR with Technology and Branding Strategies

In today’s interconnected and data-rich environment, the effective application of the Required Rate of Return is profoundly enhanced by technology and strategically integrated with brand development efforts. The synergy between Money, Tech, and Brand creates powerful new avenues for financial optimization.

Tech’s Role: AI, Software, and Data Analytics in RRR Calculation

Technology has revolutionized how financial professionals and even individual investors approach RRR.

- Financial Modeling Software: Advanced software like Microsoft Excel, specialized financial modeling platforms (e.g., Bloomberg Terminal, Capital IQ), and enterprise resource planning (ERP) systems allow for sophisticated RRR calculations. They can handle complex WACC models, run sensitivity analyses on CAPM inputs (like beta), and integrate various market data sources to derive more precise risk premiums.

- AI and Machine Learning for Risk Analysis: AI tools are increasingly being deployed to analyze vast datasets, identify intricate risk patterns, and predict market volatilities with greater accuracy. This directly impacts the “risk premium” component of RRR. AI algorithms can process news feeds, social media sentiment, economic indicators, and historical stock performance to generate more dynamic and context-aware beta values or risk assessments for specific assets, leading to more refined RRR figures.

- Algorithmic Trading Platforms: For active investors, these platforms can incorporate RRR thresholds into their trading strategies, automatically executing trades only when expected returns surpass the predefined RRR for a given level of risk, enhancing efficiency and discipline.

- Digital Security and Data Integrity: As RRR calculations become more complex and rely on sensitive financial data, the importance of robust digital security cannot be overstated. Secure financial software, encrypted data storage, and protected networks ensure the integrity of the inputs and outputs of RRR models, preventing malicious manipulation or data breaches that could undermine investment decisions.

Brand’s Impact: Evaluating Investments in Brand Equity

While often perceived as intangible, brand equity has a profound financial impact. Brand strength can reduce a company’s cost of capital (lower Rd and potentially Re due to greater investor confidence), increase revenue stability, and enhance pricing power. RRR plays a critical role in evaluating investments in brand-building initiatives.

For example, a company planning a multi-million-dollar marketing campaign to boost brand recognition might use RRR to evaluate the project’s viability. The expected returns from this campaign could include increased sales volume, higher profit margins due to premium pricing, or a stronger market position. By projecting these financial benefits and discounting them back to a present value using the company’s RRR (WACC), management can determine if the investment in brand building is financially justified.

- Case Studies: Consider a tech startup investing heavily in establishing a strong brand identity from the outset. This isn’t merely about aesthetics; it’s a strategic investment aimed at fostering trust, attracting talent, and commanding customer loyalty. The RRR applied to this “brand investment” would need to account for the long-term benefits of customer retention, reduced marketing spend in the future (due to organic growth and word-of-mouth), and a potentially higher valuation in subsequent funding rounds. A strong brand can translate into a lower perceived risk for investors, potentially even influencing a lower future RRR for the company’s cost of equity.

Optimizing Productivity and Security Through RRR Application

The deliberate application of RRR frameworks enhances financial productivity by streamlining decision-making. Instead of relying on gut feelings, individuals and businesses can make data-driven choices, saving time and resources. For example, using an RRR to screen potential investments automatically filters out suboptimal options, allowing focus on higher-potential opportunities. This productivity gain extends to strategic planning, where clearer benchmarks lead to more effective resource allocation.

Furthermore, integrating RRR with robust digital security measures ensures that these critical financial calculations are protected. Financial models containing RRR inputs and outputs are valuable intellectual property. Secure cloud platforms, multi-factor authentication, and blockchain-based solutions for data verification can safeguard the integrity of these financial tools, fostering trust in the investment process and protecting against fraud or errors. In an age where financial data is constantly under threat, ensuring the security of RRR calculations is not just about protection, but about maintaining the credibility and effectiveness of financial decision-making itself.

In conclusion, the Required Rate of Return is far more than a theoretical finance concept; it is an indispensable, dynamic, and adaptable tool for navigating the complexities of investment decisions. From personal savings to corporate strategy, and increasingly amplified by technological advancements and integrated into brand development, RRR provides the essential compass for achieving financial goals. By demanding a return commensurate with risk and opportunity, investors and businesses can make informed choices that build wealth, foster innovation, and secure a prosperous financial future.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.