In the evolving landscape of modern business finance and personal wealth management, the term “per diem” has shifted from a niche HR designation to a critical strategy for both employers and workers. Derived from the Latin phrase meaning “by the day,” a per diem employee is an individual hired on an as-needed basis rather than on a fixed, permanent schedule. While the concept sounds simple, the financial implications—ranging from corporate tax savings to personal income optimization—are profound.

For the business owner, per diem staffing is a tool for managing overhead and maintaining a lean balance sheet. For the professional, it represents a high-yield “side hustle” or a primary income strategy that offers premium daily rates in exchange for the absence of traditional benefits. Understanding the financial mechanics of this arrangement is essential for anyone looking to navigate the contemporary economy with fiscal precision.

Understanding the Financial Mechanics of Per Diem Work

At its core, the per diem model is a “pay-as-you-go” approach to labor. Unlike salaried employees who represent a fixed cost on a company’s monthly income statement, per diem workers are a variable expense. This distinction is vital for business finance, as it allows organizations to scale their workforce in direct response to revenue fluctuations or seasonal demand.

Daily Rates vs. Traditional Salary Structures

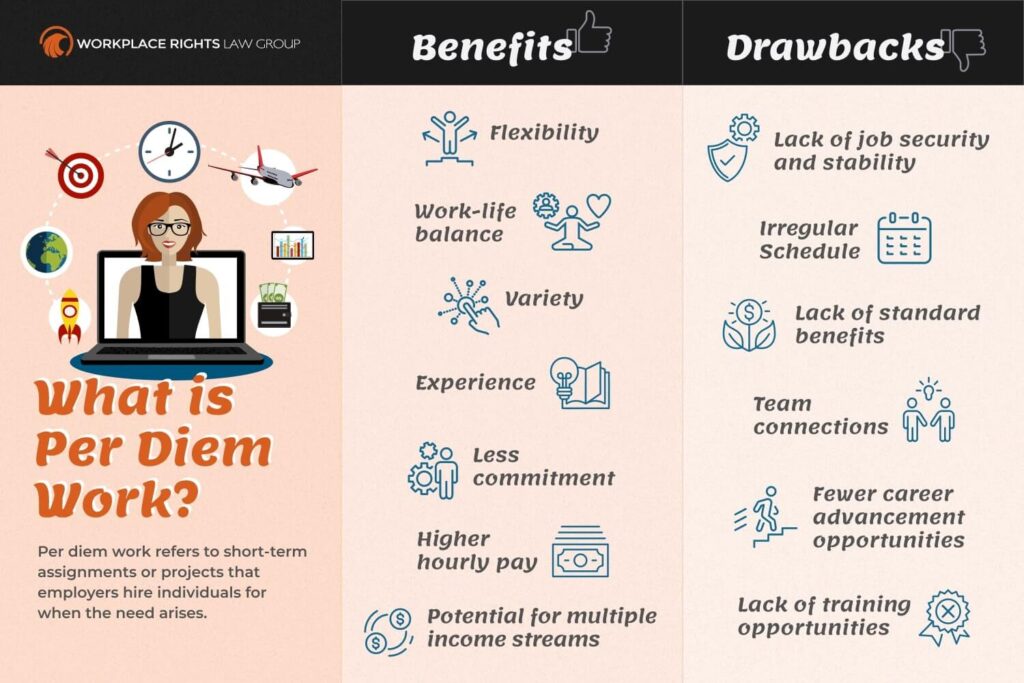

One of the most immediate differences in a per diem arrangement is the pay structure. Because per diem employees do not typically receive a standard benefits package—such as health insurance, paid time off (PTO), or 401(k) matching—their base pay is often significantly higher than that of their full-time counterparts.

From a financial perspective, this is a calculated trade-off. A business might pay a salaried nurse $40 per hour but find that, once benefits, payroll taxes, and insurance are factored in, the “total cost of employment” is closer to $60 per hour. By hiring a per diem nurse at a flat $55 per hour, the company actually reduces its total expenditure while providing the worker with a higher take-home daily rate. This creates a unique opportunity for professionals to maximize their immediate cash flow.

The Impact on Corporate Overhead and Fixed Costs

For a CFO or business manager, the primary allure of per diem staffing is the reduction of “burdened labor costs.” Fixed costs are the enemies of agility in business finance. When a company carries a large permanent staff during a slow quarter, the “burn rate” can quickly deplete cash reserves.

Per diem employees allow a firm to convert fixed costs into variable costs. If there is no work, there is no pay. This protects the company’s profit margins during downturns. Furthermore, the administrative costs associated with maintaining long-term employee files, performing annual reviews, and managing complex benefits programs are significantly reduced, streamlining the financial operations of the HR department.

The Financial Landscape for the Per Diem Professional

From the perspective of personal finance and income generation, working per diem can be a powerful wealth-building tool. Whether used as a primary career path or a secondary side hustle, it requires a disciplined approach to money management to account for the lack of a corporate safety net.

Maximizing Income Through Strategic Flexibility

The greatest financial advantage for the per diem worker is the ability to command a premium for their availability. In industries like healthcare, education, and specialized consulting, per diem rates can be 20% to 50% higher than standard hourly wages.

For those looking to accelerate their journey toward financial independence, per diem work offers a way to “stack” income. A professional might hold a stable, part-time job for benefits while taking on per diem shifts at a higher rate to fund investments, pay off debt, or build an emergency fund. This flexibility allows for an “income-on-demand” model that is far more lucrative than traditional overtime, which is often capped or discouraged by budget-conscious employers.

Navigating Tax Responsibilities and Deductions

The tax implications of per diem work depend heavily on how the individual is classified—either as a W-2 employee or a 1099 independent contractor. Most per diem workers in institutional settings (like hospitals) are W-2 employees, meaning the employer still withholds taxes. However, the lack of traditional deductions for benefits means the worker’s taxable income may appear higher.

If the per diem worker is classified as an independent contractor, they enter the realm of small business finance. This requires diligent tracking of expenses, quarterly estimated tax payments, and an understanding of Self-Employment Tax (SE tax). While this adds complexity, it also opens the door to significant tax deductions, such as home office expenses, travel costs, and equipment, which can lower the overall tax burden compared to a standard salaried worker.

Strategic Business Finance: When to Hire Per Diem

From a management standpoint, the decision to utilize per diem staff should be driven by data and financial forecasting. It is not merely an HR choice; it is a strategic move to optimize the company’s “Return on Human Capital.”

Managing Variable Labor Costs and Peak Demand

Many industries experience predictable cycles. A retail business may face a surge during the holidays, while a healthcare facility may see a spike during flu season. Hiring full-time staff to cover these peaks results in “underutilization” during the rest of the year—a major financial drain.

By integrating per diem workers into the labor mix, a business can maintain a core team of essential staff and use per diem professionals to “buffer” the peaks. This ensures that the company is never overstaffed during lean periods, preserving the bottom line. It also prevents the “overtime trap,” where existing staff are paid time-and-a-half or double-time, which can be far more expensive than hiring a per diem worker at a slightly higher flat rate.

Risk Mitigation and Financial Compliance

There is also a risk-management component to per diem hiring. Long-term employment comes with various financial liabilities, including potential unemployment insurance claims and severance packages. Per diem workers, by the nature of their “at-will” and “as-needed” status, present a lower long-term liability for the company.

However, businesses must be careful to comply with labor laws regarding classification. If a per diem worker begins to work a consistent 40-hour week for an extended period, they may legally qualify for benefits. Financial controllers must monitor these hours closely to ensure the company doesn’t inadvertently trigger “Benefit Parity” requirements, which could lead to unexpected retroactive costs and legal fees.

Evaluating the Pros and Cons: A Wealth-Building Perspective

For the individual, the per diem lifestyle is a high-risk, high-reward financial strategy. Success requires a transition from a “consumer” mindset to a “business” mindset regarding one’s own labor.

Retirement Planning for Non-Traditional Workers

The most significant financial hurdle for a per diem worker is the lack of a company-sponsored retirement plan. Without a 401(k) match, the worker is essentially leaving “free money” on the table unless they take proactive steps.

To build long-term wealth, the per diem professional must utilize specialized financial tools:

- Solo 401(k) or SEP IRA: If classified as a contractor, these allow for much higher contribution limits than a standard IRA.

- Health Savings Accounts (HSA): Since per diem workers often purchase their own high-deductible health plans, an HSA offers a triple-tax advantage for investing.

- Automated Investing: Because per diem income can be irregular, setting a percentage-based (rather than dollar-based) investment goal is crucial for maintaining a growth trajectory.

The True Cost of Missing Benefits

When calculating whether a per diem role is financially viable, one must look beyond the hourly rate. A $60/hour per diem rate may seem superior to a $45/hour salaried rate, but the “hidden” costs must be subtracted:

- Health Insurance: This can cost $500–$1,500 per month out of pocket.

- Paid Time Off: A salaried worker gets 3–4 weeks of paid rest; a per diem worker loses income every day they don’t work.

- Disability Insurance: Crucial for those without corporate coverage to protect their primary “wealth-generating asset”—their ability to work.

Ultimately, a per diem employee is a master of their own financial destiny. In a world where “job security” is increasingly an illusion, the ability to work for multiple employers on a flexible basis provides a different kind of security: the security of diversified income streams. Whether viewed as a corporate strategy for maintaining liquidity or a personal strategy for maximizing earnings, the per diem model remains one of the most effective tools in the modern financial toolkit.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.