For many households, the monthly electric bill is a source of recurring anxiety. It is one of the most volatile components of a personal budget, fluctuating with the seasons, the economy, and even daily habits. When a bill arrives that is significantly higher than the previous month, the immediate question is: “Is this normal?”

Understanding what constitutes a “normal” electric bill is not just about comparing numbers with your neighbors. It is an essential exercise in financial literacy. By decoding the factors that drive these costs, you can transition from reactive payment to proactive financial management. In the context of personal finance, your utility bill represents a controllable overhead that, when optimized, can free up significant capital for investing or debt reduction.

Decoding the Average: What Does “Normal” Actually Look Like?

To determine if your spending is within a healthy range, you must first establish a baseline. According to data from the U.S. Energy Information Administration (EIA), the average monthly residential electric bill in the United States typically hovers between $115 and $150. However, “average” is a mathematical middle ground that rarely reflects the reality of every individual.

Regional Disparities and the Cost of Living

Geography is perhaps the most significant determinant of your electric bill. Utility rates are governed by local regulations, the availability of energy resources, and the state’s infrastructure. For instance, residents in states like Hawaii or Connecticut often face bills well above $200 due to high generation costs and imported fuels. Conversely, states with abundant hydroelectric power or deregulated markets, like Washington or parts of Texas, may see averages below $100. When assessing your bill, you must compare your costs against regional benchmarks rather than national ones to get an accurate financial picture.

The Impact of Household Size on Consumption

The number of occupants in a home is a direct multiplier of energy usage. A single professional living in a 700-square-foot apartment will have a vastly different “normal” than a family of five in a suburban home. On average, a typical American home uses approximately 886 kWh per month. If you are a solo dweller and your usage exceeds 1,000 kWh, your bill is objectively high regardless of the dollar amount. Understanding your consumption in kilowatt-hours (kWh) rather than just currency allows for a more precise analysis of household efficiency.

Seasonal Fluctuations: Heating vs. Cooling

In personal finance, “normal” often refers to a moving target. For those living in the Sun Belt, a $300 bill in July might be standard due to air conditioning demands, while a $80 bill in November is expected. In the North, the reverse may be true if the home uses electric heating. A healthy financial plan accounts for these peaks and valleys. If your bill is consistent year-round but your climate is not, it may indicate an inefficient HVAC system or an unusual billing structure from your provider.

Key Factors Influencing Your Utility Budget

If your bill falls outside the normal range for your area and family size, the cause is usually found within the home’s operational efficiency. Identifying these factors is the first step in reclaiming control over your cash flow.

Appliance Efficiency and Phantom Loads

Not all appliances are created equal. Older refrigerators, dryers, and water heaters are notorious “energy hogs” that can inflate a bill by 20% or more compared to modern Energy Star-certified versions. Furthermore, “phantom loads”—the energy consumed by electronics while they are plugged in but turned off—can account for as much as 10% of a monthly bill. From a budgeting perspective, these are hidden leakages. Identifying and mitigating them is akin to finding and canceling a forgotten subscription service.

Fixed Fees vs. Variable Usage Costs

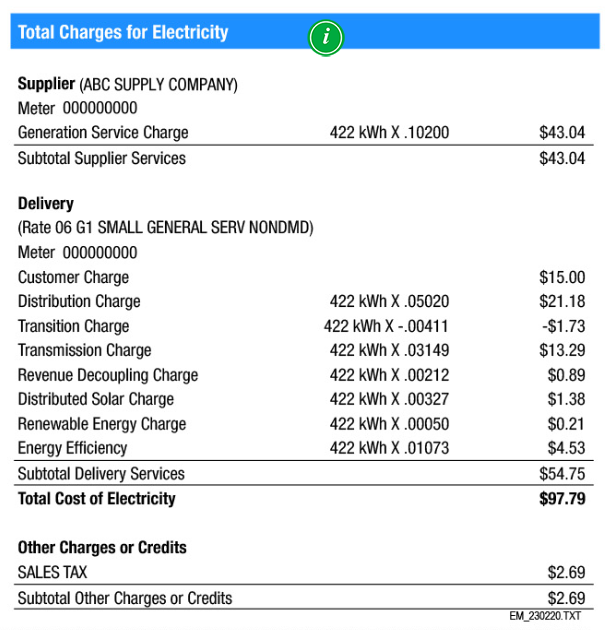

A common point of confusion for consumers is the breakdown of the bill itself. Most electric bills consist of two parts: the supply/generation charge (variable) and the delivery/distribution charge (often fixed or tiered). In some regions, delivery fees can make up nearly half of the total bill. This means that even if you cut your energy usage by 50%, your bill will not drop by 50%. Understanding this ratio helps you set realistic expectations for how much you can actually save through behavioral changes.

The Role of Housing Structure and Insulation

The “envelope” of your home—the walls, windows, and roof—dictates how much energy is required to maintain a comfortable temperature. A home with poor insulation or single-pane windows will require the HVAC system to work overtime, leading to bills that stay stubbornly high. For many homeowners, the “normal” bill is high simply because the house is “leaking” money in the form of conditioned air. Improving insulation is an upfront expense that serves as a long-term investment in reduced monthly overhead.

Strategic Financial Management of Utility Expenses

Treating your electric bill as a static expense is a missed opportunity for financial optimization. By applying business-level scrutiny to your home energy costs, you can improve your monthly margins.

Implementing an Energy Audit for Long-Term Savings

Many utility companies offer free or subsidized energy audits. A professional auditor uses infrared cameras and blower door tests to find exactly where your money is being wasted. For a personal finance enthusiast, an energy audit is the equivalent of a deep-dive audit of an investment portfolio. It identifies underperforming assets (appliances) and provides a roadmap for high-impact improvements.

Budget Billing and Levelized Payment Plans

One of the greatest challenges in personal budgeting is the volatility of utility costs. Many providers offer “Budget Billing” or “Levelized Payment” plans. These programs take your total annual energy cost and divide it into 12 equal payments. While this doesn’t reduce the total amount paid over a year, it eliminates “bill shock” during extreme weather months. From a cash-flow management perspective, this predictability is invaluable, allowing you to allocate funds to savings or investments with greater precision.

Tax Credits and Rebates for High-Efficiency Upgrades

When you decide to upgrade your home’s efficiency, the tax code can be your best friend. Legislation like the Inflation Reduction Act in the U.S. provides substantial tax credits for heat pumps, high-efficiency water heaters, and improved insulation. These incentives effectively lower the “break-even” point of your investment. When calculating the ROI (Return on Investment) of a home upgrade, always factor in these federal and local rebates, as they can turn a ten-year payback period into a five-year one.

Investing in Energy Independence

For those looking to move beyond merely “normal” bills, the ultimate financial goal is energy independence. This involves shifting from being a consumer to being a producer.

The ROI of Solar Power and Home Batteries

Solar panels represent one of the most significant “side hustles” for a homeowner. By installing a photovoltaic system, you are essentially pre-paying for 20 to 25 years of electricity at a fixed rate. While the upfront cost is high, the internal rate of return (IRR) on a solar installation often outperforms traditional market investments, especially in high-cost energy states. When coupled with a battery backup system, homeowners can avoid “Time of Use” (TOU) pricing, where utilities charge more during peak evening hours, further insulating their budget from price hikes.

Smart Home Technology as a Financial Tool

Technology has transitioned from a luxury to a financial necessity in energy management. Smart thermostats, for example, use machine learning to optimize heating and cooling based on your habits and the current price of electricity. Smart plugs and energy monitors provide real-time data on consumption. In the world of finance, “what gets measured gets managed.” These tools provide the granular data necessary to make informed decisions about where to cut back and where to invest.

Conclusion: Reframing the Electric Bill

A “normal” electric bill is ultimately a subjective figure, but it should never be a mystery. By understanding the regional, structural, and behavioral factors that drive your costs, you can move from a state of passive payment to active financial management.

Managing your utility bill is a microcosm of broader personal finance: it requires an understanding of fixed vs. variable costs, an eye for ROI on capital improvements, and the discipline to monitor and adjust habits over time. Whether through simple behavioral changes, utilizing budget billing to smooth out cash flow, or making strategic investments in solar and insulation, you have the power to define your own “normal.” In doing so, you turn a mundane monthly expense into a streamlined component of your journey toward financial freedom.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.