The journey to homeownership is often a complex and multifaceted one, with numerous players involved in facilitating the transaction. Among these key individuals, the mortgage originator stands out as a pivotal figure, acting as the primary point of contact for borrowers seeking to finance their dream homes. Understanding the role and responsibilities of a mortgage originator is crucial for anyone navigating the mortgage process, as their expertise, guidance, and actions can significantly impact the outcome of a loan application.

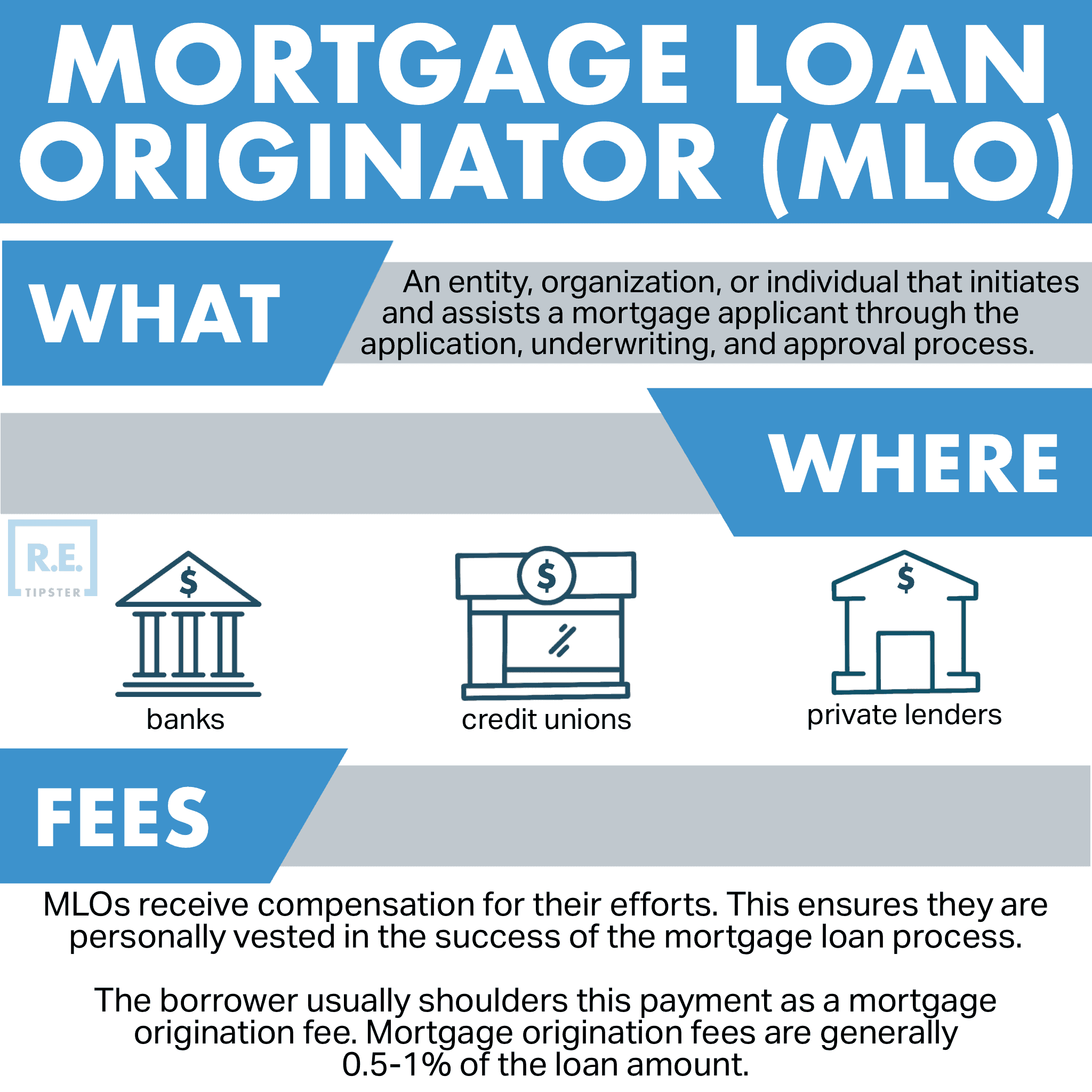

Mortgage originators are essentially the gateway to obtaining a home loan. They are licensed professionals who work with borrowers to understand their financial situations, identify suitable loan products, and guide them through the entire application and underwriting process. While the term “loan officer” is often used interchangeably, “mortgage originator” specifically refers to the individual who initiates the loan process on behalf of a borrower. They are the face of the lending institution, bridging the gap between the applicant and the lender’s internal processes. Their role is not merely administrative; it involves a deep understanding of financial products, regulatory compliance, and interpersonal skills to build trust and ensure a smooth experience for the borrower.

The Multifaceted Role of a Mortgage Originator

The responsibilities of a mortgage originator extend far beyond simply taking an application. They are tasked with a comprehensive set of duties that require a blend of financial acumen, salesmanship, and customer service.

Initial Consultation and Needs Assessment

The process begins with an initial consultation where the mortgage originator sits down with prospective borrowers, either in person, over the phone, or via video conference. This is a critical stage where the originator aims to thoroughly understand the borrower’s financial goals, their current financial standing, and their specific needs related to purchasing a home. This involves asking detailed questions about income, assets, debts, credit history, and the type of property they intend to purchase. They will inquire about the down payment amount, desired loan term, and any specific preferences or concerns the borrower may have. This thorough assessment allows the originator to identify the most appropriate loan programs and lenders that align with the borrower’s circumstances and objectives.

Explaining Loan Products and Options

Once the borrower’s needs are understood, the mortgage originator’s role shifts to educating them about the various mortgage products available. This can be a daunting task for many, given the array of loan types, interest rate structures, and repayment terms. The originator must clearly explain the differences between fixed-rate mortgages, adjustable-rate mortgages (ARMs), FHA loans, VA loans, USDA loans, conventional loans, and jumbo loans. They will detail the pros and cons of each, including interest rates, monthly payments, closing costs, and any associated fees. Furthermore, they will explain the implications of different loan terms, such as 15-year versus 30-year mortgages, and how these choices impact the overall cost of borrowing. Transparency and clarity are paramount here, ensuring the borrower makes informed decisions without feeling overwhelmed.

Guiding the Application Process

The mortgage application itself is a complex document requiring precise and accurate information. The mortgage originator is instrumental in guiding the borrower through each section of the application. They will assist in collecting necessary documentation, which typically includes proof of income (pay stubs, tax returns), bank statements, identification, and information about existing debts. The originator will review submitted documents for completeness and accuracy, identifying any potential issues or discrepancies that could hinder the loan approval process. They act as a buffer, ensuring that all required paperwork is submitted in the correct format and by the specified deadlines. This meticulous attention to detail is vital for a smooth progression towards loan approval.

Underwriting and Loan Approval

While the mortgage originator does not personally underwrite the loan (that is the role of an underwriter at the lending institution), they play a crucial role in preparing the loan file for underwriting. They will often pre-qualify or pre-approve borrowers based on initial information, providing an estimate of how much they might be able to borrow. Once the formal application is submitted, the originator will work closely with the underwriting department, responding to any requests for additional documentation or clarification. They act as the liaison between the borrower and the underwriter, translating the underwriter’s requirements and conveying any necessary information back to the borrower. Their ability to effectively communicate and advocate for the borrower can be critical in overcoming underwriting hurdles and securing loan approval.

Closing the Loan

The final stage of the mortgage process involves the closing, also known as settlement. The mortgage originator typically ensures that all parties are prepared for this event. They will coordinate with the title company, appraiser, and other relevant parties to ensure that all necessary documents are in order and that all conditions of the loan have been met. They will often attend the closing to answer any last-minute questions and ensure that the borrower understands all the paperwork they are signing. Their presence and guidance at this critical juncture provide reassurance and help to finalize the transaction smoothly.

Types of Mortgage Originators

The mortgage origination landscape is diverse, with professionals operating under various models and affiliations. Understanding these distinctions can help borrowers identify the type of originator best suited to their needs.

Bank Loan Officers

Many mortgage originators work directly for banks and credit unions. These institutions offer a wide range of mortgage products, often catering to existing customers. Bank loan officers typically have access to the bank’s proprietary loan programs and may offer competitive rates. Their advantage lies in the established trust and convenience of dealing with a familiar financial institution. However, their product offerings are limited to what their parent institution provides, which might not always be the most competitive option in the broader market.

Mortgage Brokers

Mortgage brokers, on the other hand, do not lend money directly. Instead, they act as intermediaries, connecting borrowers with various lenders. They have established relationships with multiple wholesale lenders and can shop around on behalf of their clients to find the best loan terms. This allows borrowers to access a wider array of loan products and potentially secure more favorable rates than they might find directly from a single lender. Mortgage brokers are compensated through commissions, either paid by the borrower or the lender, or a combination of both. Their expertise lies in navigating the wholesale lending market and identifying the most suitable lender for each borrower’s unique situation.

Correspondent Lenders

Correspondent lenders originate loans in their own name but then sell them to larger investors or wholesale lenders. They operate with their own underwriting guidelines but often adhere to the requirements of the investors they sell to. This model allows them to offer a degree of flexibility while still benefiting from the scale of larger institutions. They can be a good option for borrowers who may not fit the strict criteria of a major bank but are still looking for competitive rates.

Direct Lenders

Direct lenders originate and service loans themselves. This means they handle the entire process from origination to loan servicing (collecting payments and managing the loan post-closing). This model can offer a streamlined experience for borrowers, as there is a single point of contact throughout the loan lifecycle. Many large mortgage companies operate as direct lenders, offering a variety of loan products and often leveraging technology to enhance the borrower experience.

Qualifications and Licensing

To operate as a mortgage originator, professionals must adhere to strict regulatory requirements designed to protect consumers and ensure the integrity of the mortgage lending industry.

National and State Licensing

In the United States, mortgage originators are required to be licensed by both federal and state authorities. The primary federal regulator is the Nationwide Multistate Licensing System & Registry (NMLS). NMLS oversees a nationwide system for licensing and registering mortgage loan originators. This involves passing a comprehensive national test covering mortgage law, ethics, and loan origination practices, as well as meeting specific education and background check requirements. Most states also have their own licensing requirements and exams, which may vary in their specifics. These licensing requirements ensure that originators possess the necessary knowledge and ethical standards to serve consumers responsibly.

Education and Continuing Education

Beyond initial licensing, mortgage originators are mandated to complete ongoing continuing education (CE) courses to stay abreast of evolving regulations, market trends, and best practices in the industry. This commitment to continuous learning is vital in a dynamic financial landscape where laws and products can change rapidly. CE courses ensure that originators maintain their expertise and provide up-to-date advice to borrowers. Topics covered in CE often include new federal and state regulations, ethical considerations, cybersecurity awareness, and advancements in mortgage technology.

Ethical Conduct and Consumer Protection

The role of a mortgage originator carries significant ethical responsibilities. They are entrusted with sensitive financial information and are expected to act in the best interest of the borrower. This includes providing accurate and complete information, avoiding deceptive practices, and ensuring that borrowers understand the terms and implications of their loan agreements. Regulatory bodies and industry ethics codes emphasize transparency, fairness, and the prevention of predatory lending. Consumers are protected by regulations like the Truth in Lending Act (TILA) and the Real Estate Settlement Procedures Act (RESPA), which mandate disclosures and prohibit certain practices. A reputable mortgage originator will prioritize these ethical considerations, building trust and fostering long-term relationships with their clients.

The Impact of Technology on Mortgage Origination

The mortgage industry, like many others, has been profoundly shaped by technological advancements. Technology has not only streamlined processes but also created new opportunities and challenges for mortgage originators.

Digitalization of the Application Process

The traditional paper-heavy mortgage application process has largely given way to digital platforms. Online applications, electronic document submission, and digital signatures have become commonplace. Mortgage originators now utilize sophisticated loan origination software (LOS) that automates many aspects of the application, from data entry to initial document verification. This allows originators to process applications more efficiently, reduce errors, and provide borrowers with real-time updates on their loan status. Digital tools also facilitate secure communication and data sharing between borrowers, originators, and other parties involved in the mortgage process.

Data Analytics and AI in Loan Decisioning

While human expertise remains vital, data analytics and artificial intelligence (AI) are playing an increasing role in mortgage origination. Lenders are using AI-powered algorithms to analyze vast amounts of data, assess risk more accurately, and even assist in underwriting decisions. For originators, these tools can help identify potential borrowers, personalize loan offers, and predict loan performance. AI can also automate fraud detection and identify discrepancies in applicant data. The ability to leverage these technologies allows originators to be more efficient and provide more tailored solutions to borrowers.

Enhanced Communication and Customer Experience

Technology has revolutionized how mortgage originators communicate with their clients. Secure client portals, mobile apps, and video conferencing tools enable seamless interaction and provide borrowers with 24/7 access to loan information. Automated email and text notifications keep borrowers informed about application progress, upcoming deadlines, and required actions. This enhanced communication fosters greater transparency, reduces borrower anxiety, and ultimately contributes to a more positive and efficient customer experience. Mortgage originators who embrace these technological advancements are better positioned to meet the evolving expectations of today’s borrowers.

In conclusion, the mortgage originator is an indispensable professional in the home-buying process. They serve as navigators, educators, and facilitators, guiding individuals through the often-intimidating world of home financing. From understanding individual financial needs to ensuring regulatory compliance and leveraging technological advancements, their role is complex and demanding. By comprehending the duties, qualifications, and evolving landscape of mortgage origination, prospective homeowners can better prepare themselves for a successful and informed journey to homeownership.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.