In the landscape of personal finance and estate planning, few challenges are as daunting as the rising cost of long-term care. As medical advancements extend life expectancy, many individuals find themselves facing the high costs of assisted living or nursing home care, which can easily exceed $100,000 per year in many parts of the United States. Without a strategic financial plan, these expenses can rapidly deplete a lifetime of savings, leaving families with little to pass on to the next generation. This is where the Medicaid Asset Protection Trust (MAPT), commonly referred to as a Medicaid Trust, becomes a vital instrument in a comprehensive financial portfolio.

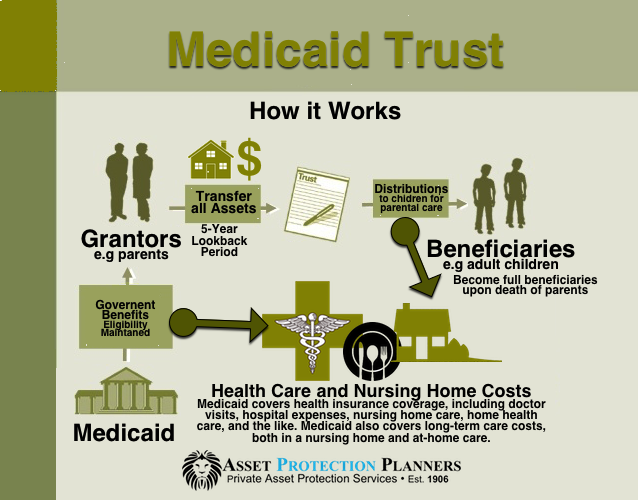

A Medicaid Trust is a specialized financial tool designed to help individuals qualify for Medicaid benefits while shielding their assets from being “spent down” to meet the program’s strict eligibility requirements. By moving assets into an irrevocable trust, the grantor effectively removes those assets from their countable estate, ensuring that their legacy remains intact while still securing the care they need.

Understanding the Financial Mechanics of a Medicaid Trust

To understand how a Medicaid Trust functions within a financial plan, one must first understand the distinction between different types of trusts. Unlike a revocable living trust, which allows the grantor to maintain total control and access to the assets, a Medicaid Trust must be irrevocable. From a financial perspective, this means the grantor gives up ownership of the assets to ensure they are not counted as available resources by the government.

How an Irrevocable Trust Works

In the context of personal finance, an irrevocable trust is a legal entity that “owns” the assets placed within it. Once the grantor transfers property, stocks, or cash into a Medicaid Trust, they no longer have the legal right to take those assets back. This permanent transfer is what allows the assets to be excluded from Medicaid’s asset limit calculations. However, the grantor can still derive some benefit from the trust, such as the right to live in a home held by the trust or the right to receive income generated by the trust’s investments.

The Distinction Between Income and Principal

A critical component of managing a Medicaid Trust is the separation of principal and income. For a trust to be effective in qualifying a person for Medicaid, the principal (the core assets) must be inaccessible to the grantor. However, many trusts are structured so that any interest or dividends generated by the principal can still be paid out to the grantor to help cover living expenses before they enter long-term care. It is important to note, however, that once an individual is in a nursing home, Medicaid may require that this income be applied toward the cost of care. Understanding this distinction is essential for financial modeling and cash flow planning in one’s later years.

Navigating the 5-Year Look-Back Period and Asset Eligibility

One of the most significant hurdles in Medicaid planning is the “Look-Back Period.” This is a timeframe during which Medicaid officials review all financial transfers made by the applicant. If assets were moved into a trust within this window, the applicant may face a penalty period of ineligibility.

The Strategy of Early Financial Planning

In most states, the look-back period is 60 months, or five years. This means that for a Medicaid Trust to be fully effective, it should ideally be established and funded at least five years before the individual anticipates needing long-term care. From a financial planning perspective, this requires a proactive approach. Waiting until a health crisis occurs is often too late to utilize a trust effectively. By planning in one’s 60s or early 70s, an individual can “start the clock” on the five-year window, ensuring that their assets are protected well before the need for professional care arises.

Penalties and Pitfalls of Late Transfers

If a transfer is made within the five-year look-back period, Medicaid calculates a penalty period based on the amount transferred divided by the average monthly cost of nursing home care in that state. For example, if an individual transfers $200,000 into a trust and the average cost of care is $10,000 a month, they would be ineligible for Medicaid for 20 months. This highlights the importance of liquidity; if a trust is funded late, the grantor must have enough “outside” funds to cover the cost of care during the penalty period. This strategic balance of assets is a cornerstone of sophisticated wealth management.

Key Benefits of a Medicaid Trust for Wealth Preservation

The primary motivation for establishing a Medicaid Trust is the preservation of wealth. Without such a trust, an individual must spend their assets down to a very low threshold—often as little as $2,000—before Medicaid will begin to cover the costs of long-term care.

Protecting the Family Home from Estate Recovery

For many families, the primary residence is their most significant financial asset. While Medicaid often considers a home an “exempt” asset during the applicant’s lifetime, the Medicaid Estate Recovery Program (MERP) allows the state to place a lien on the home after the individual’s death to recoup the costs of care paid by the program. By placing the home into a Medicaid Trust, the property is no longer part of the probate estate. This protects the home from state recovery efforts, ensuring that it can be passed down to heirs or sold for the benefit of the family.

Ensuring an Inheritance for Future Generations

Beyond the home, a Medicaid Trust protects liquid investments, such as brokerage accounts and savings. By shielding these assets from the “spend-down” requirement, the grantor ensures that their children or other beneficiaries receive an inheritance. This is particularly important for families who wish to maintain a family business or preserve a legacy of financial stability. The trust acts as a firewall, separating the funds intended for the family from the high costs of the healthcare system.

Strategic Implementation: Setting Up and Managing the Trust

Implementing a Medicaid Trust is not a “set it and forget it” action. It requires careful selection of participants and an understanding of the ongoing financial implications.

Selecting the Right Trustee

Since the grantor cannot have control over the trust, selecting a trustee is a pivotal decision. Often, adult children or a trusted professional advisor are chosen for this role. The trustee is responsible for managing the assets, filing tax returns for the trust, and ensuring that distributions are made according to the trust’s terms. From a financial oversight perspective, the trustee must be someone with the acumen to manage investments prudently while adhering strictly to the legal constraints of the trust to avoid disqualifying the grantor from future benefits.

Tax Implications and Considerations

While the primary goal of a Medicaid Trust is asset protection, the tax implications cannot be ignored. Medicaid Trusts are typically structured as “Grantor Trusts” for income tax purposes. This means that while the assets are removed from the estate for Medicaid purposes, the grantor still reports the trust’s income on their personal tax return. This is often beneficial as it allows the grantor to utilize personal tax exemptions and potentially lower tax rates compared to the compressed tax brackets of a complex trust. Furthermore, if the trust holds a primary residence, the grantor can often retain the Section 121 exclusion on the sale of a principal residence, preserving a significant tax break on capital gains.

The Role of the Trust in a Modern Financial Portfolio

Integrating a Medicaid Trust into a broader financial strategy is about risk management. Just as an investor uses insurance to protect against catastrophic loss, the Medicaid Trust protects against the “catastrophic” cost of long-term care. It complements other tools, such as Long-Term Care Insurance (LTCI). For those who may not qualify for LTCI due to age or health conditions, or for those who find the premiums of LTCI prohibitively expensive, the Medicaid Trust offers an alternative path to financial security.

Ultimately, the decision to move forward with a Medicaid Trust should be based on a thorough analysis of one’s net worth, projected healthcare needs, and desire for legacy preservation. It is a sophisticated move that requires the coordination of financial advisors and legal experts to ensure that all transfers are compliant with both state and federal regulations.

In conclusion, a Medicaid Trust is more than just a legal document; it is a strategic financial fortress. It allows individuals to navigate the complexities of the American healthcare system without sacrificing their hard-earned wealth. By understanding the look-back rules, the necessity of an irrevocable structure, and the benefits of estate recovery protection, individuals can make informed decisions that secure their own care while providing for the financial future of their loved ones. As the costs of care continue to climb, the Medicaid Trust remains one of the most effective tools for maintaining financial autonomy and ensuring that a lifetime of work translates into a lasting family legacy.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.