In the contemporary landscape of personal finance and business economics, the term “living wage” has transitioned from a niche sociological concept to a cornerstone of financial planning and corporate responsibility. At its core, a living wage is the minimum income necessary for a worker to meet their basic needs and participate fully in society without falling into a cycle of debt or relying on external assistance. Unlike the legally mandated minimum wage, which is often a static figure set by government policy, a living wage is dynamic, localized, and deeply rooted in the actual costs of living.

Understanding the nuances of a living wage is essential for anyone looking to master their personal finances, as well as for business owners aiming to build sustainable, high-performing teams. This guide explores the definition, components, and economic implications of a living wage, providing a roadmap for financial health in an era of fluctuating inflation and shifting market demands.

Understanding the Living Wage: Definition and Distinctions

To grasp the importance of a living wage, one must first distinguish it from other forms of compensation. In the world of finance, clarity is the precursor to effective decision-making.

Living Wage vs. Minimum Wage: The Fundamental Difference

The most common point of confusion lies between the “minimum wage” and a “living wage.” The minimum wage is a statutory requirement—the lowest amount an employer can legally pay an employee. In many regions, the minimum wage is not indexed to inflation or the local cost of living, leading to a “wage gap” where full-time workers still find themselves below the poverty line.

Conversely, a living wage is a market-based measurement. It represents the actual cost of survival in a specific geographic area. For example, a living wage in San Francisco is significantly higher than a living wage in rural Ohio, despite the federal minimum wage being identical for both locations. From a personal finance perspective, aiming for a minimum wage job is a strategy for survival; aiming for a living wage is a strategy for stability.

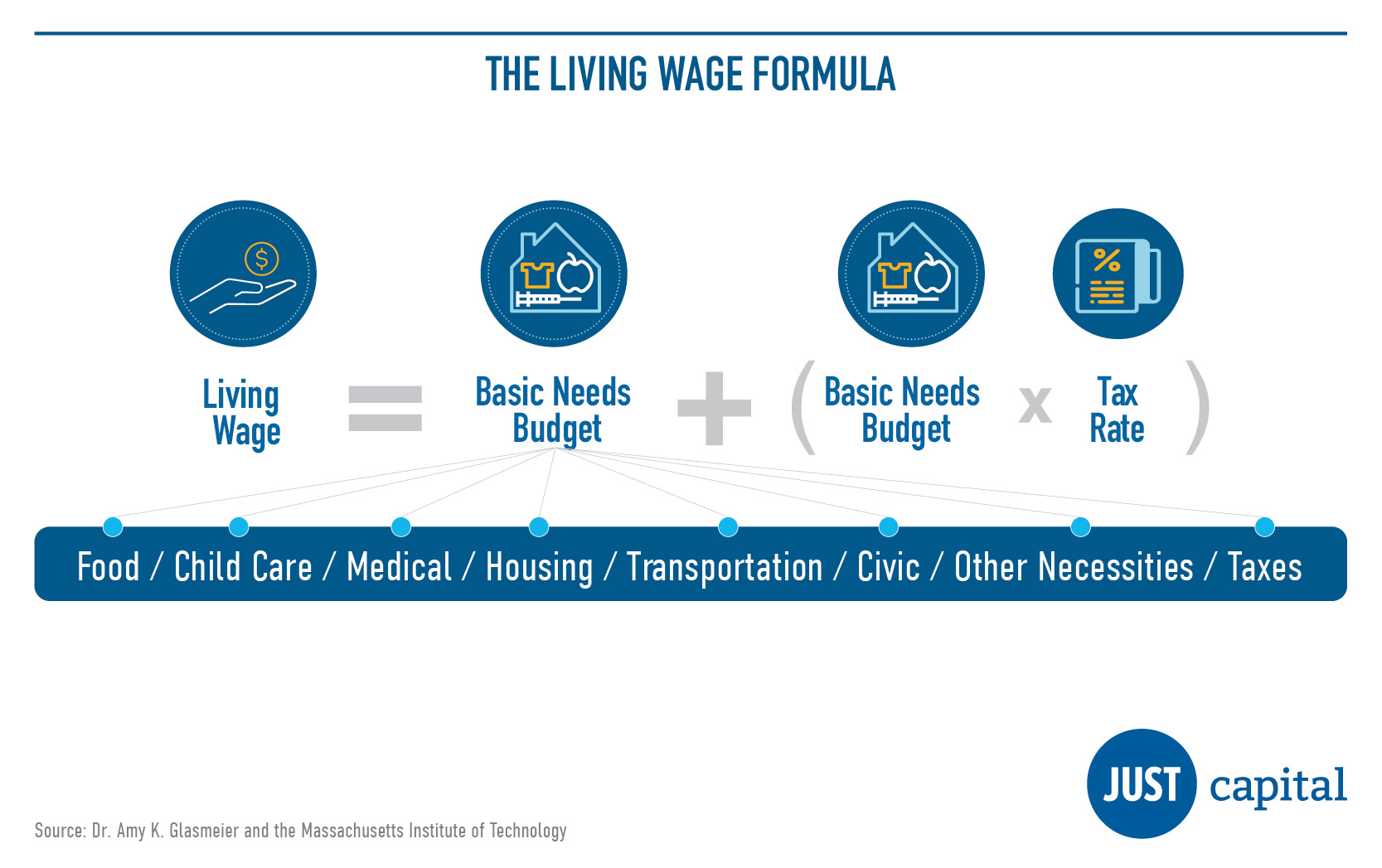

The Calculation Methodology: How Living Wages Are Determined

Calculating a living wage involves a complex synthesis of data. Economists typically use the “Basic Needs Budget” approach. This includes the cost of housing, food, healthcare, transportation, and taxes, while also accounting for a small margin for emergencies.

Tools like the MIT Living Wage Calculator have become industry standards for determining these figures. These tools analyze local market data to provide a realistic snapshot of what an individual or a family needs to earn to remain self-sufficient. For a single adult, the living wage covers the basics; for a household with children, the figure scales drastically to include childcare and increased insurance premiums.

The Essential Pillars of a Living Wage

A living wage is not about luxury; it is about the fundamental requirements for a dignified life. When we look at personal finance through the lens of a living wage, we identify five key pillars that must be covered by one’s income.

Housing and Utilities: The Largest Financial Burden

In almost every economy, housing is the most significant expenditure. The general rule of thumb in personal finance is that housing costs should not exceed 30% of gross income. A true living wage ensures that a worker can afford a modest apartment that meets health and safety standards without exceeding this threshold. When housing eats up 50% or more of an income—a condition known as being “rent-burdened”—there is little room left for saving or investing, which are the hallmarks of long-term financial health.

Nutrition and Healthcare: Non-Negotiable Essentials

A living wage must provide for a nutritionally adequate diet based on local food prices. Beyond calories, it must also account for the cost of health insurance premiums and out-of-pocket medical expenses. In many financial models, the inability to cover an unexpected $400 medical bill is a sign of financial fragility. A living wage provides the buffer necessary to manage these health-related costs without resorting to high-interest credit card debt.

Transportation and Personal Development

Whether it is the cost of public transit or the maintenance and fueling of a modest vehicle, transportation is a prerequisite for maintaining employment. Furthermore, a living wage includes a small allocation for “miscellaneous” expenses, which often covers basic personal care and, crucially, the ability to invest in minor self-improvement or community participation. Without this, an individual is functionally isolated from the economy they serve.

Why a Living Wage Matters for Business Finance and Growth

From a business perspective, the conversation around living wages is often viewed through the lens of “costs.” However, insightful business leaders recognize that paying a living wage is an investment in human capital that yields significant financial returns.

Boosting Employee Productivity and Reducing Turnover

The “Efficiency Wage Theory” suggests that when employees are paid above the market minimum—specifically a living wage—they are more productive. Financial stress is a major distractor; an employee worried about eviction or skipping meals is unlikely to perform at their peak.

Moreover, turnover is one of the “hidden killers” of business finance. The cost of recruiting, hiring, and training a replacement can range from 50% to 200% of the outgoing employee’s annual salary. By paying a living wage, businesses increase employee loyalty, drastically reducing these churn costs and retaining institutional knowledge.

The Ethical Brand Advantage: Attracting the Modern Consumer

While we are focusing on the “Money” niche, the financial reality is that modern consumers vote with their wallets. Companies that publicly commit to living wage standards often see a “reputation premium.” This can lead to increased customer loyalty and the ability to command higher price points for products and services. In the long run, being a living-wage employer can be a more sustainable financial strategy than a “race to the bottom” on labor costs.

Practical Strategies to Bridge the Income Gap

For individuals currently earning below a living wage, or for businesses looking to transition to a living-wage model, several financial strategies can be employed to bridge the gap.

Leveraging Side Hustles and Online Income Streams

In the modern economy, the traditional 9-to-5 may not always provide a living wage immediately. Many individuals utilize the “side hustle” to supplement their primary income. This could include freelance work, participating in the gig economy, or selling products online. From a personal finance standpoint, the key is to ensure that the “profit” from these activities—after taxes and expenses—actually moves the needle toward a living wage, rather than just adding to one’s burnout.

Investing in Upskilling for Higher Earning Potential

The most effective way to permanently secure a living wage is to increase one’s value in the marketplace. This involves “upskilling”—acquiring new certifications, learning high-demand technical skills, or pursuing further education. Many forward-thinking companies now offer tuition reimbursement or internal training programs. For the individual, treating education as a capital investment is a primary strategy for long-term income growth.

The Future of Compensation and Financial Well-being

As we look toward the future, the definition of a living wage will continue to evolve alongside technology and global economic shifts. Several factors will dictate how we view “fair pay” in the coming decade.

The Impact of Remote Work and Geographic Arbitrage

The rise of remote work has introduced a new variable into the living wage equation: geographic arbitrage. A worker can now earn a “New York City wage” while living in a region with a much lower cost of living. This has profound implications for personal wealth building, allowing individuals to maximize their savings and investment rates. Businesses, too, are recalculating their compensation structures, moving away from “location-based” pay toward “value-based” pay.

Automation and the Universal Basic Income Debate

As AI and automation transform the labor market, some jobs that currently pay a living wage may disappear. This has sparked a global financial debate regarding Universal Basic Income (UBI)—a government-guaranteed floor that would ensure every citizen has the equivalent of a living wage regardless of employment status. While still controversial, the discussion highlights the growing recognition that financial stability is the bedrock of a functioning economy.

In conclusion, a living wage is more than a social ideal; it is a fundamental metric of economic health. For the individual, it represents the threshold of financial freedom and the ability to build a future. For the business, it represents a commitment to quality and a strategy for sustainable growth. By understanding and advocating for a living wage, we move closer to an economy where financial security is not a luxury for the few, but a standard for the many.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.