A home warranty policy serves as a critical financial tool for homeowners, offering a distinct layer of protection against the often-unpredictable costs associated with maintaining a household. Unlike homeowners insurance, which typically covers structural damage from unforeseen events like fires or storms, a home warranty specifically targets the repair or replacement of major home systems and appliances that break down due to normal wear and tear. For many, understanding this distinction and the policy’s financial implications is key to sound personal finance management within homeownership.

Understanding the Fundamentals of a Home Warranty

At its core, a home warranty is a service contract designed to provide financial relief when essential household components malfunction. Homeowners pay an annual premium and, in most cases, a service fee per claim, in exchange for coverage on specific items. This financial arrangement aims to buffer the impact of costly repairs that could otherwise significantly disrupt a household budget.

Differentiating from Homeowners Insurance

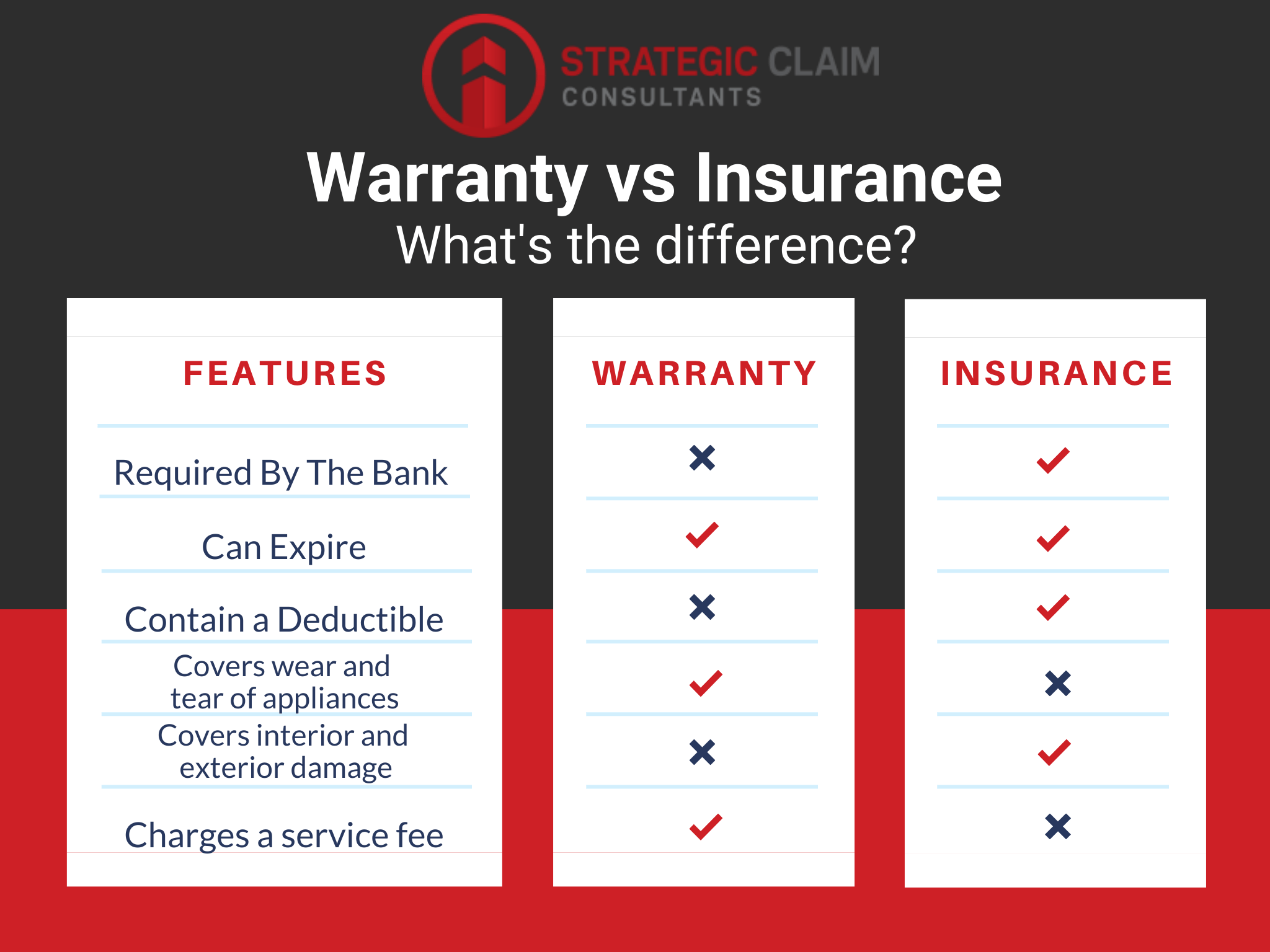

It’s crucial for homeowners to recognize that a home warranty is not a substitute for homeowners insurance; rather, it complements it. Homeowners insurance is a mandatory financial product for most mortgage holders, protecting the home’s structure and contents against catastrophic events such as fire, theft, vandalism, or certain natural disasters. It covers perils and damages, often with a deductible for each claim.

In contrast, a home warranty focuses on the functional components within the home. Imagine your air conditioning unit suddenly stops working on a sweltering summer day, or your refrigerator gives out, jeopardizing your groceries. These are scenarios where a home warranty would typically come into play. It addresses breakdowns due to age and normal use, which homeowners insurance explicitly excludes. From a financial planning perspective, this means managing two separate but equally important risk factors: external perils and internal system failures.

Core Coverage Areas

While specific coverage can vary significantly between providers and policy tiers, most home warranty plans include a standard set of home systems and major appliances. Understanding these core areas helps homeowners assess the value proposition against their personal assets and potential liabilities.

Typical Systems Covered:

- HVAC Systems: Heating, ventilation, and air conditioning units, including ductwork. This is often one of the most expensive systems to repair or replace, making its inclusion a significant financial benefit.

- Plumbing Systems: Pipes, drains, water heaters, and toilet mechanisms. Burst pipes or water heater failures can lead to not only repair costs but also potential water damage.

- Electrical Systems: Wiring, outlets, switches, and circuit breaker panels. Electrical issues can be both costly and dangerous, necessitating professional intervention.

Typical Appliances Covered:

- Kitchen Appliances: Refrigerator, oven, range, dishwasher, built-in microwave, and garbage disposal. These are high-use items prone to wear and tear.

- Laundry Appliances: Washer and dryer (often as an add-on or higher-tier inclusion).

- Other: Ceiling fans, garage door openers, and sometimes even central vacuum systems.

Many providers also offer optional add-on coverage for items like well pumps, septic systems, pools, spas, and additional refrigerators, allowing homeowners to customize their financial protection based on their specific property and assets.

The Financial Value Proposition: Costs and Benefits

Evaluating a home warranty requires a keen understanding of its financial implications. Like any financial product, it involves an outlay of capital—premiums and service fees—against the potential for future savings and peace of mind.

Policy Premiums and Service Fees

The cost of a home warranty policy generally comprises two main components:

- Annual or Monthly Premium: This is the primary cost, paid upfront annually or in monthly installments. Premiums can range from a few hundred dollars to over a thousand annually, depending on the coverage tier, location, and the property’s size.

- Service Call Fee (or Deductible): When a covered item breaks down and you initiate a claim, you’ll typically pay a service fee for the technician’s visit. This fee, similar to an insurance deductible but on a per-incident basis, can range from $60 to $125.

From a budgeting perspective, these costs need to be weighed against the potential cost of out-of-pocket repairs. For instance, if a refrigerator repair costs $500, and your service fee is $75, the warranty effectively saved you $425 on that single incident, not including the annual premium. Over several years, or with multiple unexpected breakdowns, these savings can accrue substantially.

Mitigating Unexpected Expenses

The most significant financial benefit of a home warranty is its ability to mitigate the impact of unexpected, high-cost repairs. The average lifespan of a major appliance or home system can vary, but breakdowns are inevitable. Replacing an HVAC unit could cost several thousands of dollars, while a new water heater might set you back hundreds, even over a thousand, with installation. Without a warranty, these expenses could force homeowners to dip into emergency savings, incur credit card debt, or delay other financial goals.

A home warranty acts as a financial buffer, converting potentially large, unpredictable expenses into smaller, predictable ones (the premium and service fee). This predictability is invaluable for personal budgeting and cash flow management, especially for those who prefer to avoid large, sudden expenditures. It allows homeowners to maintain their emergency fund for true emergencies, rather than depleting it on routine system failures.

Enhancing Home Value and Saleability

Beyond direct repair cost savings, a home warranty can indirectly contribute to a homeowner’s financial well-being by enhancing the property’s marketability. When selling a home, offering a transferable home warranty to prospective buyers can be a significant selling point. It provides buyers with confidence, assuring them that they won’t immediately face substantial repair costs for major systems or appliances shortly after moving in. This can make a home more attractive, potentially speeding up the sale process or even justifying a slightly higher asking price.

For sellers, it also offers protection during the listing period and ensures that any breakdowns discovered during inspection or prior to closing are handled without additional out-of-pocket costs, safeguarding their profit margins. This strategic use of a home warranty represents a smart financial maneuver in real estate transactions.

Key Considerations Before Purchasing

Before committing to a home warranty policy, a thorough financial due diligence is essential. Not all policies are created equal, and understanding the nuances can prevent future financial disappointment.

Reading the Fine Print: Exclusions and Limitations

The devil is often in the details, especially with service contracts. Home warranty policies come with various exclusions, limitations, and caps on coverage that directly impact their financial utility.

- Pre-existing Conditions: Most policies will not cover items with pre-existing conditions. If an appliance was already broken or showing signs of failure before the policy began, it will likely be excluded. This is a critical point for new buyers or those purchasing a policy for an older home.

- Improper Maintenance/Installation: Coverage can be denied if a system or appliance breaks down due to improper maintenance, installation, or misuse. Homeowners are expected to maintain their property reasonably.

- Coverage Caps: There are often maximum payout limits per item or per system, and sometimes an aggregate annual limit. For example, a policy might cover up to $2,000 for HVAC repairs, meaning if a full replacement costs $5,000, you’d still be responsible for the remaining $3,000. Understanding these caps helps set realistic expectations for potential savings.

- Types of Components: Some policies may only cover specific parts of a system (e.g., the compressor of an HVAC unit but not the freon lines), or they may not cover cosmetic damages.

Carefully reviewing the sample contract and asking direct questions about potential scenarios is vital to understanding the true financial protection offered.

Understanding Service Call Procedures

The efficiency and process of making a claim are central to the practical value of a home warranty.

- Claim Initiation: Homeowners typically contact the warranty provider when an item breaks down. The provider then dispatches a qualified technician from their network.

- Technician Network: The quality and availability of technicians can vary. While providers aim for timely service, homeowners usually don’t get to choose their own repair person, which can be a point of contention if a preferred local contractor is desired.

- Repair vs. Replacement: Policies generally state that the provider will repair a covered item first. If it’s deemed unrepairable or if the repair cost exceeds the value of the item, they will authorize a replacement. The replacement might not be an exact match to the original in terms of brand or features, but it will be of comparable quality and efficiency. This is a key financial consideration—you might not get the top-of-the-line replacement if your old unit was premium.

- Timelines: Response times for service calls can vary, especially for non-emergency items. This needs to be factored into the decision, as waiting a few days for a critical appliance like a refrigerator can be inconvenient and costly in spoilage.

Choosing the Right Provider

The home warranty industry is competitive, with numerous providers offering varying levels of service and coverage. Financial prudence dictates researching and comparing multiple companies.

- Reputation and Reviews: Check independent review sites and consumer protection agencies for feedback on customer service, claim processing, and overall satisfaction. A provider with a history of denying claims or slow service might not offer the financial peace of mind you seek.

- Coverage Options: Compare standard plans and available add-ons to ensure they align with your home’s specific systems and appliances.

- Cost Structure: Scrutinize premiums, service fees, and any hidden administrative charges. A lower premium might come with higher service fees or more restrictive coverage caps.

- Contract Length and Transferability: Consider the contract term and whether the policy is transferable if you plan to sell your home.

Is a Home Warranty a Wise Financial Decision for You?

The decision to purchase a home warranty is ultimately a personal financial one, balancing risk tolerance, budget, and the specific characteristics of your home. It’s not a universal solution but rather a tailored financial tool.

Assessing Your Home’s Age and Condition

Homes with older systems and appliances are generally considered better candidates for a home warranty. As components age, the likelihood of breakdowns due to normal wear and tear increases significantly. For a brand-new home with all new appliances, the initial years might see fewer benefits, as items are still under manufacturer warranties. However, for homes approaching the 5-10 year mark and beyond, where manufacturer warranties have expired and component lifespans are being tested, the financial protection can become more attractive. Evaluate the age and known condition of your HVAC, water heater, and major kitchen appliances. If many are older than 7-10 years, a home warranty might be a prudent investment to guard against imminent, costly failures.

Evaluating Your Financial Preparedness

Your personal financial situation plays a critical role. Do you have a robust emergency fund specifically earmarked for home repairs? Can you comfortably cover a $1,000-$5,000 unexpected repair without financial strain? If the answer is no, or if unexpected large expenses cause significant anxiety, a home warranty can provide a valuable layer of financial security. For those with ample liquid savings and a high tolerance for managing unexpected costs, the financial benefit might be less pronounced, and the money could potentially be better utilized elsewhere (e.g., higher-yield savings or investments). It’s essentially a form of financial hedging against an uncertain future.

Long-Term vs. Short-Term Value

Consider whether you view a home warranty as a short-term risk mitigation tool (e.g., for the first year after buying an older home, or while selling) or a long-term part of your home maintenance budget. For short-term needs, the value might be immediate and clear. For long-term considerations, you should annually re-evaluate the policy’s cost versus the actual claims made and the age of your home’s systems. Sometimes, after several years with few claims, you might find that setting aside the premium amount into a dedicated home repair fund offers a better return on investment, giving you more control over choosing technicians and replacement items.

Ultimately, a home warranty policy is a financial product designed to offer peace of mind and budgetary predictability against the inevitable wear and tear of home systems and appliances. By carefully weighing its costs, coverage, and your individual financial circumstances, you can make an informed decision on whether it aligns with your personal finance strategy for sustainable homeownership.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.