In the landscape of professional education, few examinations carry as much weight as the Medical College Admission Test (MCAT). While pre-medical students often view the exam through the lens of academic stress and scientific mastery, a more pragmatic analysis reveals that the MCAT is, in essence, a high-stakes financial gatekeeper. Identifying what constitutes a “great” MCAT score requires more than just looking at a percentile chart; it requires an understanding of the score’s role as a primary lever for long-term wealth building, debt mitigation, and career ROI.

A “great” score is not merely one that secures an acceptance letter. It is a score that optimizes a candidate’s “market value” in the eyes of admissions committees, potentially unlocking hundreds of thousands of dollars in merit-based aid and ensuring entry into high-earning medical specialties. In this guide, we will analyze the MCAT score through a financial and strategic lens, helping you understand how to benchmark your performance for maximum economic advantage.

The MCAT as a High-Yield Investment: Understanding the Baseline

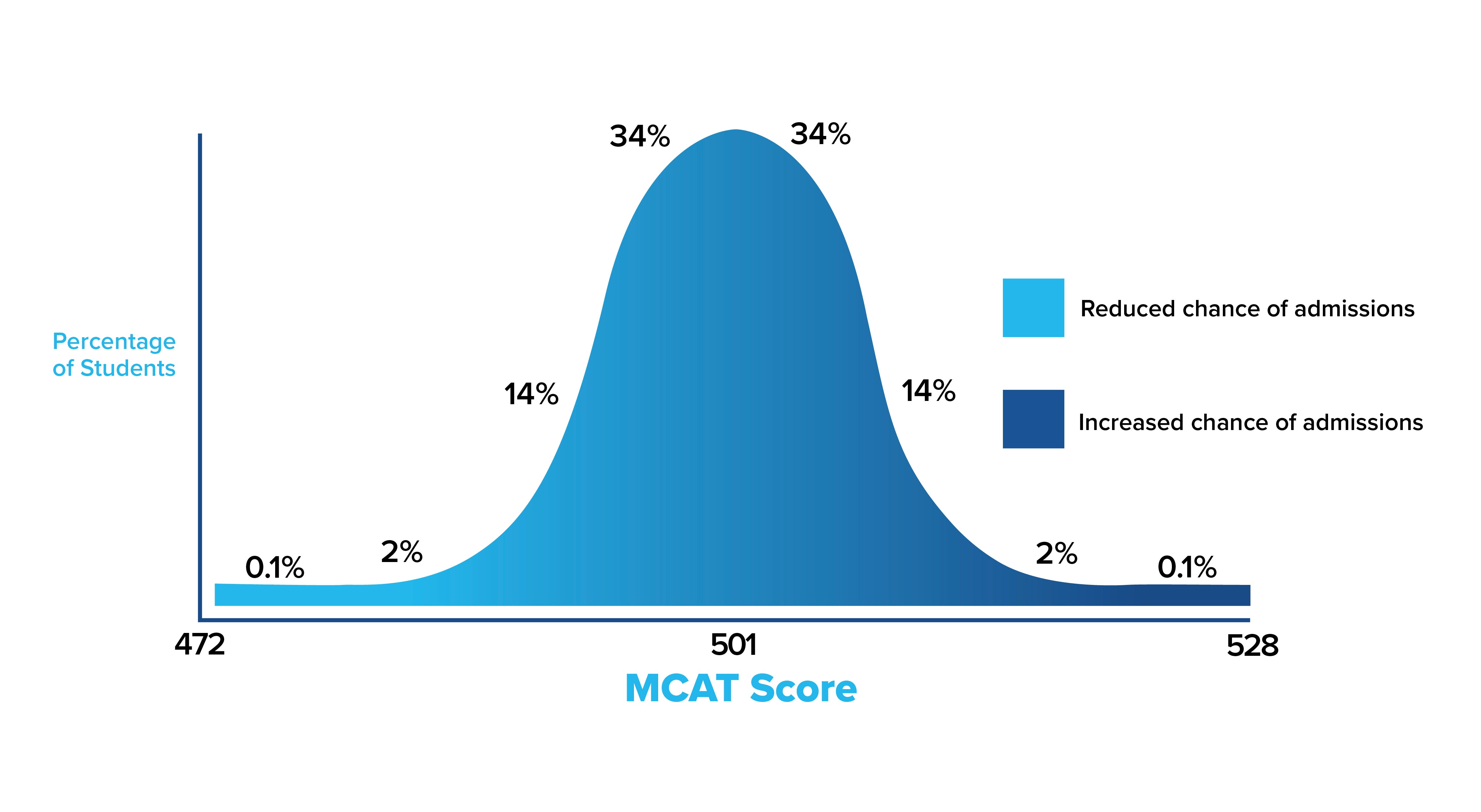

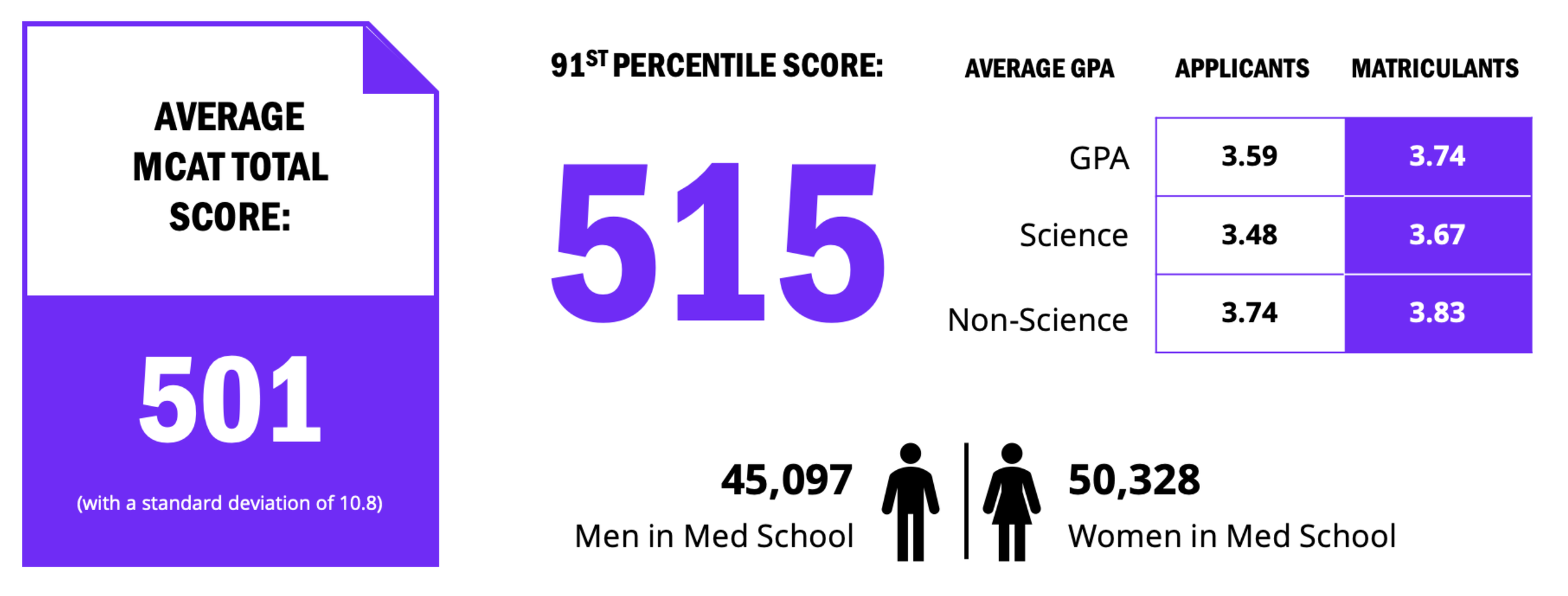

To understand the value of an MCAT score, one must first understand the “currency” of the scale. The MCAT is scored from 472 to 528, with the midpoint centered at 500. However, in the competitive market of medical school admissions, the “median” is rarely “great.” For the 2023-2024 application cycle, the average score for all applicants was approximately 506, while the average for those who actually matriculated (received an offer and enrolled) was approximately 511.9.

Defining “Great” by Competitive Benchmarks

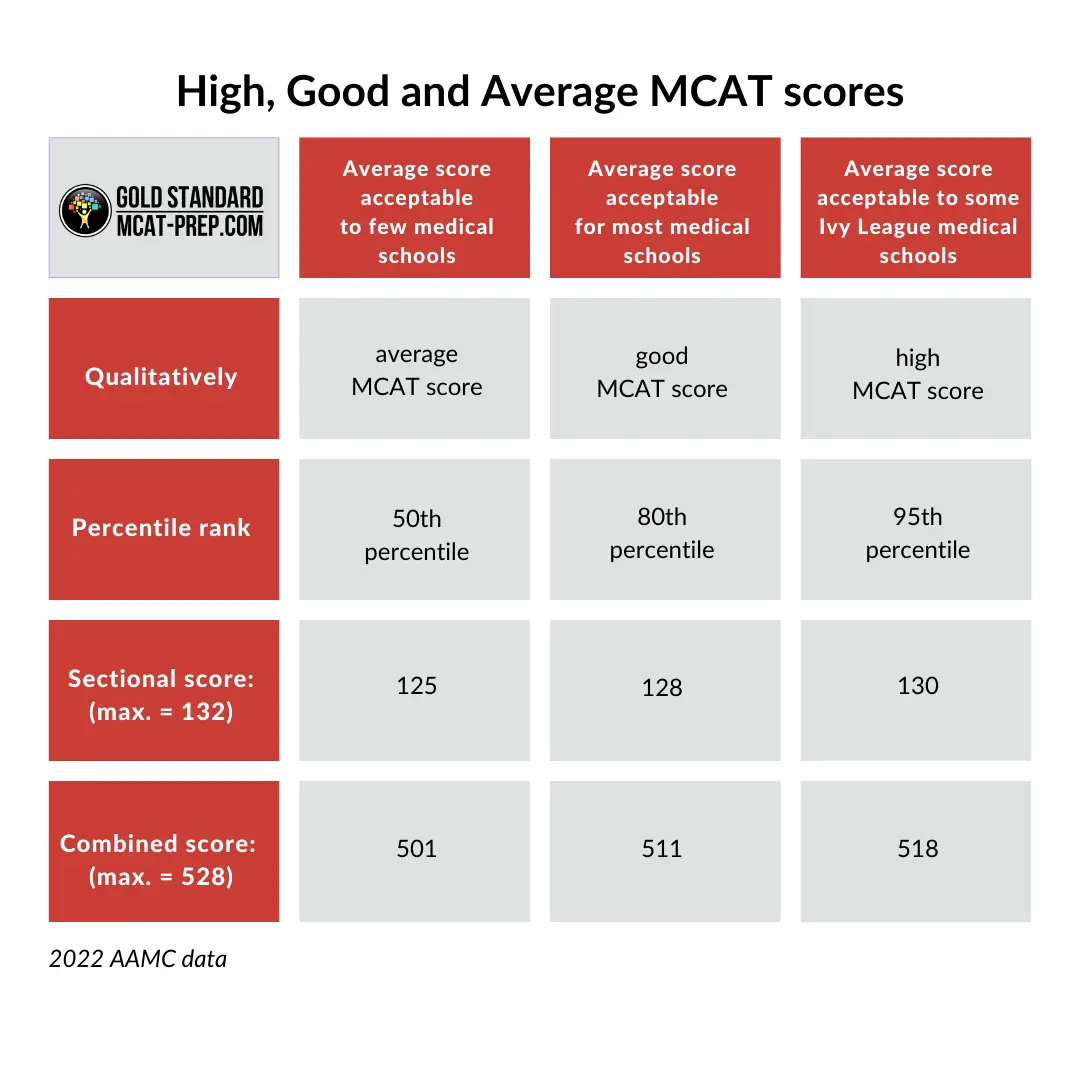

From a strategic standpoint, a “great” score is one that places an applicant in the top 20% of test-takers, typically a 511 or higher. However, to truly gain a competitive edge in the “elite” market—top-tier MD programs—the target shifts toward 515 and above. A score of 515 puts an individual in the 90th percentile, signaling to institutions that the candidate is a low-risk, high-reward investment. This distinction is critical because, in the business of medical education, schools are ranked partly based on the median MCAT scores of their incoming classes. By bringing a high score to the table, you are helping the institution maintain its “brand value,” which gives you significant leverage during the recruitment process.

The Correlation Between Scores and Institutional Tier

The financial disparity between attending a top-tier “Research” medical school and a lower-tier or unranked program can be substantial. Higher-ranked schools often have larger endowments, which translates to more robust financial aid packages. A “great” score (517+) often acts as the key to these prestigious institutions. While a 508 might get you into a private medical school with a $70,000 annual tuition and limited aid, a 518 could make you a prime candidate for a top-20 school that offers generous institutional grants, effectively altering your net worth by six figures before you even see your first patient.

Financial Implications of a Top-Percentile Score

When we discuss the MCAT in a financial context, we are primarily talking about the reduction of educational liabilities. Medical school is one of the most expensive investments a person can make, with the average debt for new physicians hovering around $200,000 to $250,000. A great MCAT score is the most effective tool available for lowering this “entry price.”

Merit-Based Scholarships and Debt Mitigation

Most medical schools use MCAT scores as a primary filter for merit-based scholarships. Unlike “need-based” aid, which is tied to your financial history, merit-based aid is tied to your performance metrics. It is not uncommon for students in the 98th or 99th percentile (521-528) to receive “full-ride” or “full-tuition” offers from mid-to-high tier programs looking to “buy” a higher class profile.

Consider the math: if an extra five points on your MCAT earns you a $40,000 annual scholarship, that score is effectively worth $160,000 over four years. When you factor in the avoided interest on student loans (often at rates of 6% to 8%), a great MCAT score can represent a $250,000 increase in your lifetime wealth. In this light, the time spent studying is perhaps the highest-paying “side hustle” a student will ever have.

Avoiding the Costly “Gap Year” Cycle

There is a significant opportunity cost associated with an average or mediocre MCAT score. If a score is not high enough to secure an admission on the first attempt, the applicant often faces a “gap year.” From a personal finance perspective, a gap year is not just a year of “waiting”; it is a lost year of an attending physician’s salary.

If an orthopedic surgeon or cardiologist earns $500,000 a year, delaying their entry into the workforce by one year due to a weak MCAT score is a $500,000 loss in lifetime earnings. Furthermore, the cost of reapplying—including secondary fees, updated prep materials, and travel for interviews—can easily exceed $5,000 to $10,000. Therefore, achieving a “great” score on the first attempt is a critical move in capital preservation.

Budgeting for the Score: Cost-Benefit Analysis of Prep Tools

Achieving a top-tier score usually requires an upfront investment in preparation. Because the financial stakes are so high, it is essential to view MCAT prep not as an expense, but as a capital expenditure. However, like any investment, it must be managed with an eye on ROI.

Evaluating the ROI of Prep Courses vs. Self-Study

The market for MCAT preparation is vast, ranging from $500 self-study bundles to $10,000 private coaching packages. For many, the “sweet spot” of ROI lies in high-quality on-demand resources and comprehensive question banks (like UWorld or the official AAMC materials).

- Self-Study (Cost: $500 – $1,500): High ROI for disciplined students. Focuses on purchasing the necessary “tools” without the overhead of a formal classroom.

- Guided Courses (Cost: $2,500 – $5,000): Moderate ROI. These provide structure and “insurance” against procrastination. If a course raises your score from a 505 to a 512, the $3,000 spent is a bargain compared to the scholarship potential unlocked.

- Private Tutoring (Cost: $150 – $500/hour): High cost, but potentially high ROI for those stuck at a “plateau.” If a tutor helps you break into the 520+ range, the investment pays for itself via merit aid.

Hidden Costs of Retaking the Examination

One of the most common financial mistakes pre-medical students make is taking the exam before they are ready. A “practice run” is an expensive error. The registration fee alone is over $330, but the real cost is the “red flag” it may place on your academic transcript. Most medical schools see all your scores. A trajectory of 500 then 515 is good, but a single 515 is better. Every retake costs more in prep, time, and emotional capital. Strategically, it is better to spend an extra $1,000 on prep to ensure a “great” score the first time than to pay for two separate attempts and the associated application delays.

Long-Term Career ROI: From Test Day to Attending Salary

The influence of a great MCAT score extends far beyond the admissions office. It sets a trajectory for the types of clinical opportunities and residencies that will eventually dictate your career’s financial ceiling.

Specialized Residency Placement and Earning Potential

While medical school performance and USMLE (Step) scores are the primary drivers for residency placement, the “tier” of the medical school you attend plays a massive role in where you land for residency. Top-tier medical schools have the “brand power” and alumni networks to place students into highly competitive, high-paying specialties like Dermatology, Plastic Surgery, or Neurosurgery.

As established earlier, a great MCAT score is the primary ticket into these top-tier schools. Therefore, there is a direct, albeit multi-step, correlation between a 520 MCAT score and the ability to enter a specialty with a $600,000 annual salary versus a $250,000 salary in a less competitive field. In the world of finance, this is known as “positioning”—putting yourself in the best possible environment to capture future upside.

The Multiplier Effect of Early Career Entry

The final financial consideration of a “great” MCAT score is the “velocity of money.” By scoring well, getting in early, and potentially qualifying for accelerated programs (like 3-year MD tracks offered to high-performing candidates), you begin earning an attending salary sooner.

When you start earning high wages earlier in life, you benefit from the power of compound interest in your retirement accounts (401k, 403b, or private brokerage). A physician who starts investing at age 30 instead of 32 will have a significantly larger nest egg by age 65, even if the total amount invested is the same. The “great” MCAT score is the catalyst that starts this financial clock.

Conclusion

In the final analysis, a “great” MCAT score is defined by its ability to provide options. It is a tool for financial liberation that allows a student to choose a medical school based on “fit” and “cost” rather than just “acceptance.” By aiming for a score in the 515+ range, applicants are doing more than just studying science; they are engaging in a sophisticated form of personal financial planning.

The investment of $2,000 in prep and 500 hours of study time can yield a “profit” of $200,000 in scholarships and millions in lifetime earnings through better specialty placement and earlier career entry. In the business of becoming a doctor, the MCAT is the most important “deal” you will ever negotiate. Treat it with the financial seriousness it deserves, and the dividends will support your professional life for decades to come.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.