In the landscape of higher education, the Preliminary SAT/National Merit Scholarship Qualifying Test (PSAT/NMSQT) is frequently misunderstood as a mere “practice run” for the SAT. However, for a high school junior, the PSAT is far more than a diagnostic tool; it is a critical financial instrument. A “good” score is not just a reflection of academic aptitude, but a gateway to significant merit-based aid, institutional grants, and a reduced reliance on student loans.

From a financial planning perspective, understanding what constitutes a competitive PSAT score allows families to maximize their return on investment (ROI) in the college admissions process. This article explores how to define a “good” score through the lens of financial strategy, scholarship acquisition, and long-term wealth management.

1. The PSAT as a Financial Asset: The National Merit Scholarship Program

For a junior, the primary financial incentive of the PSAT is the National Merit Scholarship Program (NMSP). This is where the “practice” test transforms into a high-stakes competition for capital.

Understanding the National Merit Scholarship Corporation (NMSC)

To qualify for the NMSP, a student must be in their junior year. The “Selection Index” score, derived from your PSAT Reading, Writing, and Math scores, determines your eligibility. While thousands of students achieve high scores, only about 16,000 are named Semifinalists. This designation is the first step toward unlocking a variety of scholarship tiers that can drastically alter a family’s financial planning for college.

The Monetary Value of a Qualifying Score

A “good” score in this context is one that places a student in the top 1% of their state. The direct financial rewards include:

- National Merit $2,500 Scholarships: A one-time payment that assists with initial university costs.

- Corporate-Sponsored Scholarships: Many corporations provide renewable awards for children of employees or students with specific career interests who reach Finalist status.

- College-Sponsored Scholarships: This is the most lucrative category. Many prestigious universities offer “Full-Ride” or “Full-Tuition” scholarships specifically to National Merit Finalists to attract top-tier talent to their campuses. In terms of ROI, a few hours spent on PSAT prep can yield over $100,000 in tuition savings.

2. Defining “Good” Through the Lens of Merit-Based Institutional Aid

Even if a student does not reach the Semifinalist threshold for the National Merit program, a high PSAT score remains a powerful tool for securing institutional merit aid. Many colleges use PSAT scores as early indicators to identify prospective students to whom they will later offer financial incentives.

Benchmarking for Merit-Based Funding

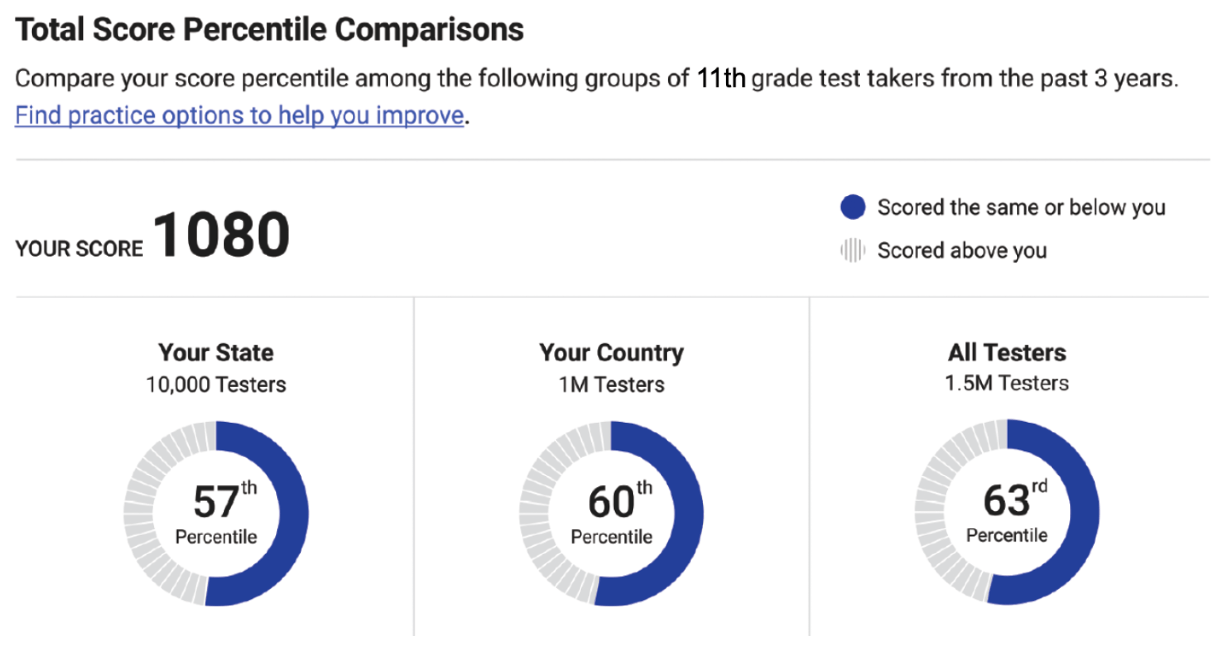

A “good” score for securing merit aid is typically one that places a student in the 90th percentile or higher (generally a score of 1200–1300+). From a financial standpoint, these scores signal to a university’s admissions and financial aid offices that the student is a low-risk, high-reward investment. High-scoring students improve the university’s overall ranking, and institutions are willing to “buy” that talent through tuition discounts and grants.

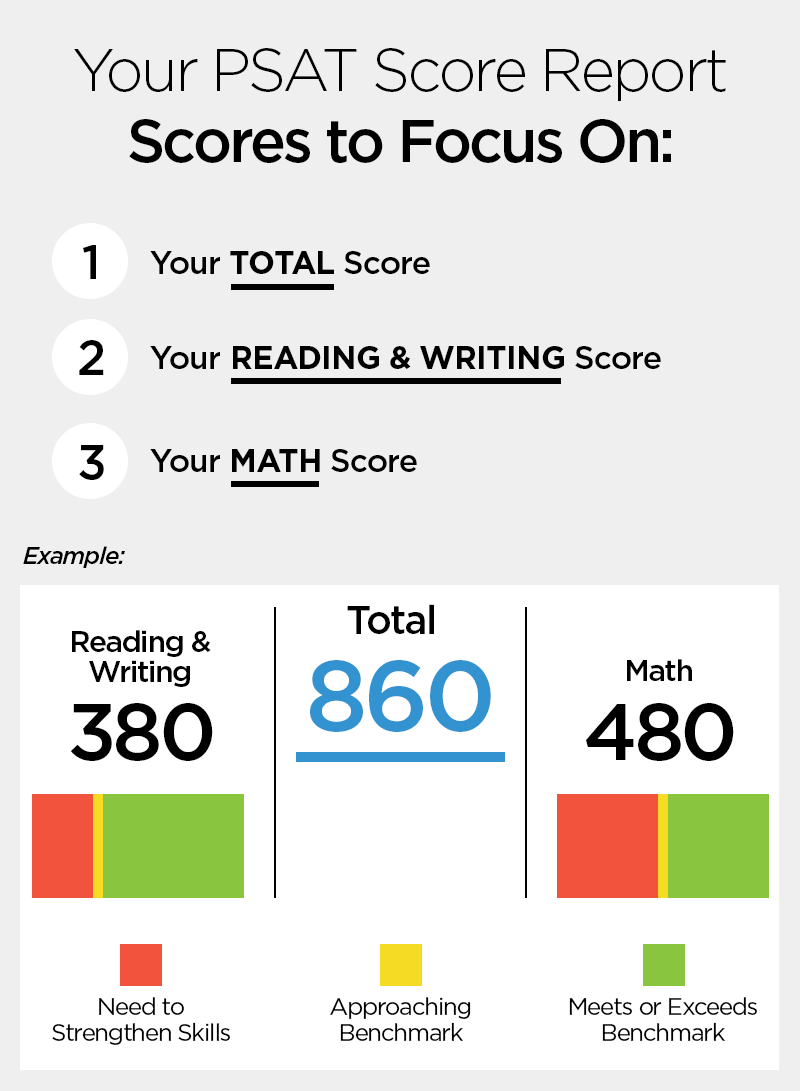

Percentiles vs. Selection Index: Navigating Financial Gateways

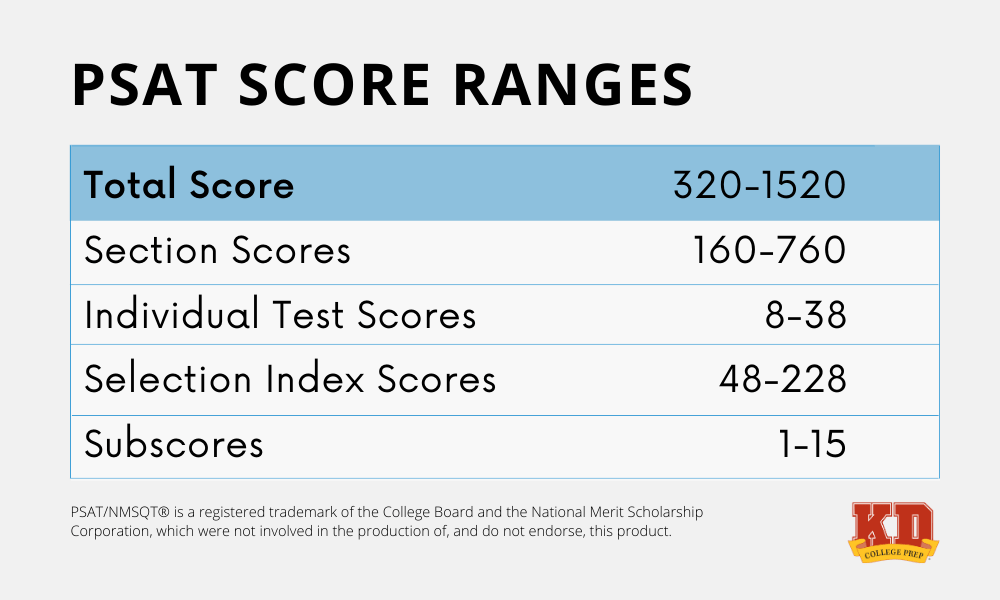

When assessing your score, you must look at two different metrics. The total score (out of 1520) is what most students focus on, but the Selection Index (2x Reading & Writing + Math) is the metric that governs scholarship eligibility. A “good” total score might be 1350, but if the sub-scores are lopsided, it might not reach the Selection Index cutoff for your state. Strategically balancing these scores is essential for those looking to leverage their performance into a financial package.

3. The ROI of Test Preparation: Investing Capital for Future Gains

In the world of personal finance, we often discuss the importance of investing early. Preparing for the PSAT as a junior is an investment of both time and money (tutors, books, or online courses) that offers a disproportionately high rate of return.

Investing in Prep vs. Future Tuition Savings

Consider the cost-benefit analysis of a $500 test prep course. If that investment helps move a student from the 85th percentile to the 99th percentile, the resulting scholarship opportunities could cover the entirety of a four-year degree. Very few financial vehicles offer a 20,000% return on investment within a single year. Therefore, a “good” score is the target that justifies the initial expenditure on preparation.

Tech-Driven Financial Efficiency in Study Tools

Modern technology has lowered the barrier to entry for high-level test prep. Utilizing AI-driven platforms like Khan Academy or specialized adaptive software allows students to target their weaknesses with surgical precision. This efficiency means less time spent “studying” and more time “strategizing,” effectively maximizing the student’s “hourly wage” in terms of potential scholarship dollars earned per hour of study.

4. Strategic Score Improvement for Maximum Funding

To move a PSAT score from “average” to “financially transformative,” a junior must treat the exam like a business problem. It requires identifying the highest-leverage areas for growth.

Analyzing Sub-Scores for Targeted Growth

The PSAT provides a detailed breakdown of performance in specific categories like “Command of Evidence” or “Heart of Algebra.” For a junior aiming for a scholarship-qualifying score, a “good” strategy involves identifying which section provides the easiest path to more points. In many cases, the Math section is the most “trainable,” offering a higher ROI for students who memorize specific formulas and logic patterns.

The Transition from PSAT to SAT/ACT for Financial Leverage

A strong PSAT score serves as the foundation for the SAT. Most students who score well on the PSAT will see a correlated performance on the SAT, which is the primary metric used by the majority of US colleges to determine the “discount rate” on tuition. By securing a “good” PSAT score, a student effectively front-loads the work required to secure their future financial aid packages, reducing stress and allowing more time to focus on other revenue-generating or resume-building activities during their senior year.

5. Long-Term Financial Implications of High PSAT Performance

The benefits of a high PSAT score extend beyond the freshman year of college. It sets a trajectory for a student’s entire financial future.

Diversifying Your Scholarship Portfolio

A high PSAT score makes a student a “preferred candidate” for private scholarships. Many foundations and local organizations look at PSAT/SAT performance as a baseline for their own financial awards. By hitting a “good” score early, a junior can build a diversified portfolio of scholarships that covers not just tuition, but also housing, books, and study-abroad programs.

Reducing Student Loan Dependency

The most significant financial advantage of a high PSAT score is the reduction—or total elimination—of student loan debt. The average student graduates with significant debt that can take decades to repay, impacting their ability to buy a home, invest in the stock market, or start a business. A “good” PSAT score is the first line of defense against this debt. By securing merit-based aid, a junior is essentially gifting their future self a massive financial head start.

Conclusion: The Bottom Line on PSAT Scoring

What is a “good” PSAT score for a junior? While the College Board might provide one answer based on academic benchmarks, a financial perspective provides another.

A score of 1000-1100 is a solid baseline for general college readiness. However, from a money-management perspective, a “good” score starts at 1200, where institutional merit aid begins to manifest. A “great” score is 1350 and above, where significant tuition discounts become common. An “elite” score—one that reaches the 1450+ range—is a financial powerhouse that can unlock full-ride scholarships and change the economic trajectory of a student’s life.

Treat the PSAT not as a test of intelligence, but as a competitive application for a high-paying financial grant. By shifting the focus from “passing a test” to “acquiring capital,” juniors and their families can approach the PSAT with the strategic seriousness it deserves. In the end, the best PSAT score is the one that allows a student to graduate with a world-class education and zero financial liability.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.