Determining what constitutes a “good” mortgage rate is one of the most significant financial challenges facing prospective homeowners today. For decades, the answer was relatively static, but the economic volatility of the early 2020s has fundamentally shifted the benchmark. A good rate is no longer just a number; it is a complex intersection of national economic policy, your personal financial health, and the specific type of loan product you choose.

To understand what a good rate looks like in the current market, one must look beyond the daily headlines and analyze the mechanics of the mortgage industry. Whether you are a first-time homebuyer or a seasoned real estate investor, securing a favorable interest rate can save you tens, or even hundreds, of thousands of dollars over the life of a 30-year loan. This article explores the parameters of a good mortgage rate and provides a roadmap for achieving the best possible terms for your financial future.

Understanding the Economic Climate: What Defines “Good” Right Now?

The definition of a good mortgage rate is inherently relative. To a borrower in the early 1980s, a 10% interest rate would have been considered an absolute steal, given that rates peaked near 18%. Conversely, to a borrower in 2021, a 5% rate might have seemed prohibitively expensive compared to the historic lows of 2.5% to 3%.

The Historical Perspective vs. Today

When evaluating today’s rates, it is vital to maintain a long-term perspective. Historically, the average 30-year fixed-rate mortgage has hovered around 7.5% to 8%. Therefore, from a historical standpoint, anything below 7% remains mathematically “good.” However, the psychological “anchor” for many consumers remains the ultra-low rates seen during the pandemic era. Navigating today’s market requires shedding that expectation and looking at the “Real Interest Rate”—the interest rate adjusted for inflation. If inflation is high, a seemingly high mortgage rate may actually be lower in real terms than it appears.

The Role of the Federal Reserve and Bond Yields

While the Federal Reserve does not set mortgage rates directly, its influence is paramount. Mortgage rates are most closely tied to the yield on the 10-year Treasury note. When the Fed raises the federal funds rate to combat inflation, Treasury yields generally rise, and mortgage lenders follow suit to maintain their profit margins. A “good” rate in a rising-rate environment is typically one that is at or slightly below the national average for your specific credit tier. Staying informed about the Fed’s “dot plot”—their projected path for interest rates—can help you time your home purchase during windows of relative stability.

Factors That Determine Your Specific Rate

Market averages are merely a baseline. The actual rate a lender quotes you—the “personal” mortgage rate—is determined by a risk assessment of your financial profile. Understanding these levers allows you to pull them in your favor.

Credit Scores and Their Impact

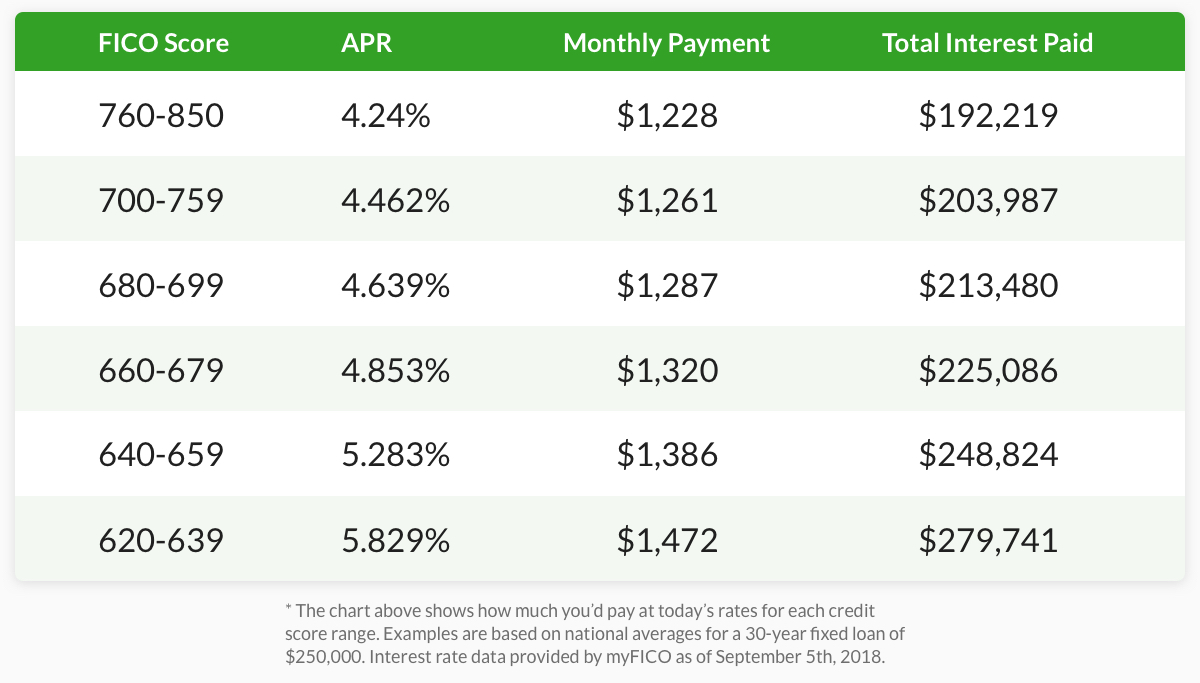

Your FICO score is the single most influential factor in the rate you are offered. Lenders categorize borrowers into “tiers.” Generally, a score of 760 or higher is required to qualify for the best available market rates. A borrower with a 760 score might receive a rate that is 0.5% to 1% lower than someone with a 660 score. Over a $400,000 mortgage, that 1% difference can translate to nearly $250 a month in savings. To secure a good rate, it is often worth delaying a purchase by six months to aggressively pay down credit card debt or dispute errors on your credit report to move into a higher scoring tier.

Loan-to-Value (LTV) Ratios and Down Payments

The “skin you have in the game” dictates the lender’s risk. The Loan-to-Value ratio (the percentage of the home’s value you are borrowing) plays a critical role. A 20% down payment (resulting in an 80% LTV) is the traditional benchmark for avoiding Private Mortgage Insurance (PMI) and securing a lower interest rate. However, some lenders offer “price breaks” at specific LTV intervals, such as 75% or 70%. If you are close to one of these thresholds, contributing a few extra thousand dollars to your down payment could move you into a lower interest rate bracket.

Debt-to-Income (DTI) Ratios

Lenders look at your Debt-to-Income ratio to ensure you have the cash flow to manage a mortgage. This is the percentage of your gross monthly income that goes toward paying debts. Most conventional lenders prefer a DTI of 36% or lower, though some programs allow up to 43% or even 50%. A lower DTI doesn’t always guarantee a lower interest rate, but it increases your “fundability,” giving you more leverage to shop around and negotiate with multiple lenders.

Different Loan Products and Their Rate Structures

A “good” rate for one type of loan might be a “bad” rate for another. Matching the loan product to your specific timeline and financial goals is essential.

Fixed-Rate Mortgages vs. ARMs

The 30-year fixed-rate mortgage is the gold standard for stability. You lock in a rate, and it never changes. However, if you plan to move or refinance within five to seven years, an Adjustable-Rate Mortgage (ARM) might offer a “good” rate that is significantly lower than the 30-year fixed. For example, a 5/1 ARM might offer an initial rate that is 0.75% lower than a fixed-rate loan. The risk, of course, is that the rate will adjust upward after the five-year “teaser” period. A good rate here is one that provides enough initial savings to offset the potential for future increases.

Government-Backed Loans (FHA, VA, USDA)

For borrowers who may not qualify for conventional financing, government-backed loans offer competitive rates, often lower than conventional rates. FHA loans are designed for lower credit scores, while VA loans (for veterans) and USDA loans (for rural properties) often offer some of the lowest rates in the market with $0 down. When comparing these, look at the “Total Cost of Credit,” as FHA loans carry permanent mortgage insurance premiums that can make the effective rate higher than it initially appears.

Jumbo Loans vs. Conventional Loans

In high-cost real estate markets, you may need a “Jumbo” loan—a mortgage that exceeds the conforming loan limits set by the Federal Housing Finance Agency (FHFA). Interestingly, Jumbo rates can sometimes be lower than conventional rates because they are held by banks on their own balance sheets rather than being sold to Fannie Mae or Freddie Mac. If you are a high-net-worth individual with significant assets, a “good” Jumbo rate might involve specialized “relationship pricing” from a private bank.

Strategies for Securing the Lowest Possible Rate

Once you understand the market and your personal profile, you must actively hunt for the best rate. Rates are not set in stone; they are highly negotiable.

The Art of Rate Shopping and Comparison

According to the Consumer Financial Protection Bureau (CFPB), borrowers who shop around with at least three different lenders save an average of $3,500 in the first few years of their loan. Don’t just talk to your primary bank. Check with credit unions, online lenders, and mortgage brokers. A mortgage broker acts as an intermediary, shopping your profile to dozens of wholesale lenders to find the most competitive “niche” rate for your specific situation.

Mortgage Points: To Buy or Not to Buy?

One way to secure a rate below the market average is to “buy down” the rate using discount points. One point typically costs 1% of the loan amount and reduces your interest rate by approximately 0.25%. Determining if this is a “good” move depends on your “break-even point.” If paying $4,000 for points saves you $100 a month, your break-even point is 40 months. If you plan to stay in the home for 10 years, buying points is a mathematically sound strategy to secure a lower rate.

Locking in Your Rate at the Right Time

Mortgage rates fluctuate daily, sometimes hourly. Once you find a rate you are happy with, you should “lock” it. A rate lock typically lasts 30 to 60 days. In a volatile market, a “float-down” option is also valuable—this allows you to lock in a rate but take advantage of a lower rate if market conditions improve before you close.

The “Total Cost” Perspective: Beyond the Interest Rate

A low interest rate can be a Trojan horse if it is accompanied by exorbitant fees. To truly identify a good deal, you must look at the Annual Percentage Rate (APR).

Closing Costs and Hidden Fees

The interest rate is the cost of borrowing the principal, but the APR includes the interest rate plus other costs like origination fees, mortgage insurance, and prepaid interest. A lender might offer a 6.5% interest rate but charge $10,000 in fees, while another offers 6.7% with $2,000 in fees. In many cases, the 6.7% loan is the superior financial choice. Always request a Loan Estimate (LE) from every lender you speak with and compare the “Total Interest Percentage” (TIP) and APR.

The Long-Term Impact of a 0.5% Difference

It is easy to become desensitized to small fractions, but in the world of personal finance, 0.5% is monumental. On a $500,000, 30-year mortgage, the difference between a 6.5% rate and a 7.0% rate is roughly $165 per month. Over the life of the loan, that small 0.5% difference results in nearly $60,000 in extra interest payments. When you realize that $60,000 is the equivalent of a college education or a significant portion of a retirement fund, the pursuit of a “good” rate becomes a critical pillar of your long-term wealth strategy.

In conclusion, a good mortgage rate is the one that minimizes your total cost of ownership while fitting within your monthly budget. It is achieved through a combination of personal financial discipline, market awareness, and aggressive comparison shopping. By focusing on your credit health, choosing the right loan product, and looking past the nominal interest rate to the APR, you can secure a mortgage that serves as a foundation for your financial success rather than a burden on your future.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.