Purchasing a car is one of the most significant financial decisions many individuals make, often second only to buying a home. For most, this purchase involves securing a car loan, and the interest rate attached to that loan can dramatically influence the total cost of the vehicle over its lifetime. Understanding what constitutes a “good” interest rate is crucial for smart financial planning and ensuring you don’t pay more than necessary. It’s not just about the sticker price; it’s about the entire financial package. A seemingly small difference in interest rate can translate into hundreds or even thousands of dollars saved or spent over the term of the loan, directly impacting your monthly budget and overall financial health. Navigating the complexities of car loan interest rates requires a blend of financial literacy, diligent research, and strategic negotiation. This guide will demystify car loan interest rates, helping you identify what a good rate looks like for your specific situation and empowering you to secure the best possible deal.

Understanding Car Loan Interest Rates

Before you can determine what a good interest rate is, it’s essential to understand the mechanics of how these rates work and the various factors that influence them. An interest rate is essentially the cost of borrowing money, expressed as a percentage of the principal loan amount.

What is an Interest Rate?

At its core, an interest rate is the charge for the privilege of borrowing money. When you take out a car loan, the lender charges you interest as compensation for the risk they take and for providing you with immediate funds to purchase your vehicle. This rate is usually presented as an Annual Percentage Rate (APR), which is a more comprehensive measure of the cost of borrowing money. Unlike a nominal interest rate, the APR includes not only the interest rate but also any additional fees or charges associated with the loan, such as administrative fees. This makes APR a more accurate indicator of the total annual cost of the loan and a better metric for comparing offers from different lenders. Understanding the difference between a stated interest rate and the APR is critical; always compare APRs when shopping for a loan.

Factors Influencing Your Interest Rate

Several key variables come into play when a lender determines the interest rate they will offer you. Recognizing these factors allows you to better prepare and potentially improve your standing.

- Credit Score: This is arguably the most significant factor. Lenders use your credit score to assess your creditworthiness – your likelihood of repaying the loan. A higher credit score (typically 700+) indicates a lower risk, translating to lower interest rates. Conversely, a lower score suggests higher risk, leading to higher rates.

- Loan Term: The length of time you have to repay the loan also plays a role. Generally, shorter loan terms (e.g., 36 or 48 months) tend to have lower interest rates because the lender’s risk is contained over a shorter period. Longer terms (e.g., 60 or 72 months) often come with higher rates.

- Down Payment: A larger down payment reduces the amount you need to borrow, thereby lowering the lender’s risk. This can often lead to a more favorable interest rate. It also shows the lender you have a vested interest in the vehicle.

- New vs. Used Car: Loans for new cars typically carry lower interest rates than those for used cars. This is because new cars generally retain their value better in the initial years, are less prone to mechanical issues, and are easier for lenders to repossess and resell if necessary.

- Lender Type: Different types of lenders (banks, credit unions, online lenders, dealership financing) have varying interest rate structures and risk appetites. Credit unions, for example, are member-owned and often offer more competitive rates.

- Market Conditions: Broader economic factors, such as the Federal Reserve’s interest rate policies and the overall economic climate, can influence prevailing car loan rates across the board. When the Fed raises rates, borrowing costs generally increase.

The Role of Your Credit Score

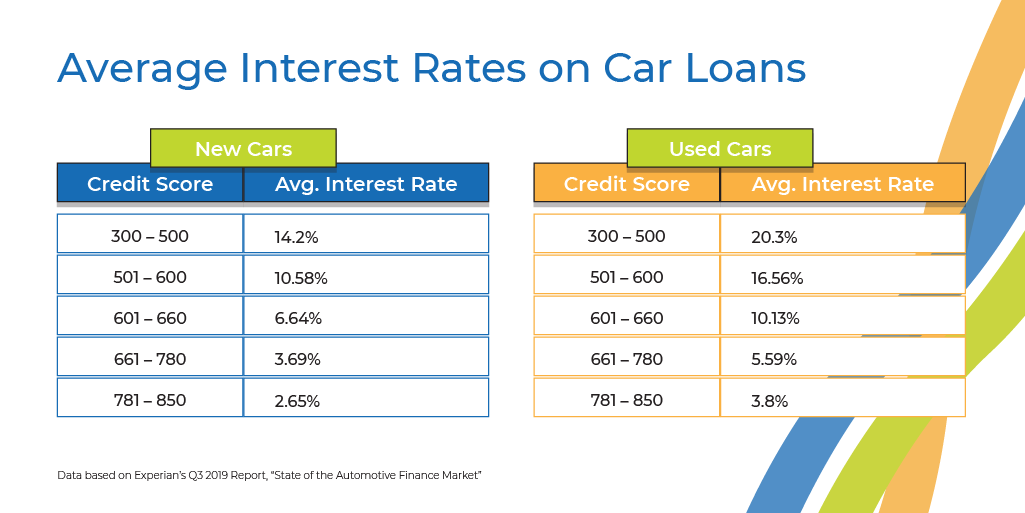

Your credit score acts as a financial report card for lenders. It summarizes your borrowing and repayment history into a three-digit number, most commonly FICO scores ranging from 300 to 850. Lenders use this score to quickly gauge how reliably you’ve managed debt in the past. An “excellent” credit score (typically 780+) signals a very low risk, making you eligible for the lowest available interest rates. A “good” score (670-739) still offers competitive rates, while “fair” (580-669) or “poor” (below 580) scores will likely result in significantly higher interest rates, if a loan is approved at all. It’s not uncommon for someone with excellent credit to secure an APR several percentage points lower than someone with fair credit, leading to thousands of dollars in savings over the life of the loan. Knowing your credit score before you apply for a loan is a powerful tool for negotiation and setting realistic expectations.

Defining “Good” by Credit Tier and Market Conditions

What constitutes a “good” interest rate isn’t a fixed number; it’s dynamic, dependent on both your individual financial profile and the prevailing economic environment. A rate that’s excellent for someone with a poor credit history might be considered high for someone with impeccable credit.

Average Rates by Credit Score Range

To truly understand what a good rate is, it’s helpful to look at general benchmarks based on credit score ranges. These figures are illustrative and subject to change based on market conditions, but they provide a solid starting point for comparison:

- Excellent Credit (780+): Borrowers in this tier often qualify for the lowest rates, which historically can range from 3% to 6% APR for new cars.

- Good Credit (670-739): These borrowers can expect competitive rates, typically falling between 6% to 9% APR.

- Fair Credit (580-669): Individuals in this range will likely see higher rates, often from 9% to 12% APR, reflecting a higher perceived risk.

- Poor Credit (Below 580): Getting a car loan with poor credit is challenging, and rates can be quite high, potentially ranging from 15% to 25%+ APR, if a loan is approved at all. Subprime lenders specialize in this market but at a significant cost.

These ranges underscore the profound impact your credit score has on the affordability of your car loan.

New vs. Used Car Loan Rates

Another critical distinction is between new and used car loan rates. Lenders generally offer lower interest rates for new cars for several reasons: they typically depreciate more predictably, are under warranty, and present lower risks of mechanical failure compared to older vehicles. As a result, new car loan rates often run 1-3 percentage points lower than used car rates for borrowers with similar credit profiles. For example, if a borrower with good credit might get a 6% APR on a new car, they might be offered 8% or 9% on a used car. The age, mileage, and condition of a used car also factor into the rate, with older, higher-mileage vehicles typically commanding higher rates.

Current Market Trends

Car loan interest rates are not static; they fluctuate with broader economic conditions. The Federal Reserve’s monetary policy, specifically its decisions regarding the federal funds rate, has a significant ripple effect on consumer loan rates, including car loans. When the Fed raises rates, the cost of borrowing for banks increases, which in turn leads them to charge higher interest rates to consumers. Conversely, when the Fed lowers rates, car loan APRs tend to decrease. Economic stability, inflation, and the overall demand for credit also play a role. Staying informed about current market trends by checking reputable financial news sources or online rate aggregators can give you an edge in determining if the rates you’re being offered are truly competitive within the current economic landscape.

When a “Good” Rate Isn’t Good Enough

While securing a low interest rate is paramount, it’s important to consider the entire loan package. A low rate on an excessively long loan term might still lead to paying more total interest over time and could result in being “underwater” on your loan (owing more than the car is worth). For instance, a 5% rate over 72 months might seem attractive due to lower monthly payments, but a 6% rate over 48 months could ultimately save you money on total interest paid. Moreover, some loans with seemingly attractive rates might come with hidden fees, prepayment penalties, or other restrictive terms. Always look at the total cost of the loan (principal + total interest paid) and ensure the monthly payments fit comfortably within your budget, even with potential interest rate increases if it’s a variable rate loan.

Strategies to Secure a Better Car Loan Rate

Knowing what a good rate is is only half the battle; the other half is actively working to secure one. Proactive steps can significantly improve your chances of getting the most favorable terms.

Improve Your Credit Score

Since your credit score is the primary determinant of your interest rate, taking steps to improve it is the most impactful strategy.

- Pay Bills On Time: Payment history accounts for 35% of your FICO score. Ensure all your credit card bills, utility payments, and other loan payments are made punctually.

- Reduce Debt: High credit utilization (the amount of credit you’re using compared to your total available credit) can negatively impact your score. Aim to keep credit card balances below 30% of your credit limit.

- Check Your Credit Report for Errors: Annually review your credit reports from all three major bureaus (Equifax, Experian, TransUnion) for inaccuracies. Disputing and correcting errors can quickly boost your score.

- Avoid New Credit Applications: Each new credit inquiry can slightly ding your score. Try to limit new credit applications in the months leading up to a car loan application.

Make a Larger Down Payment

Putting more money down upfront reduces the amount you need to borrow. This not only lowers your monthly payments but also makes you a less risky borrower in the eyes of lenders, often leading to a lower interest rate. A substantial down payment (e.g., 10-20% for new cars, 20%+ for used cars) can be a powerful negotiating tool.

Shorten Your Loan Term

While longer loan terms result in lower monthly payments, they almost always come with higher interest rates and more total interest paid over time. Opting for the shortest loan term you can comfortably afford is usually the most financially savvy decision. For example, choosing a 48-month loan over a 72-month loan could shave a full percentage point or more off your APR, leading to significant savings.

Shop Around for Lenders

Never take the first loan offer you receive, especially if it’s from the dealership. Explore various lending institutions:

- Banks: Both national and local banks offer competitive car loans.

- Credit Unions: Often known for their lower rates and more flexible terms, credit unions can be excellent options, especially if you’re already a member or can easily join one.

- Online Lenders: Companies like Capital One Auto Finance, LightStream, and others specialize in online auto loans and often provide quick pre-approvals and competitive rates.

- Dealership Financing: While convenient, dealership rates can sometimes be higher, though they may also offer special promotional rates for specific models. Always compare their offer against your pre-approved loans.

Get Pre-Approved

Before you even set foot in a dealership, get pre-approved for a loan from an external lender (bank, credit union, online lender). Pre-approval gives you a clear idea of the interest rate you qualify for and the maximum amount you can borrow. This empowers you to negotiate with confidence, treating the dealership’s financing as just another option to beat, rather than your only choice. It also separates the car-buying negotiation from the loan negotiation.

Consider a Co-Signer

If your credit score is less than ideal, having a co-signer with excellent credit can significantly improve your chances of approval and help you secure a lower interest rate. The co-signer essentially guarantees the loan, taking on legal responsibility if you fail to make payments. This reduces the lender’s risk, allowing them to offer a better rate. However, ensure both parties understand the full implications and responsibilities of co-signing.

Beyond the Interest Rate: Other Loan Considerations

While the interest rate is a critical component, it’s not the only factor to evaluate when choosing a car loan. A truly “good” loan package considers the full financial picture.

Total Cost of the Loan

Focusing solely on the monthly payment or the interest rate can be misleading. Always calculate the total cost of the loan, which includes the principal amount borrowed plus all interest paid over the loan’s term. A lower monthly payment achieved through a longer loan term might result in paying significantly more in total interest, making the loan more expensive in the long run. Use online car loan calculators to compare total costs across different loan offers.

Monthly Payment Affordability

Your monthly car payment should fit comfortably within your overall budget without straining your finances. Financial experts often recommend that your total car expenses (payment, insurance, fuel, maintenance) should not exceed 10-20% of your net monthly income. A low interest rate on a loan you can’t afford month-to-month is not a good deal. Prioritize a payment that is sustainable for your financial situation.

Loan Fees and Charges

Be vigilant about any additional fees that might be tacked onto your loan. These can include:

- Origination Fees: A fee charged by the lender for processing the loan.

- Documentation Fees (Doc Fees): Charged by dealerships for handling paperwork, these can sometimes be negotiable.

- Prepayment Penalties: Some lenders charge a fee if you pay off your loan early. While less common with simple interest auto loans, it’s crucial to check.

- Late Payment Fees: Standard fees if you miss a payment.

Ensure you understand all fees before signing the loan agreement.

Dealer Add-ons and Warranties

Dealerships often try to sell various add-ons and extended warranties, which, while sometimes beneficial, can significantly inflate your loan amount and, consequently, the total interest paid. These can include paint protection, fabric protection, VIN etching, and extended service contracts. Carefully evaluate the necessity and value of these products, and remember they are almost always negotiable or can be purchased from third parties at a lower cost. It’s often best to separate these purchases from the car itself to avoid paying interest on them.

Gap Insurance

Guaranteed Asset Protection (GAP) insurance is an optional coverage that pays the difference between what you owe on your car loan and the car’s actual cash value if it’s declared a total loss or stolen. Because new cars depreciate rapidly, it’s easy to owe more than the car is worth in the early years of a loan. If you make a small down payment, have a long loan term, or are buying a rapidly depreciating vehicle, GAP insurance can provide valuable protection. While dealerships offer it, you can often find it for less through your car insurance provider or other financial institutions.

Ultimately, a truly good interest rate for a car loan is one that reflects your strong creditworthiness, aligns with current market conditions, and contributes to an overall loan package that is affordable, transparent, and financially sound for your personal circumstances. By understanding these various components and employing smart financial strategies, you can drive away not just with a new car, but with a financially advantageous deal.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.