Understanding options trading involves grasping several key concepts, and among the most crucial is “delta.” Delta is a fundamental Greeks measure that quantifies an option’s sensitivity to a $1 change in the underlying asset’s price. In simpler terms, it tells you how much the option’s price is expected to move for every dollar the stock, ETF, or other underlying asset moves. For options traders, particularly those seeking to profit from specific market movements or hedge existing positions, understanding what constitutes a “good” delta is paramount. This isn’t a one-size-fits-all answer; a “good” delta is highly dependent on an individual trader’s strategy, risk tolerance, and market outlook.

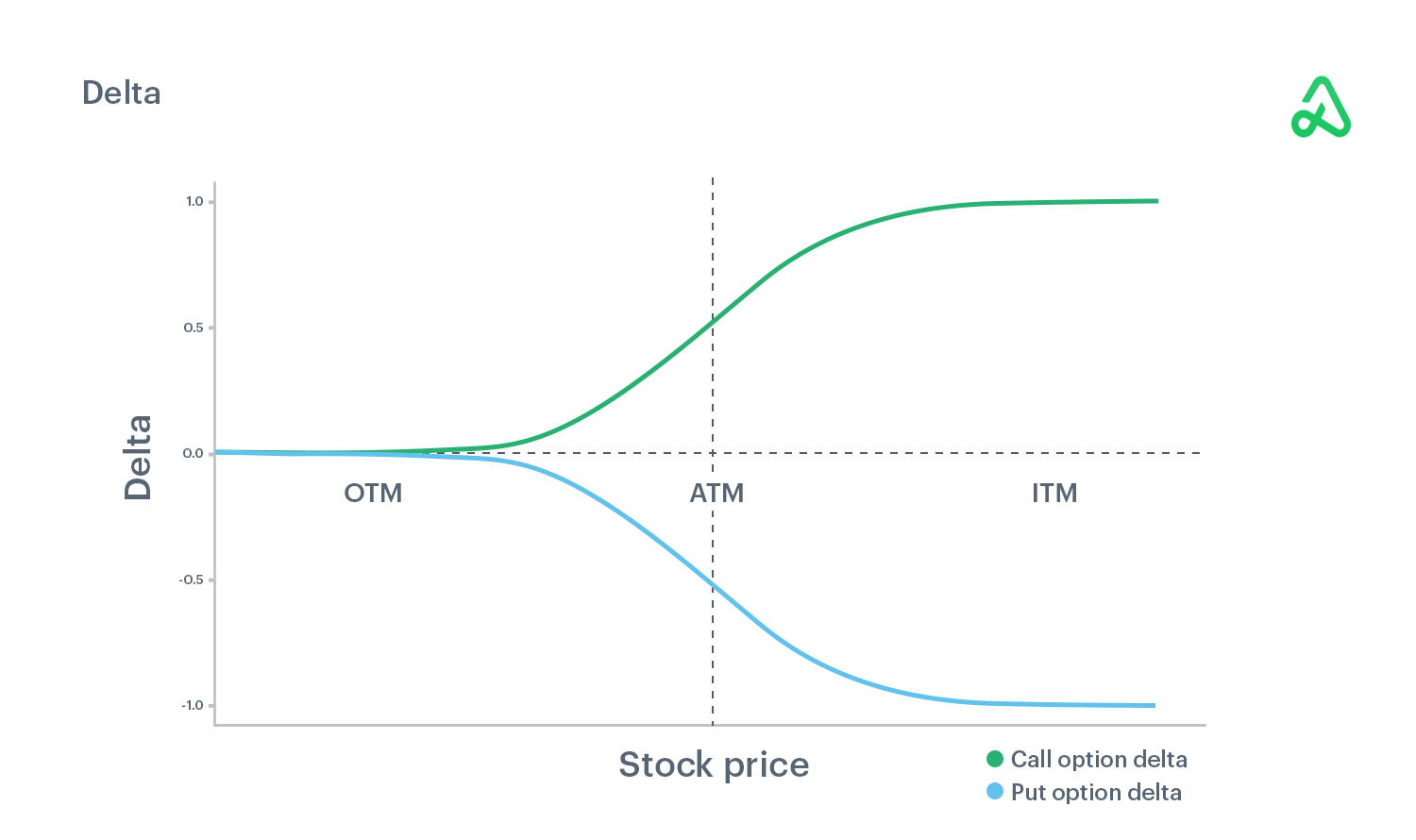

The concept of delta ranges from 0 to 1 for call options and from 0 to -1 for put options. A delta of 0.50 for a call option, for instance, implies that for every $1 increase in the underlying asset’s price, the call option’s premium is expected to rise by $0.50. Conversely, a delta of -0.50 for a put option suggests that for every $1 increase in the underlying asset’s price, the put option’s premium will decrease by $0.50 (and vice-versa for a price decrease). Understanding this relationship is the first step in determining what makes a delta “good” for a particular trading objective.

Delta as a Probability Indicator

One of the most powerful ways to interpret delta is as a proxy for the probability of an option expiring in-the-money (ITM). While not an exact probability, delta provides a strong statistical approximation. For example, an option with a delta of 0.70 is often considered to have approximately a 70% chance of expiring ITM. This probabilistic interpretation is invaluable for traders who want to assess the likelihood of success for their trades.

Deep In-the-Money (ITM) Options: High Delta, High Probability

Options that are deep ITM have deltas close to 1 for calls and -1 for puts. For instance, a call option with a strike price significantly below the current market price of the underlying asset will have a delta nearing 1. Similarly, a put option with a strike price significantly above the current market price will have a delta nearing -1.

Why is a high delta (close to 1 or -1) considered “good” in certain scenarios?

- Predictable Price Action: When a trader is highly confident about the direction and magnitude of the underlying asset’s price movement, a high delta option offers more direct leverage. If a stock is expected to move up by $5, and a call option has a delta of 0.90, the option’s price is expected to increase by roughly $4.50 (0.90 * $5). This provides a more substantial profit potential compared to options with lower deltas, assuming the prediction is correct.

- Hedging: In the context of hedging, a high delta is often sought. For example, an investor holding a large portfolio of stocks might buy put options with high deltas to protect against a market downturn. The high delta ensures that the value of the put options will increase significantly as the stock market falls, effectively offsetting some of the losses in the underlying portfolio.

- Lower Time Decay (Theta): While delta is the primary focus here, it’s worth noting that deep ITM options generally experience less significant erosion from time decay (theta) compared to out-of-the-money (OTM) options. This makes them more resilient over shorter periods if the underlying asset moves slightly against the trader’s position.

However, the “goodness” of a high delta comes with caveats. These options are typically more expensive due to their inherent value. The premium paid will be substantial, meaning a smaller percentage move in the underlying might not be enough to cover the initial investment if the trade doesn’t go as planned. Furthermore, while the probability of expiring ITM is high, the profit potential on a percentage basis might be lower than that of OTM options if the underlying asset makes a very large move.

At-the-Money (ATM) Options: Moderate Delta, Balanced Risk/Reward

Options trading at the money (ATM) have strike prices that are very close to the current market price of the underlying asset. Their deltas typically range from approximately 0.40 to 0.60 for calls and -0.40 to -0.60 for puts. These deltas represent a more balanced approach to risk and reward.

Why is a moderate delta (around 0.50) considered “good” in many trading strategies?

- Sensitivity to Price Movements: A delta of 0.50 offers a good balance between price sensitivity and the cost of the option. For every $1 move in the underlying, the option’s premium is expected to move by $0.50. This provides leverage without requiring an excessively large initial investment.

- Higher Potential for Leverage Amplification: Compared to deep ITM options, ATM options offer greater leverage potential. A smaller percentage move in the underlying asset can translate into a larger percentage gain in the option’s premium because the initial premium is generally lower. If an ATM call option with a delta of 0.50 doubles in price, it implies the underlying asset has moved by a significant amount in the correct direction, a scenario where the percentage gain on the option is much higher than on the underlying.

- Time Decay Trade-offs: ATM options have a higher theta (time decay) than ITM options. This means their value erodes faster as expiration approaches. However, their deltas also tend to increase more rapidly as the underlying price moves favorably, potentially compensating for the time decay. Traders often view this trade-off as acceptable for the increased leverage and lower upfront cost.

- Strategic Flexibility: Many sophisticated options strategies, such as straddles, strangles, and iron condors, utilize ATM options as core components. These strategies aim to profit from volatility or price range expectations, and the 0.50 delta provides the optimal sensitivity for capturing price movements within a defined trading plan.

A “good” delta around 0.50 for ATM options signifies a sweet spot for many traders who are looking for substantial leverage and a reasonable probability of profit without the high cost of deep ITM options or the extreme speculative nature of OTM options.

Out-of-the-Money (OTM) Options: Low Delta, High Speculation & Leverage

Options that are out-of-the-money (OTM) have strike prices that are beyond the current market price of the underlying asset. For call options, this means the strike price is above the current market price, and for put options, it means the strike price is below the current market price. OTM options have deltas close to 0 for calls and close to 0 (negative) for puts. For example, a call option with a delta of 0.20 has a roughly 20% chance of expiring ITM.

Why might a low delta be considered “good” in specific, high-risk/high-reward strategies?

- Cost-Effectiveness: The primary appeal of OTM options is their low premium. This makes them significantly cheaper to purchase compared to ATM or ITM options. This low cost allows traders to control a larger number of contracts or to speculate on significant price movements with a smaller capital outlay.

- Magnified Percentage Returns: While the absolute dollar profit might be less for a small move in the underlying compared to higher delta options, the percentage return on investment can be astronomical if the underlying asset makes a substantial move in the desired direction. A small initial investment in an OTM option can multiply several times over if the underlying experiences a significant rally (for calls) or decline (for puts). This is the essence of highly leveraged trading.

- Betting on Large Moves or Events: Traders might purchase OTM options with low deltas when they anticipate a significant, often event-driven, price movement. This could be in anticipation of major company news, earnings reports, or macroeconomic announcements that are expected to cause substantial volatility. The low delta reflects the lower probability of the event occurring or having the predicted impact.

- “Lottery Ticket” Trades: For some traders, OTM options represent a “lottery ticket” strategy. They are willing to risk a small amount of capital for the chance of a very large payout, understanding that the probability of success is low. In this context, a low delta is not necessarily a flaw but an accurate reflection of the low probability of the option expiring ITM, which is why it is so cheap.

It’s crucial to understand that “good” delta for OTM options is synonymous with a small delta because the objective is not necessarily a direct correlation with small price movements but rather a bet on a large, directional surge. The risk is exceptionally high, as the majority of OTM options expire worthless, leading to a total loss of the premium paid.

Delta and Your Trading Strategy

The determination of what constitutes a “good” delta is intrinsically linked to your specific trading strategy and objectives. There is no universal delta value that is inherently superior; rather, it’s about aligning the delta with your trading plan.

Aggressive Growth Strategies: Targeting High Delta

For traders seeking aggressive growth and who are confident in their directional market predictions, a higher delta might be considered “good.” This often means focusing on ATM or slightly ITM options. These options provide a more direct and amplified exposure to the underlying asset’s price movements. The goal here is to capture significant percentage gains on the option premium for relatively smaller moves in the underlying compared to OTM options. The trade-off is a higher premium paid and potentially less leverage than OTM options on a per-contract basis.

Income Generation Strategies: Moderate Delta for Premiums

Traders focused on generating income, such as those selling covered calls or cash-secured puts, often prefer options with moderate deltas. Selling slightly OTM calls or puts (often with deltas between 0.20 and 0.40) can provide a steady stream of premium income. The delta here is “good” because it offers a reasonable probability of the option expiring worthless, allowing the seller to keep the premium, while still providing some downside protection (for put sellers) or upside potential (for call sellers, up to the strike price). The moderate delta balances the likelihood of retaining the premium with the potential for the option to be assigned.

Hedging and Risk Management: Tailoring Delta for Protection

For hedging purposes, a “good” delta is one that effectively mitigates risk. An investor holding a large stock position might buy OTM or ATM put options to protect against a downturn. The desired delta for these puts would depend on the extent of protection desired and the market outlook. A higher delta put offers more immediate protection as the underlying asset falls, but it will be more expensive. Conversely, a lower delta put is cheaper but provides less immediate protection and relies on a more significant price drop to become profitable. The “good” delta here is the one that provides the desired level of insurance at an acceptable cost.

Volatility Plays: Adapting Delta Based on Expected Volatility

Strategies that aim to profit from changes in implied volatility, such as straddles and strangles, often involve ATM options. The delta for these options typically hovers around 0.50. In this context, a delta around 0.50 is “good” because it maximizes the option’s sensitivity to changes in the underlying price, which is crucial for these strategies to profit from large price swings in either direction. When volatility is expected to increase, traders might even look to slightly OTM options, which have lower deltas but can offer explosive gains if volatility spikes and the underlying asset makes a significant move.

Factors Influencing a “Good” Delta

Beyond the broad strategic categories, several other factors influence what might be considered a “good” delta for a particular options trade.

Time to Expiration

The time remaining until an option expires significantly impacts its delta. As an option approaches expiration, its delta becomes more sensitive to changes in the underlying asset’s price.

- Near-Term Options: For options with only a few days or weeks until expiration, delta becomes a more immediate indicator of directional exposure. A 0.50 delta option expiring in a week will react much more strongly to price movements than a 0.50 delta option expiring in six months. Traders looking for quick profits from short-term price fluctuations might seek higher deltas in near-term options.

- Long-Term Options (LEAPS): Options with longer expirations (LEAPS) have deltas that behave more like stocks. A LEAP call option with a delta of 0.90 will move very closely with the underlying asset, offering less leverage but more predictability. For long-term directional bets or as a substitute for owning the underlying asset, a high delta is often considered “good.”

Implied Volatility

Implied volatility (IV) is the market’s expectation of future price fluctuations. It affects option premiums and, consequently, delta.

- High Implied Volatility: When IV is high, option premiums are inflated. This can make ATM options have deltas closer to 0.50, but the cost of these options is higher. Traders might opt for slightly OTM options with lower deltas, knowing that if volatility decreases, the premium will shrink, but if the underlying moves strongly, the delta can still provide significant profit.

- Low Implied Volatility: When IV is low, option premiums are cheaper. This can make ATM options have deltas closer to 0.50 with a more affordable price. Traders might be more inclined to use higher delta options in this environment, as the cost of admission is lower, allowing for greater leverage.

Underlying Asset Characteristics

The nature of the underlying asset itself can influence what constitutes a “good” delta.

- Highly Volatile Stocks: For stocks that are known for rapid price swings, traders might prefer options with lower deltas to take advantage of potential explosive moves. A 0.20 delta option on a volatile stock might offer a substantial return if the stock moves dramatically.

- Stable, Dividend-Paying Stocks: For more stable stocks, where large price movements are less common, traders might opt for options with higher deltas to gain more direct exposure to modest price appreciation.

Ultimately, a “good” delta for options is a subjective measure, tailored to the individual trader’s objectives, risk appetite, and market analysis. It’s a dynamic metric that needs to be understood in conjunction with other option Greeks and market conditions. By carefully considering your strategy, time horizon, and view on volatility, you can identify the delta that aligns best with your trading goals, transforming it from a mere number into a powerful tool for informed decision-making.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.