Navigating the landscape of car financing can often feel like a complex journey, fraught with jargon and varying figures. At the heart of this process lies the car loan interest rate, a seemingly small percentage that can significantly impact the overall cost of your vehicle. Understanding what constitutes a “good” car loan interest rate is not merely about finding the lowest number; it’s about comprehending the factors that influence it, recognizing market trends, and employing strategies to secure the most favorable terms for your financial situation. For many, a car is the second-largest purchase they’ll make after a home, making the financing terms, particularly the interest rate, a critical component of responsible financial planning. A savvy borrower doesn’t just look at the monthly payment; they delve into the total cost of the loan, empowered by knowledge to make an informed decision.

Understanding the Dynamics of Car Loan Interest Rates

Before we can define “good,” it’s essential to grasp what an interest rate represents in the context of a car loan and why its impact is so profound. An interest rate is essentially the cost of borrowing money, expressed as a percentage of the principal amount. When you take out a car loan, the lender provides you with funds to purchase the vehicle, and in return, you agree to repay that principal amount plus interest over a predetermined period.

What an Interest Rate Truly Means for Your Loan

The interest rate determines how much extra you’ll pay on top of the car’s sticker price. A higher interest rate means a greater total cost over the life of the loan, translating into higher monthly payments or a longer repayment period. Conversely, a lower interest rate reduces the cost of borrowing, making the car more affordable in the long run. It’s not just about the monthly budget; it’s about optimizing your capital and ensuring you’re not overpaying for the convenience of financing. This often overlooked detail is where many borrowers can lose thousands of dollars unnecessarily.

Why Interest Rates are a Critical Financial Lever

Interest rates are a critical financial lever because they reflect risk and opportunity cost for the lender. For you, the borrower, they directly influence your debt-to-income ratio, your disposable income, and your overall financial health. A high-interest car loan can strain your budget, potentially delaying other financial goals like saving for a home or retirement. Furthermore, the interest rate can dictate the type of car you can realistically afford. A seemingly small difference of one or two percentage points can accumulate into substantial savings or additional costs over a typical five-year loan term. This makes rate comparison and negotiation one of the most impactful steps in the car buying process.

Key Factors Influencing Your Car Loan Interest Rate

The interest rate you’re offered isn’t arbitrary; it’s a carefully calculated figure based on a myriad of individual and market-driven factors. Lenders assess risk, market conditions, and the specifics of the loan to determine what rate they are willing to offer. Understanding these components can empower you to improve your standing as a borrower.

Your Credit Score: The Primary Determinant

Without a doubt, your credit score is the most significant factor influencing your car loan interest rate. Lenders use this three-digit number to gauge your creditworthiness and your likelihood of repaying the loan. A higher credit score (typically FICO scores above 700-720) indicates a lower risk to the lender, resulting in more favorable interest rates. Conversely, a lower credit score signals higher risk, leading to higher interest rates to compensate the lender for that perceived risk. Maintaining a strong credit history, making payments on time, and managing existing debt responsibly are paramount.

Loan Term and Loan Amount: The Time and Size Elements

The length of your loan term also plays a crucial role. Shorter loan terms (e.g., 36 or 48 months) often come with lower interest rates because the lender’s risk exposure is reduced. However, shorter terms mean higher monthly payments. Longer loan terms (e.g., 60 or 72 months or even 84 months) typically have higher interest rates, but they offer lower monthly payments, making them seem more affordable upfront. While a longer term might reduce your monthly burden, it significantly increases the total interest paid over the life of the loan. The loan amount also matters; larger loans inherently carry more risk for lenders, which can sometimes translate into slightly different rate structures.

Down Payment and Trade-In Value: Reducing Lender Risk

The size of your down payment directly impacts the amount you need to borrow. A larger down payment reduces the principal loan amount, which lowers the lender’s risk and can often lead to a better interest rate. Similarly, trading in an old vehicle with equity can serve as a de facto down payment, achieving the same beneficial effect. Lenders prefer borrowers who have a significant financial stake in the vehicle, as it signals commitment and reduces the chance of default.

Lender Type and Market Conditions: Where and When You Borrow

Different lenders offer different rates. Banks, credit unions, and online lenders each have unique underwriting criteria and competitive strategies. Credit unions, being member-owned, often offer some of the most competitive rates. Market conditions, specifically the prime rate set by the Federal Reserve, also influence car loan rates. When the Fed raises interest rates, car loan rates tend to follow suit. Conversely, in a low-interest rate environment, borrowers can typically secure more attractive deals. Shopping around and getting multiple pre-approvals is crucial.

Vehicle Age and Type: The Asset Itself

The vehicle you choose can also impact your rate. New cars generally qualify for lower interest rates than used cars because new cars are seen as less risky assets; they depreciate slower initially, have warranties, and their value is more predictable. Used cars, especially older models, carry higher risk due to potential mechanical issues and faster depreciation, leading to higher interest rates. Luxury or specialized vehicles might also have different rate structures compared to mass-market models.

What Constitutes a “Good” Interest Rate?

Defining a “good” interest rate is relative, as it depends heavily on the factors discussed above and the prevailing economic climate. However, we can establish benchmarks and general expectations.

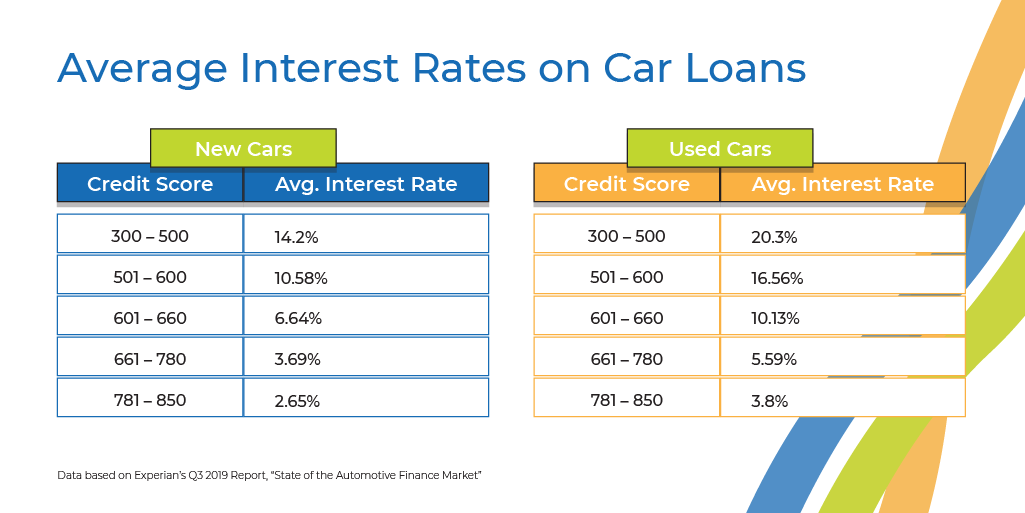

Average Car Loan Rates by Credit Score Tier

In general, borrowers with excellent credit (780+) can expect to see the lowest rates, often in the single digits, potentially as low as 3-5% for new cars in a favorable market. Those with good credit (670-739) might see rates in the 5-8% range, while fair credit (580-669) could lead to rates between 8-12% or even higher. Subprime borrowers (below 580) often face rates upwards of 15-20% or more, reflecting the significant risk lenders perceive. These are broad averages, and actual rates fluctuate.

Comparing New vs. Used Car Loan Rates

As mentioned, new car loan rates are typically lower than used car loan rates. For instance, if a borrower with excellent credit gets 3.5% on a new car, they might get 4.5% or 5% on a used car. The gap widens significantly for borrowers with lower credit scores, where a used car loan might carry an interest rate several percentage points higher than a new car loan for the same borrower. This disparity reflects the depreciation curve and perceived reliability of the asset.

Benchmarking Against Current Market Trends

To truly know if you’re getting a good rate, you must benchmark it against current market trends. Resources like the Federal Reserve, reputable financial news outlets, and financial aggregators frequently publish average car loan rates. If the market average for someone with your credit profile is 6% and you’re offered 5%, that’s generally excellent. If you’re offered 7% or 8% in the same scenario, it’s a sign to shop around more aggressively or re-evaluate your credit standing.

Strategies to Secure a Favorable Rate

Even if your credit isn’t perfect, there are proactive steps you can take to improve your chances of securing a more favorable interest rate on your car loan.

Boost Your Credit Score Before Applying

If you have time before your purchase, focus on improving your credit score. This involves paying all bills on time, reducing credit card balances, and avoiding new credit inquiries. Even a small increase in your score can move you into a better rate tier, saving you hundreds or thousands over the life of the loan. Dispute any errors on your credit report immediately.

Shop Around and Compare Multiple Lender Offers

This is perhaps the most impactful strategy. Don’t simply accept the first offer from the dealership. Apply for pre-approvals from multiple banks, credit unions, and online lenders. Aim for at least 3-5 different offers. Because multiple hard inquiries for the same type of loan within a short period (typically 14-45 days, depending on the scoring model) are usually treated as a single inquiry, you can shop around without damaging your credit score significantly. Having pre-approved offers in hand gives you leverage when negotiating with a dealership’s finance department.

Make a Larger Down Payment

As discussed, a larger down payment reduces the loan amount and the lender’s risk. Aim for at least 20% if possible, especially for new cars, to help offset depreciation and potentially qualify for a lower rate. For used cars, a substantial down payment can be even more beneficial due to their faster depreciation.

Opt for a Shorter Loan Term (If Feasible)

While higher monthly payments can be daunting, a shorter loan term almost invariably comes with a lower interest rate and significantly reduces the total interest paid. If your budget allows, choosing a 36- or 48-month loan instead of a 60- or 72-month loan can result in substantial savings. Always calculate the total cost of the loan for different terms, not just the monthly payment.

Consider Refinancing Your Existing Loan

If you’ve already purchased a car and your credit score has improved, or if interest rates have dropped since you took out your original loan, consider refinancing. Refinancing allows you to replace your current car loan with a new one, potentially at a lower interest rate, reducing your monthly payments or the total cost of the loan. This is a particularly effective strategy for those who bought a car when their credit wasn’t optimal.

Avoiding Common Pitfalls

Even with all the knowledge, some common mistakes can derail your efforts to secure a good rate.

Understanding the Total Cost of the Loan, Not Just Monthly Payments

Dealers often focus on monthly payments to make a car seem more affordable. While important for budgeting, it can obscure the true cost. A lower monthly payment achieved by extending the loan term might lead to a significantly higher total interest paid. Always ask for the total cost of the loan, including all interest and fees.

Beware of Dealer Markups on Interest Rates

Dealership finance departments often act as intermediaries for various lenders and can mark up the interest rate they offer you from what the lender initially approved. This “dealer reserve” is profit for the dealership. By having your own pre-approval from another lender, you can identify and negotiate against these markups, ensuring you get the rate you truly qualify for.

The Impact of Add-ons on Your Loan

Be cautious of expensive add-ons like extended warranties, GAP insurance, or anti-theft devices bundled into your loan without full transparency. While some might be worthwhile, others inflate your loan amount, meaning you pay interest on these additional products, further increasing your total cost. Evaluate each add-on independently and decide if it’s truly necessary and offers good value.

In conclusion, securing a “good” car loan interest rate is a multifaceted endeavor that rewards an informed and proactive approach. It requires understanding your credit profile, diligent research into market rates, strategic shopping for lenders, and careful negotiation. By taking control of these variables, you can drive away not just with the car of your dreams, but with a financing package that genuinely serves your financial well-being.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.