The question “What is a good annual salary?” is perhaps one of the most subjective inquiries in the world of personal finance. To a recent college graduate, $60,000 might feel like a fortune; to a mid-career professional in a metropolitan hub with a family of four, $150,000 might feel like just enough to get by.

Determining what constitutes a “good” income requires moving beyond a single, arbitrary number. It involves a deep dive into the cost of living, personal financial goals, debt-to-income ratios, and the lifestyle one wishes to lead. In this guide, we will explore the multifaceted nature of annual earnings, how to benchmark your income against economic realities, and how to optimize your financial life regardless of the number on your paycheck.

Defining the “Good” Salary: Factors That Influence Your Number

A salary does not exist in a vacuum. Its value is entirely dependent on the environment in which it is spent and the obligations it must fulfill. To understand if your salary is “good,” you must first audit the variables that dictate your purchasing power.

Geographic Location and Cost of Living

The most significant factor in determining the value of your salary is where you choose to live. Economic historians and financial planners often discuss “purchasing power parity.” For instance, a $100,000 salary in San Francisco, California, has roughly the same purchasing power as a $45,000 salary in San Antonio, Texas.

Housing is typically the largest expense for any household. In “high-cost-of-living” (HCOL) areas, rent or mortgage payments can easily consume 40% to 50% of a person’s gross income. Conversely, in “low-cost-of-living” (LCOL) areas, that same individual might spend only 20%. A “good” salary is one that allows you to keep your housing costs below the recommended 30% of your gross income while still living in a safe, accessible neighborhood.

Lifestyle Expectations and Household Size

A single individual living a minimalist lifestyle will have a vastly different definition of a good salary than a primary breadwinner supporting a spouse and three children. When calculating your target income, you must account for the “per capita” needs of your household. Costs such as childcare, education, health insurance premiums, and groceries scale significantly with family size. Furthermore, personal values play a role; if your lifestyle includes frequent international travel, luxury vehicles, or high-end dining, your “good” salary threshold will naturally be higher than someone who prioritizes domestic hobbies and home-cooked meals.

Debt Obligations and Financial Goals

Your “net” freedom is often more important than your “gross” income. If you earn $120,000 a year but carry $200,000 in high-interest student loans and significant credit card debt, your effective income is much lower. A good annual salary is one that provides enough “margin”—the gap between what you earn and what you spend—to aggressively pay down debt while simultaneously building an emergency fund. Without this margin, even a high salary can lead to “lifestyle creep” and financial fragility.

Measuring Your Salary Against National and Regional Benchmarks

While personal context is paramount, it is helpful to look at economic data to see where you stand relative to the rest of the population. Benchmarking allows you to understand your market value and the broader economic landscape.

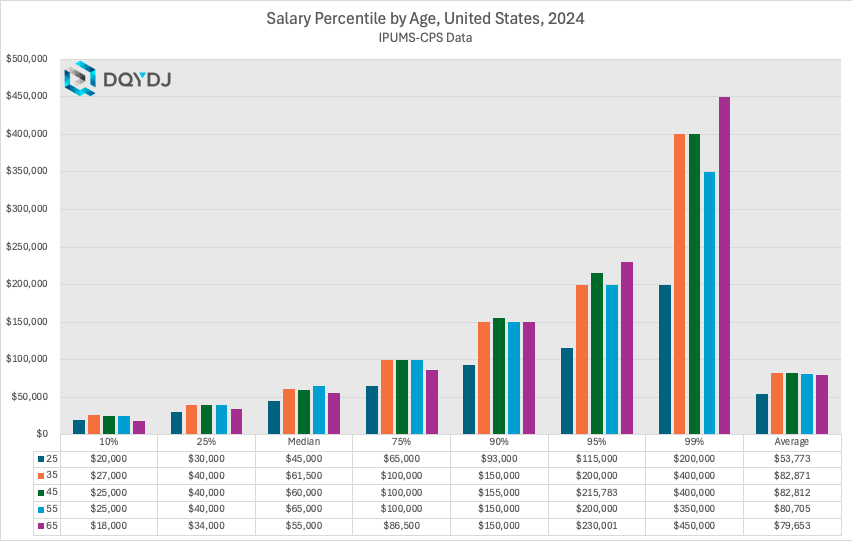

Understanding Median vs. Average Income

When researching salaries, it is crucial to look at the median income rather than the average. Averages can be skewed by ultra-high earners (the top 1%), whereas the median represents the exact middle of the data set. In the United States, the median household income fluctuates around $75,000 to $80,000.

If your individual salary is above the median for your specific region and career stage, you are statistically doing “well.” However, professional benchmarks should also be considered. Using tools like the Bureau of Labor Statistics (BLS) or industry-specific financial reports can help you determine if you are being paid fairly for your expertise and years of experience.

The 50/30/20 Rule as a Litmus Test

A classic personal finance metric to determine if your salary is sufficient is the 50/30/20 rule. This framework suggests that:

- 50% of your income should go to Needs (housing, utilities, groceries, transportation).

- 30% should go to Wants (entertainment, dining out, hobbies).

- 20% should go to Savings and Debt Repayment.

If your annual salary does not allow you to cover your basic needs within 50% of your take-home pay, it may not be a “good” salary for your current environment. If you are consistently dipping into the 20% savings category just to pay for rent, it is a clear indicator that either your income needs to increase or your expenses need a radical overhaul.

The “Happiness Plateau” Research

Psychologists and economists have long studied the link between income and emotional well-being. A famous study from Princeton University once suggested that emotional well-being peaks at an annual income of approximately $75,000 (now adjusted for inflation to roughly $100,000–$110,000).

The theory is that up to this point, every extra dollar significantly reduces stress by providing security, healthcare, and comfort. Beyond this threshold, the “marginal utility” of wealth decreases; more money doesn’t necessarily make you happier, though it may improve your “life evaluation” or sense of achievement. A good salary, therefore, can be defined as the amount that removes financial anxiety from your daily life.

Beyond the Base Pay: Total Compensation and Wealth Building

In the modern economy, looking only at your annual base salary is a mistake. Total compensation—the sum of your salary, benefits, and incentives—is the true measure of your financial intake.

Evaluating Benefits and Bonuses

A $90,000 salary with a 15% annual bonus and fully covered health insurance premiums is often superior to a $110,000 salary with no bonus and a high-deductible health plan. When evaluating your income, you must assign a dollar value to your benefits package. This includes:

- Paid Time Off (PTO): How much is a week of your time worth?

- Health and Wellness: Lower premiums and HSA contributions are direct additions to your net worth.

- Stock Options or Equity: In many corporate sectors, Restricted Stock Units (RSUs) can double your actual take-home pay over a vesting period.

Retirement Contributions and Employer Matching

One of the most overlooked aspects of a “good” salary is the employer’s 401(k) or pension match. If a company matches 6% of your salary, that is essentially a 6% raise that is immediately invested for your future. A salary that seems lower on paper but comes with a robust retirement contribution plan can actually lead to greater long-term wealth than a higher base salary with no retirement support.

Tax Implications and Net vs. Gross Income

It is easy to get caught up in “gross” figures, but you live on your “net” (take-home) pay. High earners in states like New York or California may see nearly 40% of their income disappear to federal, state, and local taxes. Conversely, residents in states with no income tax, like Florida or Texas, keep significantly more of their earnings. A “good” salary is one that remains substantial even after the tax man takes his cut. Understanding tax brackets and utilizing tax-advantaged accounts (like IRAs or 401ks) is essential for keeping more of what you earn.

Strategies to Increase Your Earning Potential

If you have concluded that your current annual salary is not “good” enough to meet your goals, the focus must shift from budgeting to income expansion. Personal finance is a two-sided equation: expenses and income.

Mastering the Art of Negotiation

Many professionals are underpaid simply because they never asked for more. Negotiation is a critical financial skill. To negotiate effectively, you must gather data on market rates for your role, document your specific contributions to the company’s bottom line, and be prepared to walk away or ask for non-monetary benefits if the budget is tight. A 5% to 10% increase through negotiation can compound into hundreds of thousands of dollars over a career.

Upskilling and Strategic Career Pivoting

In a rapidly changing economy, your “human capital” is your greatest asset. Investing in certifications, advanced degrees, or learning high-demand skills (such as financial analysis, project management, or specialized technical skills) can move you into a different income bracket entirely. Sometimes, a “good” salary isn’t possible in your current industry; in such cases, a strategic pivot to a higher-margin sector is the most logical financial move.

Developing Multiple Streams of Income

The wealthiest individuals rarely rely on a single annual salary. To truly achieve financial independence, consider diversifying your income. This could include:

- Side Hustles: Consulting or freelance work in your field of expertise.

- Investing: Generating passive income through dividends, real estate, or index funds.

- Business Ventures: Starting a small-scale online business or e-commerce store.

By building multiple streams, you reduce the pressure on your primary salary to do all the heavy lifting for your financial future.

Conclusion: Finding Your Personal “Enough”

Ultimately, a “good” annual salary is one that aligns with your values and facilitates your long-term financial peace. It is an income that allows you to live comfortably today while systematically building the wealth required for tomorrow. Whether that number is $70,000 or $270,000 depends on your geography, your family, and your ambitions.

The goal of personal finance is not merely to accumulate the highest possible number, but to ensure that the number you do earn is working effectively for you. By understanding the factors of cost of living, measuring yourself against the right benchmarks, and maximizing your total compensation, you can turn any “good” salary into a foundation for a wealthy and fulfilling life.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.