For entrepreneurs and established corporations alike, the state of Texas offers a unique economic landscape. Renowned for its lack of a personal income tax and its “open for business” reputation, Texas is a magnet for relocation and startup activity. However, business owners must navigate a specific fiscal obligation known as the Texas Franchise Tax. Unlike standard corporate income taxes found in other states, the Texas Franchise Tax operates on a “margin” basis, making it one of the most misunderstood aspects of business finance in the Lone Star State.

Understanding this tax is not merely about compliance; it is a critical component of financial planning and cash flow management. Whether you are a solo practitioner or the CFO of a multi-state enterprise, grasping the nuances of who pays, how much is owed, and what exemptions exist can significantly impact your bottom line.

Understanding the Texas Franchise Tax Landscape

The Texas Franchise Tax is essentially a privilege tax imposed on each taxable entity formed or organized in Texas or doing business in the state. It is the price of admission for the legal protection and economic infrastructure provided by the state government. While many people mistake it for an income tax, it is technically calculated on a business’s “margin.”

Who is Required to File?

In Texas, the net is cast wide. The tax applies to a vast majority of business structures, including corporations, limited liability companies (LLCs), partnerships (limited, limited liability, and general), business trusts, and professional associations. Even if an entity is formed in another state, if it has sufficient “nexus” (a legal presence) in Texas, it is subject to the filing requirement.

Notably, sole proprietorships and certain general partnerships (those owned directly by natural persons) are generally exempt. However, the moment a business incorporates or forms an LLC to protect personal assets, it enters the jurisdiction of the franchise tax.

The Concept of Nexus and Physical Presence

Historically, “nexus” was defined by physical presence—having an office, warehouse, or employees in the state. However, in the modern digital economy, Texas has expanded its reach. Economic nexus rules now dictate that any entity with gross receipts from Texas sources totaling $500,000 or more in a reporting period is subject to the tax, regardless of whether they have a physical footprint in the state. This makes it imperative for online retailers and service providers across the country to monitor their Texas-sourced income closely.

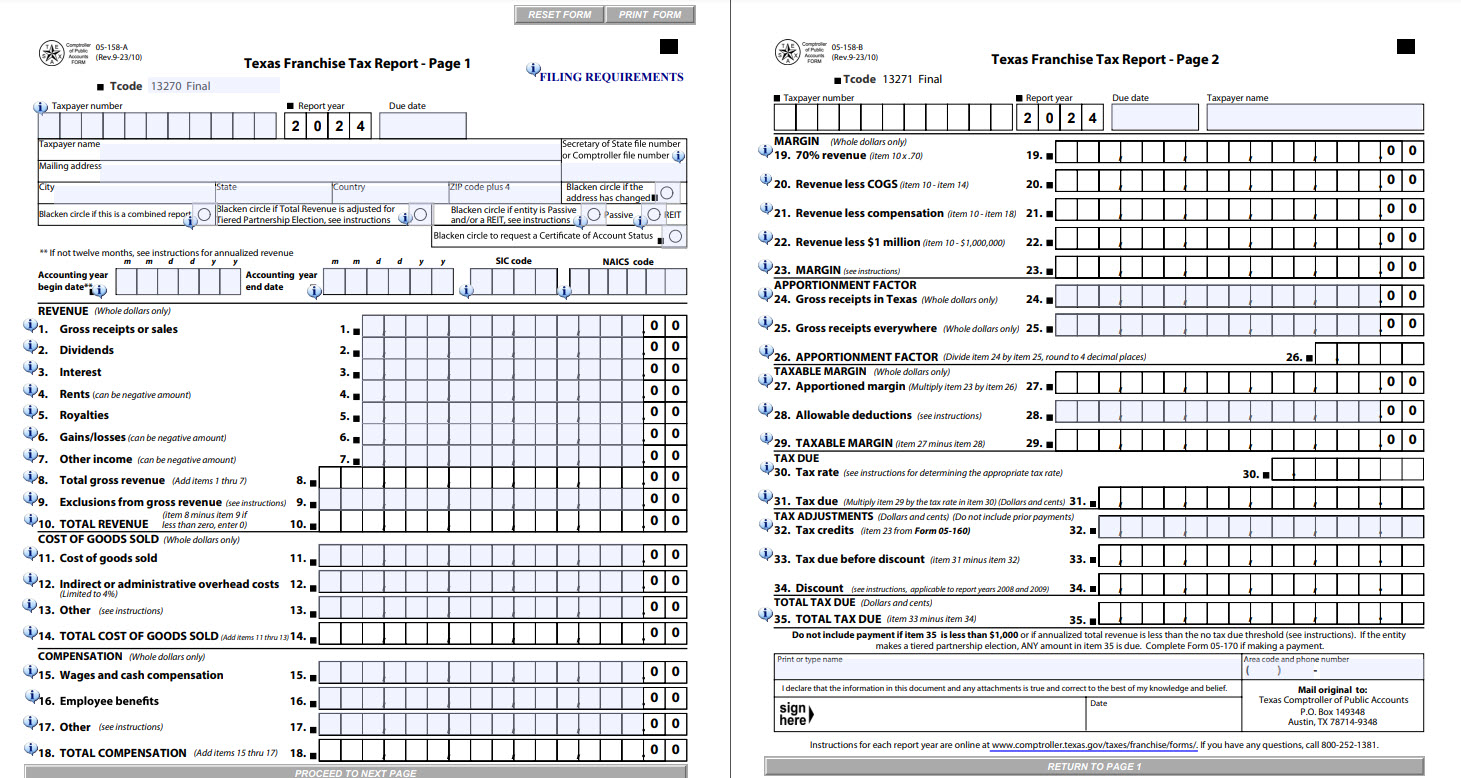

Calculating the Margin: The Four Ways to Determine Tax Liability

The Texas Franchise Tax is often referred to as a “margin tax” because the tax base is the “taxable margin.” Business owners are not stuck with a single rigid formula; instead, the state provides four different methods to calculate this margin. A business is allowed to choose the method that results in the lowest tax liability.

Total Revenue minus Cost of Goods Sold (COGS)

This is often the most beneficial method for businesses involved in manufacturing, retail, or wholesale. By subtracting the direct costs of producing or purchasing the products they sell, these businesses can significantly reduce their taxable base. However, Texas has very specific rules about what qualifies as COGS. It generally includes direct labor and materials but excludes many administrative costs and distribution expenses that might be deductible on federal returns.

Total Revenue minus Compensation

For service-based industries—such as law firms, accounting practices, or consulting agencies—COGS is often negligible. In these cases, the “Compensation” deduction is usually more advantageous. This allow businesses to deduct wages, salaries, and even the cost of benefits (like health insurance and retirement contributions) paid to employees and officers. There is, however, a cap on the amount of compensation that can be deducted per person, which is adjusted biennially for inflation.

70% of Total Revenue

If a business has high overhead that doesn’t fit neatly into COGS or Compensation, they can opt for a flat deduction. This method simply takes 70% of the total revenue as the taxable margin. While rarely the most advantageous for high-margin businesses, it provides a “ceiling” for tax liability and simplifies the calculation process for businesses with complex expense structures.

Total Revenue minus $1 Million (EZ Computation)

For smaller businesses that exceed the no-tax-due threshold but still want to avoid complex accounting, the “EZ Computation” is available. To qualify, an entity must have a total revenue of $20 million or less. Under this method, the tax is calculated by applying a reduced tax rate to the apportioned total revenue, without the need to calculate specific deductions for COGS or compensation.

Tax Rates and Thresholds for the Modern Era

One of the most significant aspects of the Texas Franchise Tax is how the rates differ based on the nature of the business. The state distinguishes between “retail/wholesale” and all other types of businesses.

Retail vs. Service Industries

As of the current reporting cycles, the tax rate for entities primarily engaged in retail or wholesale trade is 0.375%. For all other entities—which includes most service providers, manufacturers, and professional firms—the rate is 0.75%. To qualify for the lower retail/wholesale rate, a business must derive more than 50% of its revenue from the sale of finished goods and must not provide significant “incidental” services.

The No-Tax-Due Threshold

The most important recent development in Texas business finance is the significant increase in the “No-Tax-Due” threshold. Thanks to legislative changes in 2023 (Senate Bill 3), the threshold for the 2024 and 2025 reporting years was raised to $2.47 million.

This means that if a business’s total revenue is $2.47 million or less, they owe zero franchise tax. This is a massive boon for small and medium-sized enterprises (SMEs). However, a critical financial trap exists here: Even if you owe $0, you are still required to file a “No Tax Due Report.” Failure to file this informational return can lead to penalties and the loss of the entity’s “Good Standing” status with the Secretary of State.

Filing Requirements and Key Deadlines

Managing the administrative side of the Texas Franchise Tax is just as vital as the calculation itself. The tax year in Texas generally follows the calendar year, and the reporting period is based on the previous year’s financial activity.

The Public Information Report (PIR)

Every entity that files a franchise tax report must also file a Public Information Report (PIR). This document lists the names and addresses of the company’s officers, directors, or managers. If the entity is a limited partnership, it must file an Ownership Information Report (OIR) instead. This transparency is a requirement for maintaining the right to do business in the state. Failing to file the PIR is a common mistake that leads to the administrative forfeiture of a business’s corporate charter.

Late Penalties and Interest

The deadline for filing and payment is May 15th of each year. If May 15th falls on a weekend or holiday, the deadline moves to the next business day. The penalties for missing this deadline are steep: an automatic $50 penalty is applied to every late report, even if no tax is due. If tax is owed, a 5% penalty is added immediately, which increases to 10% if the tax is not paid within 30 days of the due date. Interest also begins to accrue on the unpaid balance, creating a compounding financial burden.

Strategic Tax Planning for Texas Businesses

In the realm of business finance, the Texas Franchise Tax should not be viewed as a static expense. Through proactive strategy, businesses can optimize their filings and ensure they are not overpaying.

Evaluating Your Business Structure

Because the franchise tax treats different entities differently, the choice of entity is paramount. For example, a general partnership composed entirely of natural persons is exempt from the tax, whereas an LLC is not. For a growing business, the trade-off between the liability protection of an LLC and the tax savings of a general partnership must be carefully weighed. Furthermore, as a business grows toward the $2.47 million threshold, tax-efficient revenue recognition becomes a vital conversation with a financial advisor.

Deductions and Credits

Texas offers various credits that can be applied against the franchise tax. The most notable are credits for Research and Development (R&D). If your business is investing in innovation, technology, or new manufacturing processes within the state, you may be eligible to offset a significant portion of your tax liability. Additionally, certain “clean energy” projects or businesses operating in “enterprise zones” (economically distressed areas) may qualify for specific incentives.

Navigating the Texas Franchise Tax requires a blend of rigorous accounting and strategic foresight. While the “No-Tax-Due” threshold provides relief for many, the complexities of the four-margin calculation and the strict filing requirements mean that business owners must remain vigilant. By integrating franchise tax planning into your broader financial strategy, you ensure that your business remains compliant, protected, and positioned for long-term growth in the competitive Texas market.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.