Navigating the complexities of the United States tax system requires more than just an annual look at your income and expenses. Because the U.S. operates on a “pay-as-you-go” system, the timing of your tax payments is just as critical as the amount you pay. When there is a disconnect between when income is earned and when the IRS receives its share, taxpayers often encounter IRS Form 2210.

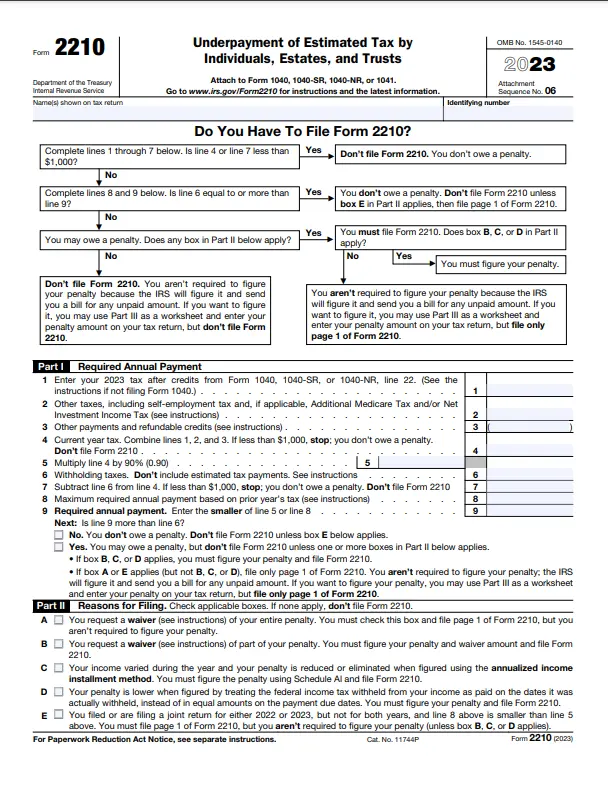

Form 2210, officially titled “Underpayment of Estimated Tax by Individuals, Estates, and Trusts,” is a document used to calculate whether you owe a penalty for not paying enough tax throughout the year. For investors, freelancers, and high-net-worth individuals, understanding this form is a vital component of proactive financial management.

Understanding the Purpose and Mechanics of Form 2210

The core philosophy of the Internal Revenue Service is that taxes should be paid as income is earned or received during the year. For most employees, this happens automatically through payroll withholding. However, for those with diverse income streams—such as dividends, capital gains, or self-employment earnings—the responsibility falls on the individual to make quarterly estimated payments.

The “Pay-As-You-Go” Financial Structure

The U.S. tax system is designed to ensure a steady stream of revenue for the government. If a taxpayer waits until April 15th to pay their entire tax bill for the previous year, they have effectively received an interest-free loan from the government. Form 2210 is the mechanism the IRS uses to “charge interest” on that deferred payment in the form of an underpayment penalty.

Who is Required to Use Form 2210?

In many cases, the IRS will calculate your underpayment penalty for you and send a bill, meaning you don’t necessarily have to file Form 2210 yourself. However, you are legally required to file the form if you are requesting a waiver of the penalty or if you are using the “Annualized Income Installment Method” to lower your penalty. From a financial planning perspective, filing the form yourself is often the best way to ensure you aren’t overpaying on penalties due to seasonal fluctuations in your income.

The $1,000 Threshold

Generally, the IRS will not impose an underpayment penalty if the total tax due, after subtracting withholding and credits, is less than $1,000. This buffer protects small-scale earners and those who made minor errors in their withholding calculations. Once you cross this threshold, Form 2210 becomes a necessary part of your financial reporting.

Key Thresholds and the Safe Harbor Rules

To avoid the sting of underpayment penalties, savvy taxpayers look toward “Safe Harbor” rules. These are specific benchmarks established by the IRS that, if met, exempt a taxpayer from penalties regardless of how much they actually owe at the end of the year. Understanding these thresholds is a cornerstone of effective personal finance and cash flow management.

The 90% and 100% Rules

Most taxpayers can avoid a penalty if they pay at least 90% of the tax shown on their current year’s return through withholding or timely estimated payments. Alternatively, they can satisfy the Safe Harbor by paying 100% of the tax shown on their return from the previous year (provided the previous year covered a full 12-month period). This “100% of last year” rule is particularly popular among investors because it provides a fixed, known number to aim for, regardless of how much their income might grow in the current year.

Special Considerations for High-Income Earners

If your adjusted gross income (AGI) for the previous year exceeded $150,000 (or $75,000 if married filing separately), the Safe Harbor threshold increases. Instead of paying 100% of your prior year’s tax, you must pay 110% to avoid the underpayment penalty. Failure to account for this 10% jump is one of the most common reasons high-earning professionals find themselves filling out Form 2210.

Exceptions for Farmers and Fishermen

The IRS recognizes that certain industries have highly volatile, seasonal cash flows. Farmers and fishermen are held to a different standard; they generally only need to pay 66 and 2/3% of their current year’s tax to avoid a penalty, reflecting the unique financial risks and timing of their respective trades.

Calculating the Penalty: The Mechanics of Form 2210

Calculating the penalty is not a straightforward interest calculation. Because the penalty is tied to when the money was due, Form 2210 breaks the year down into four distinct payment periods.

The Short Method vs. The Regular Method

Form 2210 offers a “Short Method” for taxpayers who made no estimated payments (meaning their only tax payments came from withholding) or those who made four equal estimated payments on time. However, many people with complex financial lives find that the “Regular Method” is necessary. The Regular Method is more granular, looking at the exact dates payments were made to determine the duration of the underpayment.

The Annualized Income Installment Method

This is perhaps the most powerful section of Form 2210 for those with fluctuating income. If you earned the bulk of your money in the fourth quarter (for example, through a year-end bonus or a large stock sale in December), paying equal quarterly installments would be unfair.

The Annualized Income Installment Method allows you to calculate your tax liability based on what you actually earned during each specific quarter. By “annualizing” your income at each interval, you can prove to the IRS that your underpayment in the first or second quarter was justified because you hadn’t actually earned the money yet. This can significantly reduce or even eliminate the penalty.

Penalty Rates and Interest

The penalty is essentially an interest charge on the amount you underpaid for the period it remained unpaid. The rate is determined quarterly and is based on the federal short-term rate plus three percentage points. From a wealth-management perspective, these penalties represent a “guaranteed loss” on your capital, making it much more efficient to pay the tax on time than to pay the penalty later.

Strategic Financial Planning to Avoid Form 2210

The ultimate goal for any taxpayer should be to manage their finances so that Form 2210 becomes unnecessary. This requires a proactive approach to cash flow and a deep understanding of one’s tax liabilities throughout the year.

Adjusting Withholding via Form W-4

For those who are primarily employees but have side income, the simplest way to avoid an underpayment penalty is to increase withholding on their W-4. By asking your employer to withhold an additional dollar amount from each paycheck, you can cover the tax liability of your investments or side hustles without ever having to write a check for estimated taxes. Since withholding is treated by the IRS as being paid evenly throughout the year—regardless of when it actually happened—this is a powerful tool for catching up if you realize mid-year that you are underpaid.

Mastering Quarterly Estimated Payments

For the self-employed or those living off investment income, quarterly estimated payments are a non-negotiable part of financial life. These payments are due on April 15, June 15, September 15, and January 15 of the following year. Setting aside a fixed percentage of every dollar earned into a high-yield savings account specifically for taxes is a best practice. This ensures that the liquidity is available when the payment deadlines arrive, avoiding the need to liquidate assets or dip into emergency funds.

Requesting a Penalty Waiver

Life is unpredictable, and the IRS does provide a safety valve. You can use Form 2210 to request a waiver of the penalty if the underpayment was caused by a casualty, disaster, or other unusual circumstance where imposing the penalty would be inequitable. Furthermore, if you retired (after reaching age 62) or became disabled in the current or prior tax year, and your underpayment was due to reasonable cause rather than willful neglect, the IRS may waive the penalty. Documenting these financial hardships is essential when submitting Form 2210 for a waiver request.

Conclusion: Form 2210 as a Tool for Financial Discipline

While Form 2210 is often viewed with dread as a “penalty form,” it serves as a vital reminder of the importance of financial discipline and tax liquidity. In the world of personal finance, tax is often the largest single expense an individual will face. Managing that expense with the same rigor one applies to an investment portfolio or a business budget is the hallmark of financial maturity.

By understanding the Safe Harbor rules, utilizing the Annualized Income Method, and maintaining a proactive relationship with quarterly payments, you can ensure that your capital stays in your accounts rather than being siphoned off by avoidable penalties. Form 2210 is not just a calculation of what you owe the government; it is a roadmap for how to better manage your cash flow in the years to come. In the intersection of money and law, being informed is the most effective way to preserve your wealth.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.