In the modern financial landscape, the ease of swiping a card or clicking “buy now” has revolutionized how we consume goods and services. However, this convenience comes with a complex layer of consumer protection and institutional oversight. At the heart of this system is the concept of a “disputed charge.” Whether you are a consumer noticing an unfamiliar line item on your monthly statement or a business owner facing a sudden reversal of funds, understanding the mechanics of disputed charges—often referred to as chargebacks—is essential for maintaining financial health.

A disputed charge is a formal request made by a credit or debit cardholder to their card-issuing bank to reverse a specific transaction. It is a powerful tool designed to protect consumers from fraud, billing errors, and unscrupulous business practices. Yet, for the financial ecosystem to remain balanced, the process is governed by strict regulations, timelines, and evidentiary requirements.

The Mechanics of a Disputed Charge: Definitions and Legal Frameworks

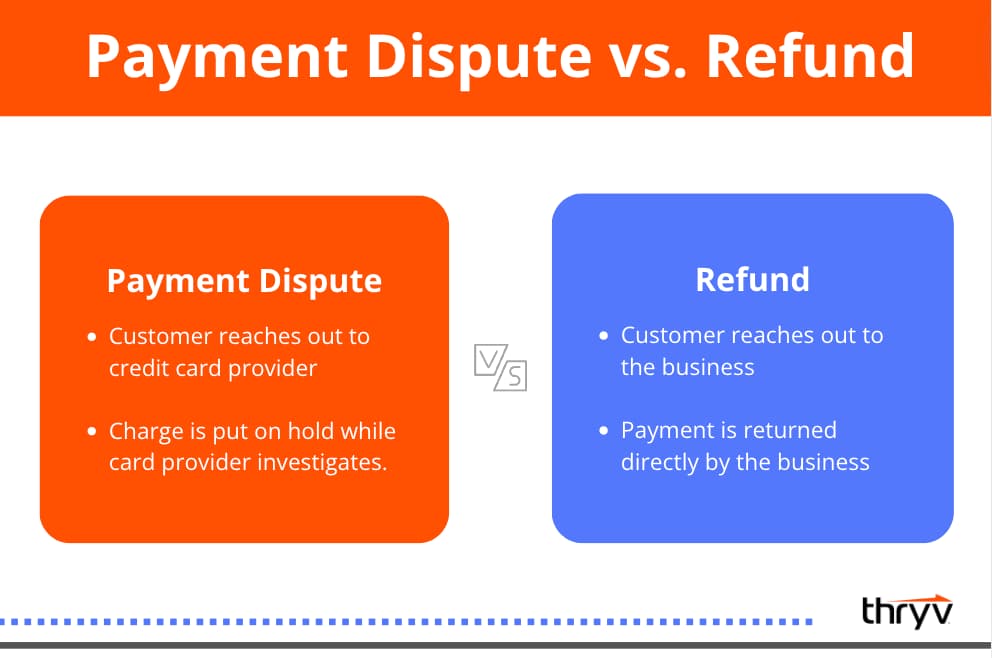

To understand what a disputed charge is, one must first understand the “Chargeback.” While many people use the terms interchangeably, a dispute is the act initiated by the consumer, while a chargeback is the technical financial mechanism that returns the funds. This system was largely codified in the United States by the Fair Credit Billing Act (FCBA) of 1974, which provides a legal safety net for consumers using open-ended credit accounts.

Defining the Chargeback Process

The process begins when a cardholder contacts their bank (the “issuer”) to challenge a transaction. The issuer reviews the claim, and if it appears valid under the merchant’s rules and federal law, they provide a provisional credit to the customer. The funds are then withdrawn from the merchant’s account. This shift of liability is what makes the dispute process so significant in business finance; it prioritizes consumer protection while placing the burden of proof on the merchant to show that the transaction was legitimate.

Common Grounds for a Dispute

Not every purchase you regret qualifies as a disputed charge. Legitimate disputes typically fall into three major categories:

- Fraudulent Transactions: The most common reason, occurring when a card is stolen or cloned, and unauthorized purchases are made.

- Service or Quality Issues: This includes “merchandise not received” or “service not as described.” If you pay for a premium laptop and receive a broken toy—and the merchant refuses to help—a dispute is your primary recourse.

- Clerical and Billing Errors: These involve duplicate charges, incorrect amounts, or failure to process a return that was already accepted by the merchant.

The Fair Credit Billing Act (FCBA) Protections

Under the FCBA, consumers have the right to dispute charges over $50 for goods and services not delivered as agreed or for billing errors. This federal law is the bedrock of consumer finance, ensuring that credit card users aren’t held liable for the mistakes or malice of others. However, it also dictates specific timelines—usually, you must file a dispute within 60 days of the statement containing the error.

Navigating the Dispute Process: A Roadmap for Consumers

Initiating a dispute is a serious financial action. While banks make it as easy as clicking a button in a mobile app, it is important to follow a logical progression to ensure a successful outcome and maintain a good standing with your financial institution.

Preliminary Steps: Contacting the Merchant

In almost all cases, the first step should not be a formal dispute. Financial experts and banks recommend contacting the merchant directly first. Most reputable businesses would rather issue a refund than face a chargeback, as chargebacks often come with heavy administrative fees from the processor. If you have a record of attempting to resolve the issue with the merchant, your case with the bank becomes significantly stronger.

Initiating the Formal Dispute with the Bank

If the merchant is unresponsive or fraudulent, you then contact your issuer. You will be asked to select a “reason code.” This code categorizes the dispute and dictates what evidence the bank will require. During this phase, the bank acts as an arbiter. They will investigate the claim, often reaching out to the merchant’s bank (the “acquirer”) to see if the merchant can provide proof of delivery or a signed receipt.

Evidence Collection and Timelines

A successful dispute is built on documentation. Consumers should keep copies of:

- Receipts and order confirmations.

- Email correspondence with the merchant.

- Photographs of damaged goods.

- Tracking numbers for returned items.

The investigation can take anywhere from 30 to 90 days. During this time, the disputed amount is usually “frozen” or credited back provisionally, meaning you do not have to pay interest on that specific amount while the case is pending.

![]()

The Business Side of Disputes: Managing and Preventing Chargebacks

While disputes are a protection for consumers, they represent a significant financial risk for businesses. In the world of business finance, a high chargeback rate can be devastating, leading to lost revenue, high fees, and even the loss of the ability to process card payments entirely.

The Financial Impact on Merchants

When a dispute is filed, the merchant doesn’t just lose the sale price of the item. They are also hit with a “chargeback fee,” which can range from $15 to $100 per transaction, regardless of whether they win the dispute. Furthermore, the merchant loses the cost of the goods sold and the shipping expenses. If a merchant’s chargeback-to-transaction ratio exceeds a certain threshold (usually 1%), they may be placed in a “high-risk” category, leading to higher processing fees or the termination of their merchant account.

How Businesses Defend Against Disputes

Merchants have the right to “representment.” This is the process where the business submits evidence to prove the charge was valid. Effective defense involves providing “compelling evidence,” such as:

- Proof of delivery signed by the customer.

- IP addresses and timestamps for digital downloads.

- Records showing the customer used the service.

- Clear documentation of the merchant’s refund and cancellation policies that the customer agreed to at checkout.

Strategies for Chargeback Prevention

Proactive financial management is the best defense for a business. Using clear “Statement Descriptors” (the name that appears on the customer’s bank statement) can prevent confusion that leads to disputes. Additionally, implementing robust customer service and easy refund policies can catch issues before they escalate to the bank level. Many businesses also employ fraud detection tools that flag suspicious transactions before they are processed.

Credit vs. Debit: Differences in Dispute Rights and Financial Liability

It is a common misconception that all plastic is created equal when it comes to disputes. In reality, the financial protections for credit cards are significantly more robust than those for debit cards, a distinction that every personal finance enthusiast should understand.

Federal Protections for Credit Cards

As mentioned, credit cards fall under the Fair Credit Billing Act. Because you are technically spending the bank’s money when you use a credit card, the bank has a vested interest in recovering those funds. Your maximum liability for unauthorized charges is $50, and many issuers offer “zero-liability” policies as a competitive feature.

The Limitations of Debit Card Disputes

Debit card transactions are governed by the Electronic Fund Transfer Act (EFTA). Because a debit card pulls money directly from your checking account, a dispute means you are trying to get your own cash back, rather than just clearing a balance on a statement.

The timelines for debit cards are much stricter:

- Within 2 days: Your liability is limited to $50.

- Within 60 days: Your liability could jump to $500.

- After 60 days: You may have no protection at all and lose the entire amount.

Furthermore, while a credit card dispute leaves the money in your pocket during the investigation, a debit card dispute often means that money is missing from your bank account for weeks while the bank investigates.

Long-term Financial Health and the Ethics of Disputes

While the dispute system is a vital safety net, it must be used ethically. The rise of “friendly fraud” has become a major concern in the financial sector, affecting the costs of goods and services for everyone.

Friendly Fraud and Its Consequences

“Friendly fraud” occurs when a consumer makes a legitimate purchase but then disputes it through their bank to get their money back, either because they don’t recognize the charge, a family member made the purchase without permission, or they are simply trying to “get it for free.” While it may seem harmless to the individual, banks track dispute patterns. If a consumer develops a history of frequent or unfounded disputes, the bank may close their account, and it can negatively impact their internal “risk score,” making it harder to get loans or new credit lines in the future.

Protecting Your Credit Score and Relationship with Lenders

A legitimate dispute does not inherently hurt your credit score. However, if you stop paying your entire credit card bill because you are waiting for a dispute to clear—without verifying that the amount is officially deferred—you could end up with a late payment on your credit report. It is always wise to pay the undisputed portion of your bill and stay in constant communication with your bank’s dispute department.

In conclusion, understanding what a disputed charge is serves as a cornerstone of modern financial literacy. For the consumer, it is a shield against fraud and poor service. For the business, it is a risk to be managed through excellent service and rigorous record-keeping. By navigating this process with honesty and due diligence, we contribute to a more stable and trustworthy global financial system.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.