In the realm of personal finance and real estate investing, understanding the legal instruments that govern property ownership and debt is essential. For many prospective homeowners and seasoned investors, the term “mortgage” is a household name, yet in many U.S. states, the “Deed of Trust” is the actual legal document used to secure a real estate loan. While both serve the same ultimate purpose—securing a loan with a piece of property—the Deed of Trust carries specific financial implications, structural differences, and procedural nuances that can significantly impact a borrower’s rights and a lender’s security.

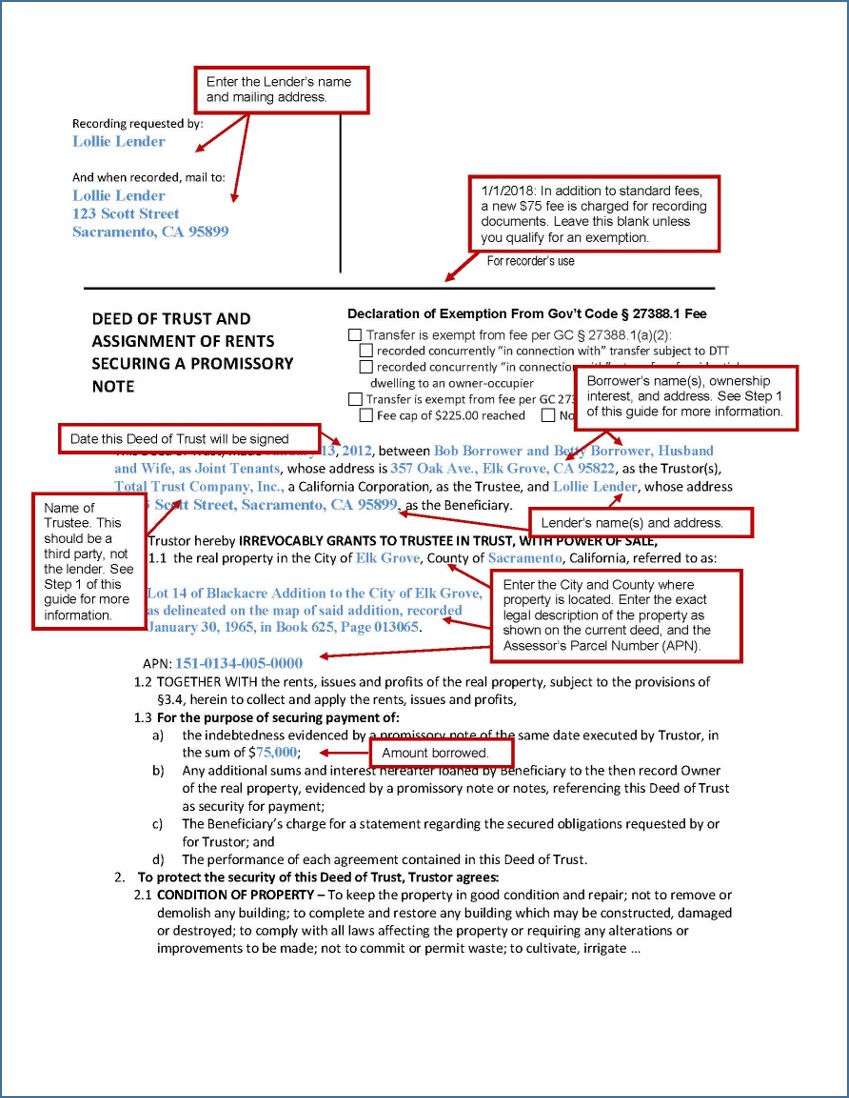

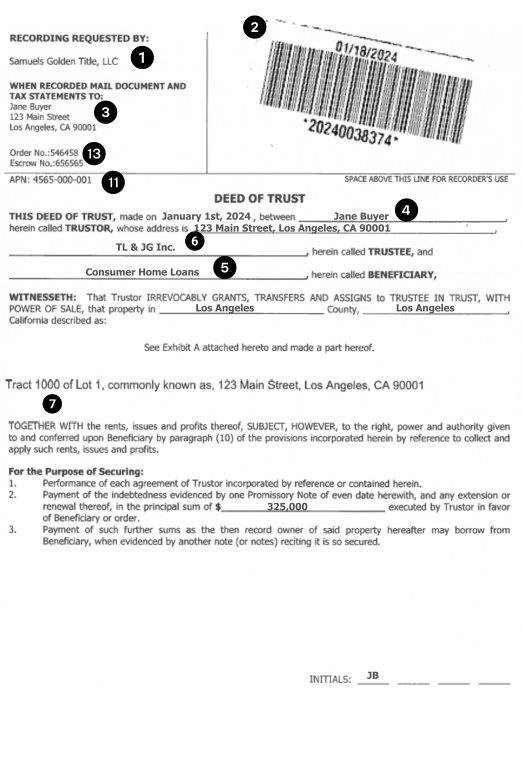

A Deed of Trust is essentially an agreement between a borrower and a lender to have a third party hold the legal title to a property until the debt is fully repaid. From a financial perspective, this document is a critical component of risk management, determining how a default is handled and how quickly a property can be liquidated. To master the “Money” side of real estate, one must understand how this three-party instrument functions and why it is often preferred by institutional and private lenders alike.

The Mechanics of a Deed of Trust: The Three-Party Agreement

Unlike a standard mortgage, which typically involves only two parties (the borrower and the lender), a Deed of Trust involves three distinct entities. Each party plays a specific role in the financial ecosystem of the loan, ensuring that the terms of the agreement are met and providing a mechanism for resolution should the borrower fail to meet their obligations.

The Trustor (The Borrower)

The Trustor is the individual or entity borrowing the funds to purchase the real estate. In the context of personal finance, the Trustor is the person making the down payment and committing to monthly installments. Although the Trustor holds “equitable title”—meaning they have the right to use, enjoy, and build equity in the home—they do not hold “legal title” while the Deed of Trust is in effect. Their primary financial responsibility is to maintain the property, pay taxes, and ensure the debt is serviced according to the promissory note.

The Beneficiary (The Lender)

The Beneficiary is the entity providing the capital. This could be a traditional bank, a credit union, or a private investor. The Beneficiary’s interest is purely financial; they want to ensure their capital is returned with interest. The Deed of Trust protects the Beneficiary by providing a streamlined path to recover their investment if the Trustor defaults. Because the Beneficiary does not hold the title directly, they rely on the third-party Trustee to manage the legal standing of the collateral.

The Trustee (The Neutral Third Party)

The Trustee is perhaps the most misunderstood part of the arrangement. Usually a title company or an escrow agent, the Trustee holds “nominal” or legal title to the property in trust for the Beneficiary. The Trustee’s role is largely passive until one of two things happens: either the loan is paid off in full, or the borrower defaults. Their neutral position is designed to ensure that the foreclosure process, if necessary, is handled according to the specific “power of sale” clause written into the document, often bypassing the traditional court system.

Deed of Trust vs. Mortgage: Key Differences for Investors and Homeowners

From a distance, a Deed of Trust and a mortgage look identical: you borrow money, you buy a house, and you pay it back over 30 years. However, for those focused on financial strategy and asset protection, the differences are monumental, particularly regarding how title is held and how foreclosure is executed.

Judicial vs. Non-Judicial Foreclosure

The most significant financial distinction lies in the foreclosure process. Mortgages generally require a “judicial foreclosure,” meaning the lender must sue the borrower in court to prove a default has occurred before they can sell the property. This process is time-consuming and expensive for the lender.

In contrast, a Deed of Trust typically includes a “power of sale” clause, which enables a “non-judicial foreclosure.” If the borrower stops making payments, the Trustee can initiate a sale of the property without court oversight, provided they follow state-mandated notice requirements. For a lender, this reduces the “time-to-liquidity,” making the Deed of Trust a more attractive and lower-risk financial instrument.

The Power of Sale Clause

The Power of Sale clause is the engine that drives the Deed of Trust. It grants the Trustee the authority to sell the property to satisfy the debt if the Trustor defaults. For the borrower, this means less time to cure a default compared to a judicial process. For the investor or lender, it means a more predictable timeline for recovering capital. Understanding this clause is vital for anyone engaged in distressed debt investing or high-interest private lending, as it dictates the speed at which an asset can be repositioned.

Legal Title vs. Equitable Title

In a mortgage state, the borrower usually holds the legal title. In a Deed of Trust state, the borrower holds equitable title while the Trustee holds legal title. This distinction might seem academic until it comes to the “reconveyance” of the title. When a homeowner finishes paying off a Deed of Trust, they must ensure the Trustee issues a “Deed of Reconveyance,” which officially transfers the legal title back to the homeowner. Forgetting this step can lead to significant hurdles when trying to sell the property or use it as collateral for a future business loan.

The Financial Lifecycle of a Deed of Trust

Understanding the lifecycle of a Deed of Trust allows borrowers and investors to navigate the financial milestones of property ownership with greater clarity. From the moment the ink dries on the closing documents to the final payment, several legal and financial transitions occur.

Execution and Recordation

The process begins with the execution of the promissory note and the Deed of Trust. While the note is the “I.O.U.” (the promise to pay), the Deed of Trust is the security for that promise. Once signed, the document is recorded in the county records where the property is located. This recordation is a public notice of the lender’s “lien” on the property. For a real estate investor, checking these records is a fundamental part of due diligence, as it reveals the level of debt leveraged against a potential acquisition.

The Reconveyance Process

Once the final payment is made, the Beneficiary (lender) notifies the Trustee that the debt has been satisfied. The Trustee then executes a Deed of Reconveyance, which is recorded in the public record to show that the lien has been released. From a personal finance perspective, this is the moment of true “homeownership,” where the individual holds both equitable and legal title, free of the lender’s encumbrance. This document is the ultimate goal of any long-term debt-reduction strategy in real estate.

Default and the Foreclosure Timeline

If the Trustor fails to meet the financial obligations, the “Notice of Default” is filed. This is the first stage of the non-judicial foreclosure process. The timeline varies by state—often ranging from 90 to 120 days—during which the borrower may have a “right of reinstatement” to pay the arrears and stop the process. If the debt isn’t settled, the Trustee schedules a “Trustee’s Sale” (an auction). For the savvy money manager, understanding this timeline is key to negotiating short sales or participating in foreclosure auctions where properties can often be acquired below market value.

Why Deeds of Trust Matter in Private Lending and Real Estate Investing

For those looking to move beyond simple homeownership and into the world of sophisticated finance, the Deed of Trust is a powerful tool for generating passive income and securing private capital.

Using Deeds of Trust for Seller Financing

In high-interest rate environments, seller financing becomes a popular tool. A property owner (acting as the Beneficiary) can sell their home to a buyer (the Trustor) and carry the “paper.” By using a Deed of Trust, the seller ensures that if the buyer stops paying, they can reclaim the property relatively quickly through the non-judicial foreclosure process. This allows the seller to earn interest income—often at rates higher than a savings account—while maintaining a secured position.

Risk Management for Private Lenders

Private lending, or “hard money” lending, relies heavily on the Deed of Trust. Because these loans are often shorter-term and higher-risk, the lender needs the security of a quick foreclosure process if things go south. By structuring the deal with a reputable Trustee, private lenders can mitigate the risk of a borrower dragging them through years of litigation, which is a common hazard in judicial-only mortgage states.

Diversifying a Portfolio with Real Estate Paper

Investors often choose to “buy the paper” rather than the physical property. Investing in Trust Deeds involves purchasing existing loans from other lenders. This allows an investor to act as the bank, collecting monthly interest payments without the headaches of property management (tenants, toilets, and trash). However, this requires a deep understanding of the Deed of Trust’s terms, the property’s value, and the borrower’s creditworthiness to ensure the investment remains a “secured” one.

Conclusion: Financial Literacy and the Deed of Trust

The Deed of Trust is more than just a stack of papers signed at a closing table; it is a sophisticated financial instrument that balances the rights of the borrower with the security requirements of the lender. For the average person, it represents the bridge between debt and the ultimate goal of debt-free property ownership. For the investor, it represents a mechanism for risk mitigation and a vehicle for generating consistent returns.

Whether you are a first-time homebuyer in a Deed of Trust state or a professional looking to diversify into private lending, understanding the roles of the Trustor, Beneficiary, and Trustee is non-negotiable. By mastering the nuances of non-judicial foreclosure, title reconveyance, and the power of sale, you position yourself to make smarter, more secure financial decisions in the complex world of real estate. Real estate is often the largest asset in a person’s financial portfolio; knowing exactly how that asset is secured is the hallmark of true financial literacy.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.