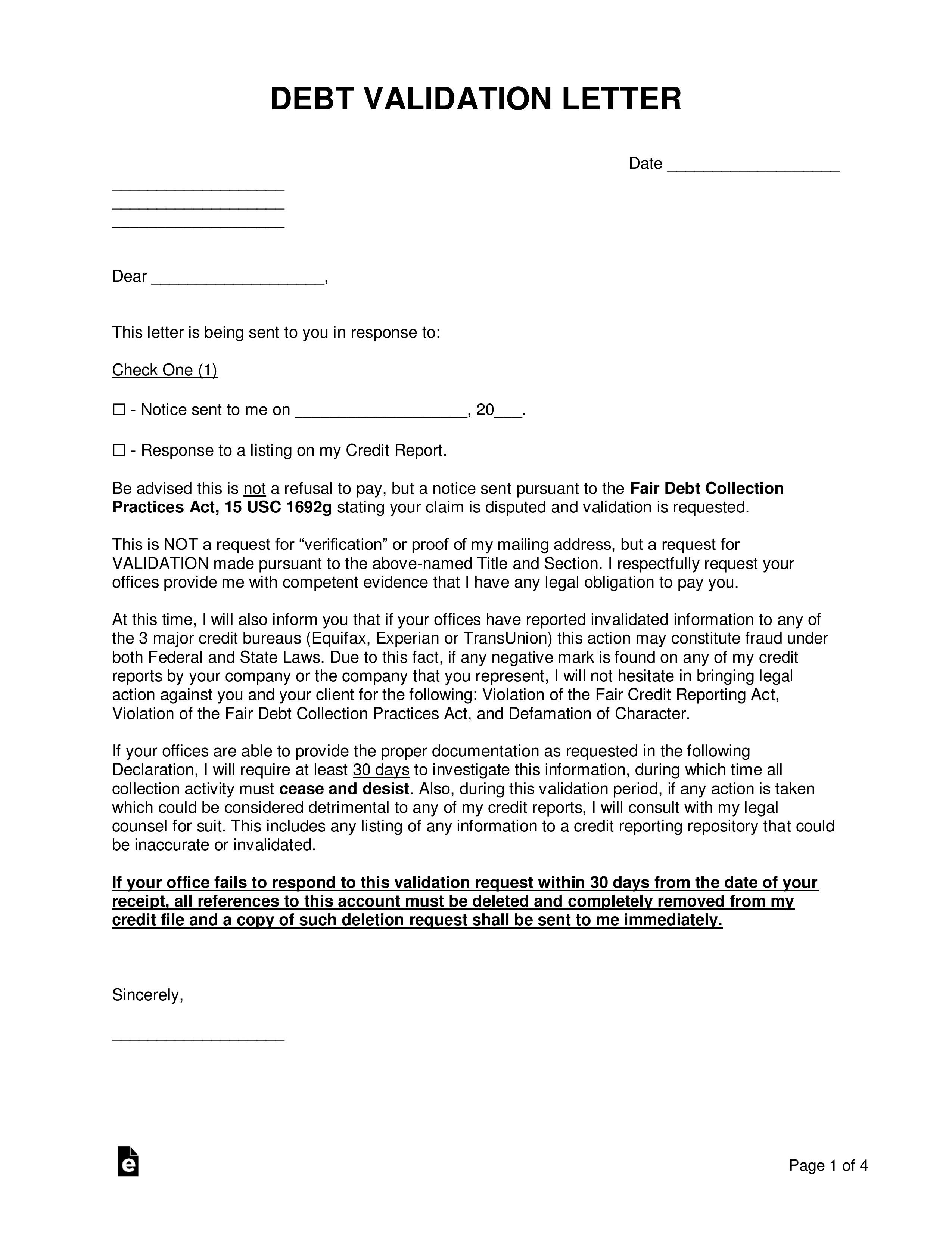

A debt validation letter is a crucial document that can empower consumers facing debt collection. It’s not merely a piece of paper; it’s a right afforded to you under federal law, specifically the Fair Debt Collection Practices Act (FDCPA). Understanding what a debt validation letter is, why it’s important, and how to effectively use it can be a game-changer in navigating the often-stressful world of debt collection. This letter serves as your official request for a debt collector to prove they have the legal right to collect a debt from you and that the amount they claim is accurate.

The FDCPA, enacted in 1977, aims to protect consumers from abusive, deceptive, and unfair debt collection practices. One of its key provisions is the consumer’s right to request verification of a debt. A debt validation letter is the formal mechanism for exercising this right. When a debt collector contacts you about a debt, especially if it’s a debt you don’t recognize, believe is inaccurate, or has been sold to a third party, sending a debt validation letter is your first line of defense.

Understanding the Purpose and Importance of Debt Validation

The core purpose of a debt validation letter is to shift the burden of proof from the consumer to the debt collector. When you send this letter, you are essentially asking the collector to provide evidence that they are legally entitled to collect the debt and that the amount they are demanding is correct. This is particularly vital in situations where the debt is old, has been transferred multiple times, or you have no prior record of it.

Why is Debt Validation Necessary?

The debt collection industry can be complex and, unfortunately, prone to errors and even outright fraud. Debts can be sold to different collection agencies, sometimes multiple times. With each transfer, the risk of errors in account information, balances, or ownership increases. Furthermore, some collectors may attempt to collect on debts that are past the statute of limitations for legal action, or even debts that have already been paid or settled.

Without debt validation, you might:

- Pay a debt that isn’t yours: You could be held responsible for a debt incurred by someone with a similar name or in a fraudulent transaction.

- Pay an incorrect amount: The balance owed might be inflated due to accrued interest, fees, or simple accounting errors.

- Pay a debt that is legally uncollectable: The debt might be beyond the statute of limitations, or the collector might not have proper legal standing to collect.

- Become a victim of harassment: Without proper validation, you may be subjected to persistent and potentially illegal collection tactics.

The Legal Basis: The Fair Debt Collection Practices Act (FDCPA)

The FDCPA provides a robust framework for consumer protection against unscrupulous debt collection practices. It outlines what debt collectors can and cannot do, and it grants consumers specific rights. The right to request debt validation is one of the most significant of these rights.

Under the FDCPA, if you dispute a debt, you have the right to request verification of that debt from the collector. The collector must then cease all collection efforts until they provide you with the requested validation. This mechanism is designed to prevent collectors from harassing consumers with unverified claims.

How to Send a Debt Validation Letter and What to Expect

Sending a debt validation letter is a straightforward process, but it requires careful attention to detail and adherence to specific guidelines to ensure its effectiveness. The timing of your letter is crucial, as is what you include and how you send it.

The Right Timing and Content of Your Letter

The FDCPA grants you 30 days from the initial communication from a debt collector to dispute the debt. This means that if you receive a collection letter or phone call, you have a 30-day window to send your debt validation request. While you can technically send it outside this window, sending it within the first 30 days triggers specific FDCPA protections, compelling the collector to pause collection efforts until validation is provided.

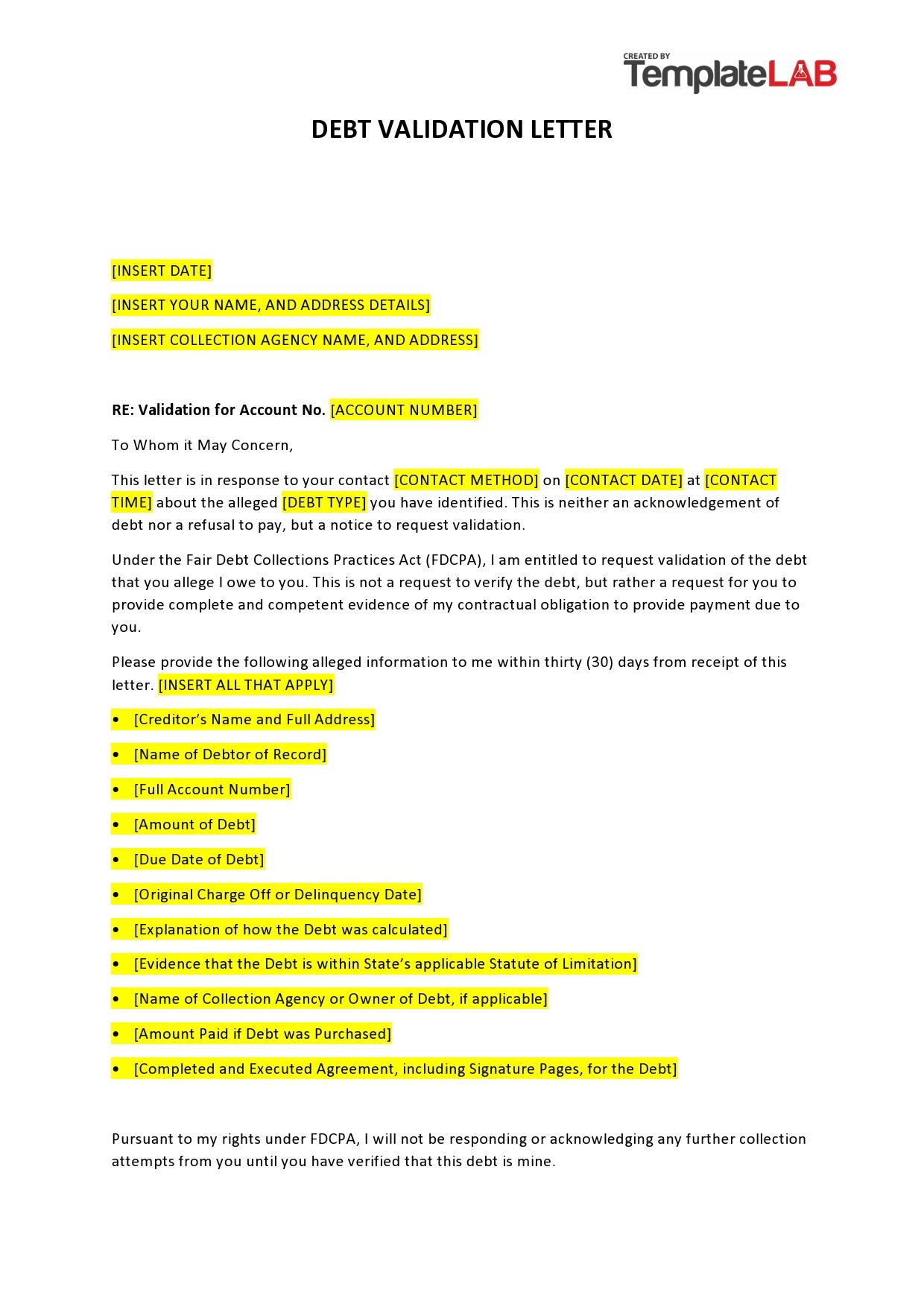

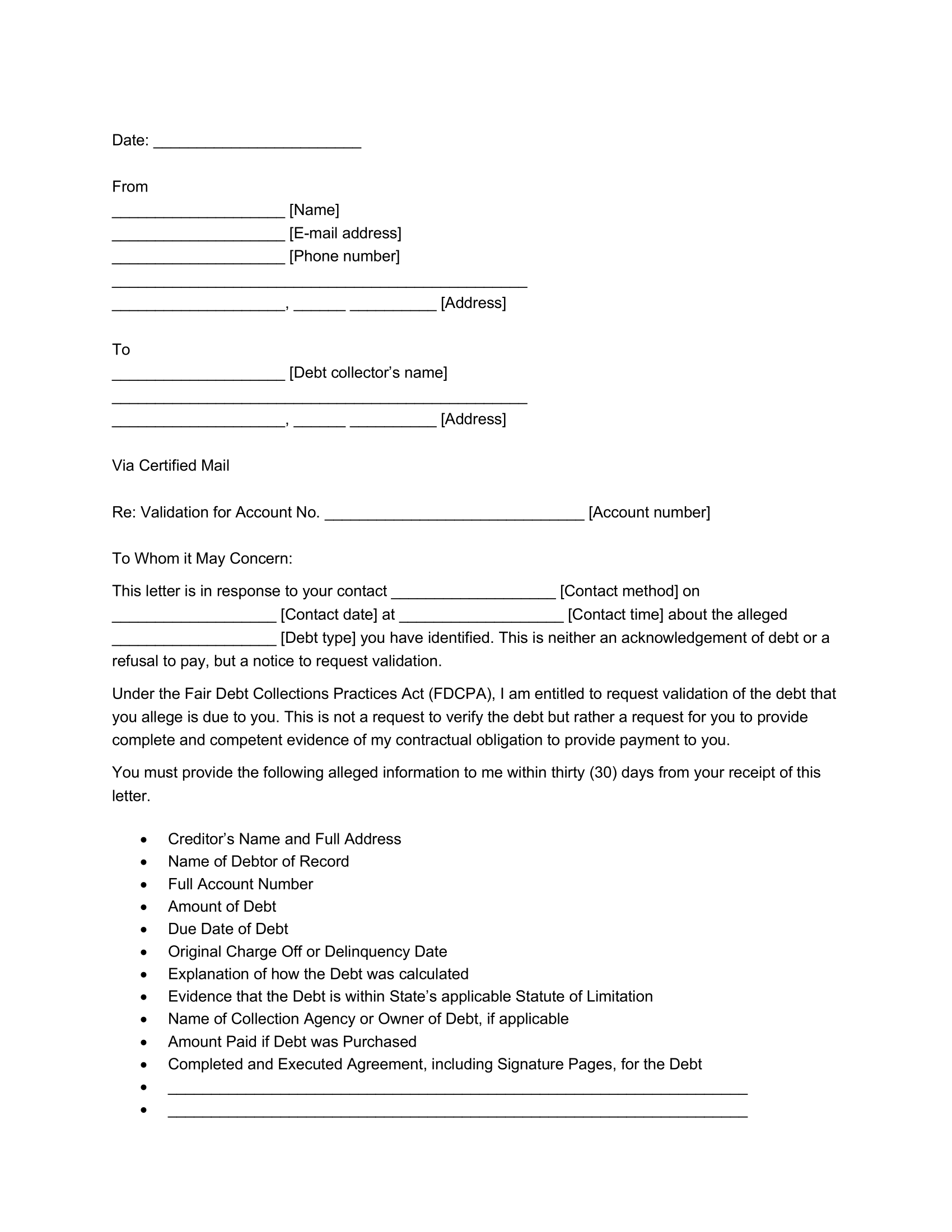

When drafting your letter, include the following key information:

- Your full name and address: Ensure the collector can identify you.

- The name and address of the debt collector: Address the letter directly to the collection agency.

- The account number (if provided by the collector): This helps them locate the specific debt.

- A clear statement that you are requesting debt validation: State explicitly that you dispute the debt and require verification.

- A request for specific documentation: Be precise about what you want. This could include:

- Proof of the original creditor’s name.

- The original signed contract or agreement.

- A complete payment history.

- The amount of the debt, including any interest, fees, or charges.

- Proof that the debt collector is legally entitled to collect the debt (e.g., an assignment agreement from the original creditor).

- Proof that the statute of limitations has not expired.

- A statement that you want them to cease collection activities until validation is provided: This reinforces your FDCPA rights.

- A statement that you do not want to be contacted by phone: If you prefer written communication.

- Your signature and the date: This makes the letter official.

Sending Your Letter: Certified Mail is Key

It is absolutely imperative that you send your debt validation letter via certified mail with a return receipt requested. This method provides you with undeniable proof that the collector received your letter and on what date. This documentation is invaluable if the collector fails to comply or if you need to pursue further action. Keep a copy of your letter and the return receipt for your records.

What to Expect After Sending the Letter

Once the debt collector receives your validated letter, they are legally obligated to stop all collection activities until they provide you with the requested validation. This pause can be incredibly beneficial, giving you breathing room to assess the situation without the pressure of immediate collection efforts.

The collector has a few options once they receive your request:

- Provide Validation: If they have the necessary documentation, they will send it to you. Review this information carefully. If it clearly proves the debt is valid and the amount is accurate, you may then decide how to proceed with repayment.

- Cease Collection: If the collector cannot provide the requested validation, or if the debt is indeed uncollectable (e.g., past the statute of limitations, not theirs to collect), they must cease all collection efforts. They cannot continue to pursue you for the debt.

- Sell the Debt: In some cases, a collector might sell the debt to another agency that may be better equipped to validate it. If this happens, the new collector must also adhere to FDCPA rules and provide you with validation upon request.

If the collector continues to contact you for payment or engages in collection activities after receiving your validation letter without providing the requested proof, they are likely violating the FDCPA. This violation could give you grounds to take legal action against the collector.

Potential Outcomes and Next Steps After Validation

Receiving a debt validation letter from a collector is the first step in a process that can lead to several outcomes. Your subsequent actions will depend on the information provided by the collector and your assessment of its validity.

Reviewing the Validation Information

Upon receiving the validation documents, it’s crucial to examine them thoroughly. Compare the information provided against your own records. Look for any discrepancies in account numbers, balances, dates, or names.

Ask yourself:

- Does this documentation clearly identify the original creditor?

- Does it show a clear chain of ownership if the debt has been sold?

- Is the amount claimed accurate and supported by documentation?

- Is the debt within the statute of limitations for your state?

If the validation provided is insufficient, incomplete, or raises further questions, you should communicate this in writing to the debt collector, again using certified mail. You can state that the information provided does not constitute proper validation and that they must cease collection until they can provide satisfactory proof.

When the Debt is Validated

If the collector provides sufficient evidence that the debt is valid, belongs to you, and the amount is accurate, you then have a decision to make. You are not legally obligated to pay a debt if it’s past the statute of limitations for legal action, but if it’s within that period and validated, it is a legitimate debt you owe.

Options include:

- Negotiating a Settlement: You might be able to negotiate a lump-sum settlement for less than the full amount owed. This is often possible with collection agencies.

- Arranging a Payment Plan: If you cannot afford to pay the full amount at once, you can propose a payment plan that fits your budget.

- Paying the Full Amount: If you have the funds available, paying the debt in full will resolve the issue.

Always get any settlement agreement or payment plan in writing before making any payments.

When the Debt is Not Validated or is Uncollectable

If the debt collector fails to provide validation, provides incomplete or inaccurate validation, or if the debt is determined to be uncollectable (e.g., past the statute of limitations), the collector must cease their collection efforts. They cannot legally pursue you for this debt.

In such cases, you should:

- Continue to communicate in writing: Keep a record of all correspondence.

- Consider reporting the collector: If the collector continues to harass you or violates the FDCPA, you can file a complaint with the Consumer Financial Protection Bureau (CFPB) and your state Attorney General’s office.

- Consult with a consumer protection attorney: If you believe the collector has violated your rights, an attorney can advise you on your legal options, which might include suing the collector for damages.

The Broader Impact of Debt Validation on Consumer Rights

The debt validation letter is more than just a transactional document; it’s a powerful tool that empowers consumers and upholds fundamental rights in the financial landscape. It serves as a critical check against potential abuses within the debt collection industry and fosters a more transparent and fair system.

Empowering Consumers in Financial Disputes

In the realm of personal finance, individuals can often feel overwhelmed by debt and the aggressive tactics sometimes employed by collectors. The debt validation letter democratizes the power dynamic, placing the onus on the collector to prove their claim. This shifts the burden from the consumer, who might be in a vulnerable financial position, to the entity seeking payment, which is expected to have proper documentation and legal standing.

By understanding and utilizing their right to request validation, consumers can:

- Protect themselves from scams and fraud: Invalid debts are unfortunately common, and validation is the primary defense.

- Ensure accuracy in financial obligations: Correcting errors in debt amounts or ownership prevents overpayment and financial hardship.

- Gain control over their financial situation: By pausing collection efforts, consumers gain valuable time to assess their finances, seek advice, and make informed decisions without undue pressure.

- Hold debt collectors accountable: The FDCPA, enforced through tools like the debt validation letter, creates a framework for accountability, deterring illegal practices and encouraging ethical conduct.

Fostering Transparency and Accountability in Debt Collection

The debt collection industry operates on the premise of collecting legitimate debts. However, the sale and transfer of debt portfolios can sometimes lead to a loss of original documentation and an increase in errors. The FDCPA, and by extension, the debt validation process, acts as a crucial mechanism for ensuring transparency and accountability in this ecosystem.

When collectors know that consumers can and will request validation, they are incentivized to maintain accurate records and to acquire debts only when they have proper proof of ownership and the correct amounts. This ultimately contributes to a more trustworthy debt collection market.

Furthermore, the existence of the debt validation right encourages consumers to be more proactive and informed about their financial dealings. It underscores the importance of understanding financial agreements and the rights afforded to them under consumer protection laws.

When to Consider Professional Assistance

While sending a debt validation letter is a DIY process, there are instances where professional assistance can be highly beneficial. If you are dealing with a large or complex debt, if the collector is particularly aggressive or appears to be in violation of the FDCPA, or if you are unsure about the validity of the debt, consulting with a qualified consumer protection attorney or a reputable credit counseling agency is advisable.

These professionals can:

- Help you draft a more comprehensive and legally sound debt validation letter.

- Review the validation documents provided by the collector.

- Negotiate with debt collectors on your behalf.

- Represent you in legal disputes if necessary.

In conclusion, a debt validation letter is a fundamental right designed to protect consumers from fraudulent or inaccurate debt collection practices. By understanding its purpose, knowing how to send it correctly, and being prepared for the potential outcomes, consumers can effectively navigate debt collection issues and assert control over their financial well-being. It is a cornerstone of consumer protection, empowering individuals to demand proof and ensure fairness in their financial obligations.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.