A de facto relationship, often misunderstood, is a critical legal and financial designation that carries significant implications for individuals who live together without being legally married. While the specifics can vary slightly by jurisdiction, the core concept revolves around two people, regardless of gender, living together on a genuine domestic basis, much like a married couple. This status is not merely a social observation; it bestows upon partners certain rights and responsibilities, particularly concerning financial matters, property, and inheritance, that mirror those of married spouses. For anyone navigating shared finances, property ownership, or planning for the future with a partner, understanding what constitutes a de facto relationship is not just prudent—it’s essential for protecting financial interests and ensuring future security.

Defining De Facto: More Than Just Living Together

The determination of a de facto relationship goes far beyond simply cohabiting. Legal systems examine the nature of the relationship holistically, looking for clear indicators of commitment and interdependence that transcend a casual living arrangement or housemate situation. This recognition is crucial for financial planning, as it can trigger entitlements and obligations that individuals might not anticipate if they assume their unmarried status absolves them of such responsibilities.

Legal Recognition and Financial Implications

The primary reason for defining a de facto relationship is to ensure equitable treatment and protection under the law for couples who choose not to marry but have nonetheless built a life together. Financially, this means de facto partners may have similar rights to married couples regarding property division, spousal maintenance (or equivalent), and superannuation splitting upon separation. Furthermore, in the event of one partner’s death, the surviving de facto partner may have rights concerning the deceased’s estate, superannuation, and other assets, even if a formal will does not explicitly name them, depending on intestacy laws and estate claims. This legal recognition underscores the importance of proactive financial planning and clear communication within a de facto partnership to avoid complex and costly disputes down the line.

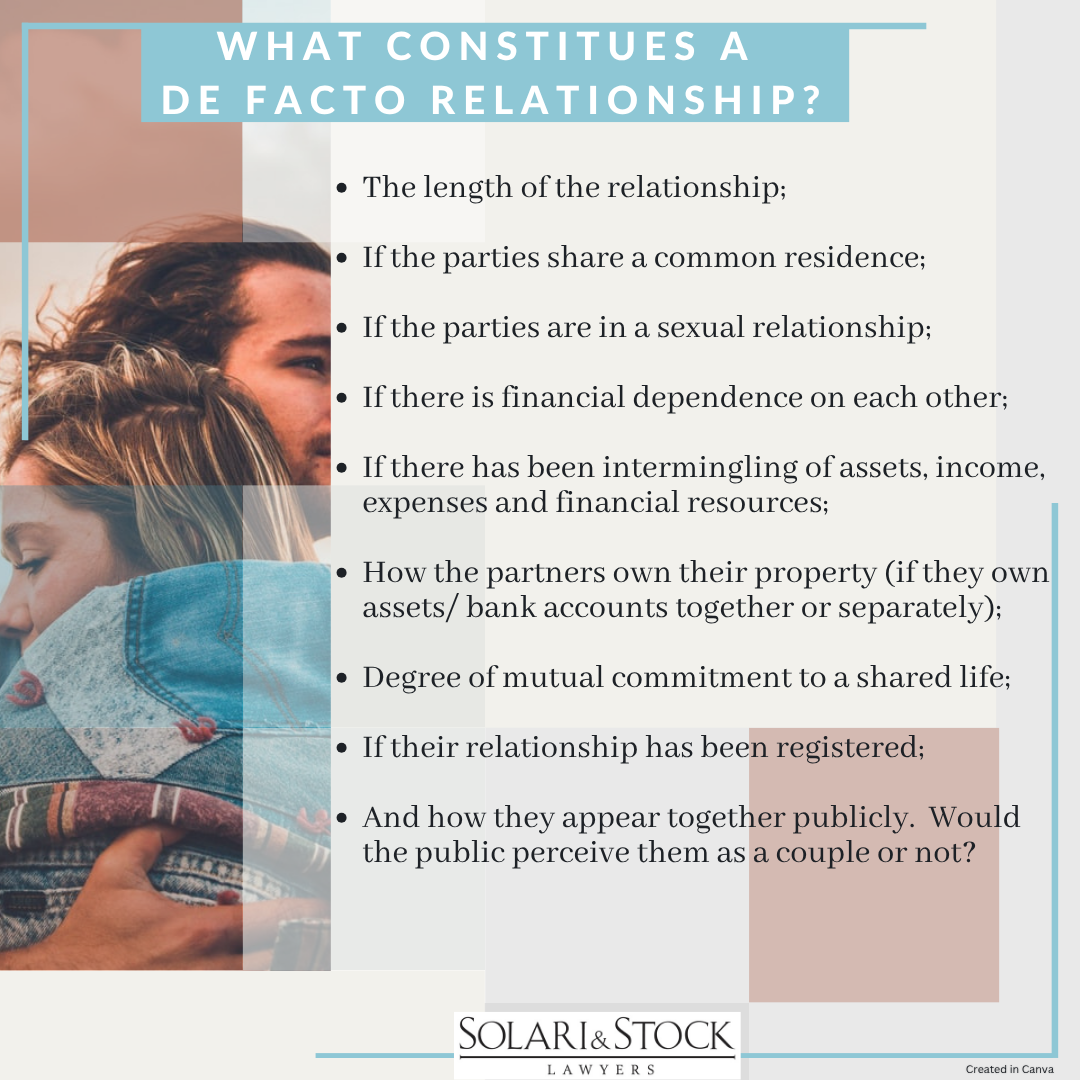

Key Indicators of a De Facto Relationship

Courts and legal frameworks assess several factors to determine if a de facto relationship exists, focusing heavily on financial interdependence and shared lives. These indicators often include:

- Duration of the Relationship: While there’s no universal minimum, many jurisdictions consider relationships of two years or more as a strong indicator, though shorter relationships with a child or significant financial contributions can also qualify.

- Nature and Extent of Common Residence: Living together is a key factor, but the quality of that shared life (e.g., sharing household duties, joint bills) is more important than just having the same address.

- Financial Aspects of the Relationship: This is often the most critical area for the “Money” niche. Evidence includes joint bank accounts, shared payment of household expenses, shared assets (like property or vehicles), joint investments, and the extent of financial support provided by one partner to the other. Commingling of funds and shared financial goals are strong indicators.

- Nature of the Relationship: This encompasses whether a sexual relationship exists, the commitment to a shared life, and the public aspects of the relationship (e.g., presenting as a couple to family, friends, and the community).

- Care and Support of Children: If children are involved, whether they are children of both partners or one partner’s child being cared for by the other, this significantly strengthens the case for a de facto relationship.

- Ownership, Use, and Acquisition of Property: Joint ownership of assets, particularly real estate, is a powerful indicator of a de facto relationship, highlighting shared financial commitment and investment in a common future.

Each of these factors is weighed collectively, with no single factor being decisive on its own. The overarching theme is the demonstration of a genuine commitment to a shared life, especially in a financial context.

The Financial Entanglements of De Facto Partnerships

The financial interplay within a de facto relationship can be complex and often mirrors that of a marriage. Partners frequently pool resources, make joint investments, and incur shared liabilities, creating a web of financial interdependence that requires careful management and foresight.

Shared Assets and Liabilities

One of the most immediate financial implications of a de facto relationship is the commingling of assets and liabilities. This often begins subtly with joint bank accounts for household expenses but can quickly escalate to shared credit cards, loans for vehicles or other significant purchases, and even business ventures. While convenient for day-to-day management, these shared financial instruments mean that both partners can be legally responsible for the debts incurred, regardless of who made the actual purchase. For assets, joint ownership means that both parties have a legal claim, but the percentage of ownership or contribution can become contentious upon separation if not clearly documented. Understanding the implications of joint tenancy versus tenancy in common for property, for example, is crucial for de facto partners.

Property and Real Estate Considerations

Real estate is often the largest asset acquired within a de facto relationship, and its ownership has significant financial ramifications. Whether partners contribute equally to a deposit, mortgage repayments, or renovations, or if one partner contributes more than the other, these contributions can establish a financial interest. If the property is solely in one partner’s name, the other partner might still have a claim based on their financial contributions, direct or indirect, or non-financial contributions to the property’s value (e.g., home improvements, care for children enabling the other partner to work). The absence of a formal declaration of trust or a written agreement regarding equity can lead to protracted disputes if the relationship ends.

Superannuation and Retirement Planning

Superannuation (or similar retirement funds) is a key asset that is increasingly considered during de facto relationship breakdowns. Many jurisdictions now allow for the splitting of superannuation interests between de facto partners upon separation, similar to married couples. This means that a portion of one partner’s superannuation may be transferred to the other partner, particularly if there is a significant disparity in their respective retirement savings or if one partner made substantial non-financial contributions to the relationship, impacting their ability to save for retirement. Furthermore, de facto partners are often recognized as beneficiaries for superannuation death benefits, but clear beneficiary nominations are always advisable to avoid disputes and ensure funds are distributed according to intent. Proper financial planning within a de facto relationship must therefore encompass both current assets and future retirement savings.

Protecting Your Financial Future

Given the complex financial implications of de facto relationships, proactive measures are paramount to safeguarding individual and shared financial interests. Clear communication, transparency, and formal agreements can prevent future disputes and provide peace of mind.

The Value of a Financial Agreement

A Financial Agreement, sometimes known as a Cohabitation Agreement or a “pre-nup for de factos,” is arguably the most powerful tool for de facto couples to manage their financial future. This legally binding document outlines how assets, liabilities, and superannuation would be divided in the event of separation, and it can also address spousal maintenance. It allows couples to deviate from default legal provisions and tailor arrangements that reflect their unique circumstances, contributions, and expectations. A well-drafted agreement can cover current assets, future inheritances, business interests, and financial support for children from previous relationships. Seeking independent legal advice for both partners is crucial to ensure the agreement is valid and enforceable. This investment upfront can save significant legal fees and emotional distress should the relationship unfortunately end.

Estate Planning and Wills

For de facto partners, comprehensive estate planning is critical. While some laws provide for de facto partners in intestacy rules (where there is no will), these provisions may not align with the partners’ wishes and can lead to disputes with other family members. A clear, up-to-date will ensures that assets are distributed according to the deceased partner’s intentions, providing for the surviving de facto partner and any children. Beyond a will, partners should consider appointing each other as enduring power of attorney for financial and medical decisions, ensuring that their chosen partner can manage their affairs if they become incapacitated. Superannuation beneficiary nominations are also essential, as superannuation often falls outside the will and requires specific nominations to be paid to the intended recipient.

Managing Joint Accounts and Debts

Transparent and strategic management of joint accounts and debts is fundamental to a healthy de facto financial relationship. While joint accounts offer convenience, it’s wise to maintain separate individual accounts for personal spending and savings. Clearly define how shared expenses will be met and how savings will be allocated. For joint debts, both partners should fully understand their legal obligations and the potential impact on their credit scores if one partner defaults. Regular financial discussions, perhaps with a financial planner, can help de facto couples set shared goals, monitor progress, and adjust strategies as their financial circumstances evolve. This proactive approach fosters financial harmony and reduces potential points of contention.

When Things Go Wrong: De Facto Separation and Financial Settlements

Even with the best intentions, de facto relationships can end, and when they do, the financial implications can be as complex and significant as those following a divorce. Navigating a de facto separation requires a clear understanding of financial rights and obligations to ensure an equitable settlement.

Understanding Financial Claims

Upon the breakdown of a de facto relationship, partners typically have the right to seek a financial settlement that divides the assets and liabilities accumulated during the relationship, and potentially some prior to it. The process often considers four key steps: identifying all assets and liabilities (the ‘asset pool’), assessing the financial and non-financial contributions of each partner (including direct financial contributions, homemaking, parenting, and career sacrifices), evaluating future needs (such as age, health, earning capacity, and care of children), and finally, determining whether the proposed division is just and equitable. Unlike simply splitting assets 50/50, this process is highly individualised, aiming for a fair outcome based on each partner’s unique circumstances and contributions to the relationship. It’s not uncommon for these settlements to extend to superannuation, investments, businesses, and property.

The Role of Legal and Financial Advice

Given the complexity and emotional nature of de facto separations, engaging professional legal and financial advisors is not merely beneficial but often essential. A family lawyer specializing in de facto matters can explain your rights and obligations, help identify all relevant assets and liabilities, negotiate with your ex-partner (or their lawyer), and represent your interests in court if an agreement cannot be reached. A financial planner can assist in valuing assets, understanding the tax implications of different settlement options, and helping you reconstruct your financial life post-separation. They can provide projections for your future financial stability based on various settlement scenarios. Attempting to navigate these intricate financial settlements alone can lead to unfavorable outcomes, protracted disputes, and significant financial loss. Professional advice ensures that decisions are informed, equitable, and protect your long-term financial well-being.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.