In the realm of personal finance and investing, few concepts hold as much transformative power as compound interest. Often lauded as the “eighth wonder of the world” by Albert Einstein, it is the invisible engine that drives significant wealth accumulation over time. Understanding compound interest isn’t just an academic exercise; it’s a fundamental principle that empowers individuals to make informed decisions about their savings, investments, and even their debt, shaping their financial future profoundly. At its core, compound interest is interest earned not only on the initial principal but also on the accumulated interest from previous periods. This seemingly simple mechanism creates a powerful snowball effect, where your money starts working harder for you, generating returns on its own returns, leading to exponential growth that far surpasses what simple interest can achieve. For anyone aspiring to build a robust financial foundation, master their investments, or simply grow their savings efficiently, grasping the nuances of compound interest is not merely beneficial—it is essential.

The Core Mechanism of Compound Interest

To truly appreciate the power of compound interest, it’s crucial to understand its underlying mechanics and how it fundamentally differs from its simpler counterpart. This distinction is the bedrock upon which effective financial planning is built.

Simple vs. Compound Interest: A Fundamental Difference

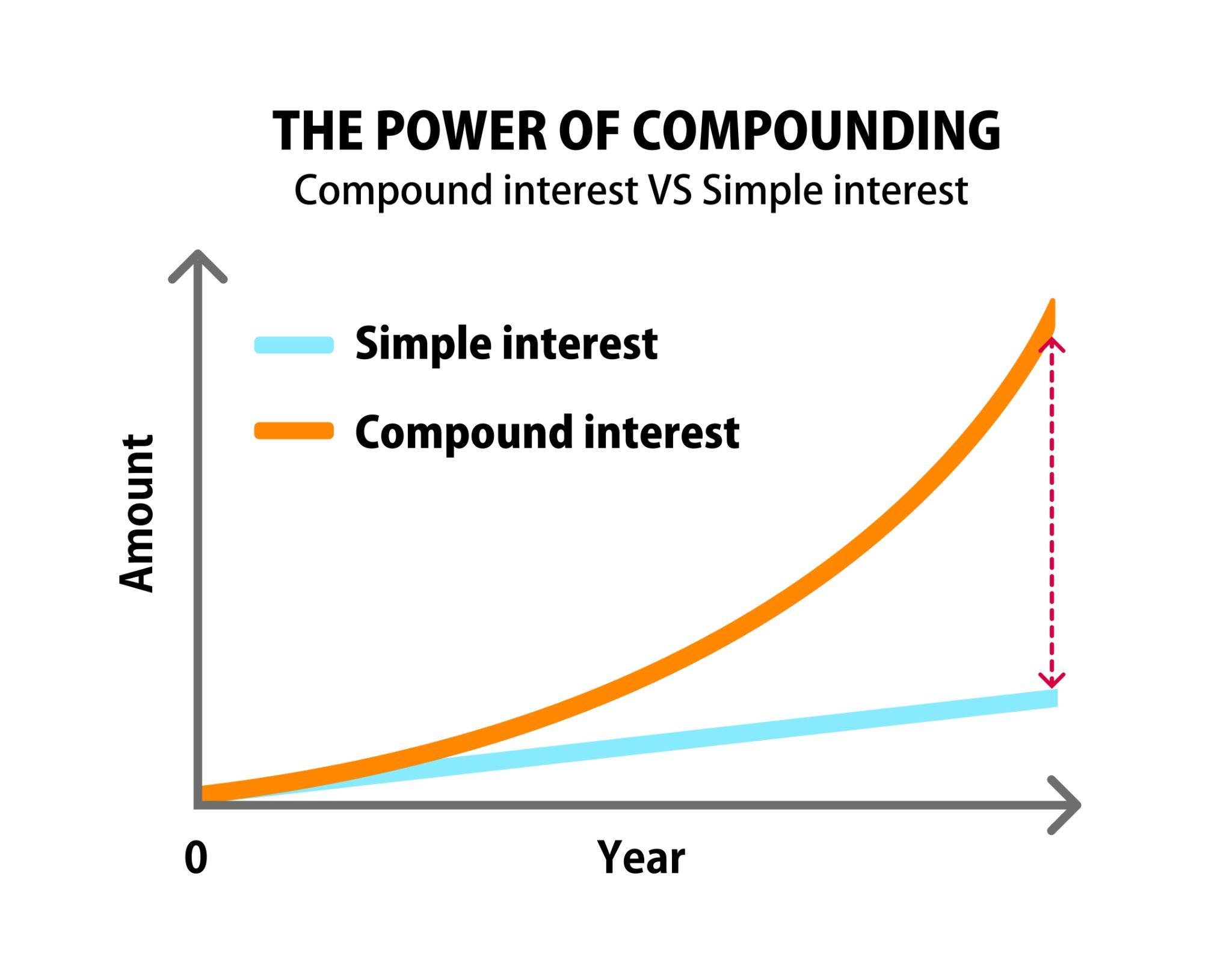

The most straightforward way to understand compound interest is to contrast it with simple interest. Simple interest is calculated solely on the principal amount, which is the initial sum of money deposited or loaned. For example, if you invest $1,000 at a 5% simple interest rate for five years, you would earn $50 in interest each year ($1,000 * 0.05). Over five years, your total interest earned would be $250, bringing your total to $1,250. The interest calculation always refers back to the original principal.

Compound interest, however, operates differently and far more powerfully. With compound interest, the interest earned in each period is added to the principal, and then the next period’s interest is calculated on this new, larger principal. Using the same example: if you invest $1,000 at a 5% compound annual interest rate, in the first year, you earn $50, bringing your total to $1,050. In the second year, the 5% interest is calculated not on the original $1,000, but on $1,050, yielding $52.50. Your new total becomes $1,102.50. This process continues, with each subsequent interest payment being slightly larger than the last, as it’s based on an ever-growing principal. This incremental growth, while seemingly small initially, accumulates rapidly over time, illustrating the “interest on interest” effect that defines compounding.

The Compounding Frequency and Its Impact

The frequency at which interest is compounded plays a significant role in how quickly your money grows. While our previous example used annual compounding for simplicity, interest can be compounded semi-annually, quarterly, monthly, daily, or even continuously. The more frequently interest is compounded, the faster your principal grows because interest is added to the principal more often, leading to earlier opportunities for that interest to start earning its own interest.

Consider an investment of $10,000 at an annual interest rate of 6% over five years:

- Annually compounded: Interest is added once a year.

- Monthly compounded: Interest is added 12 times a year. This means that after the first month, a small amount of interest is added to your principal, and then the next month’s interest is calculated on this slightly larger sum. This happens every month, leading to a marginally higher return than annual compounding over the same period, despite the same stated annual rate.

- Daily compounded: The effect is even more pronounced, albeit often to a smaller degree compared to the jump from annual to monthly.

While the difference might seem negligible over short periods, over decades, the impact of more frequent compounding can lead to substantially higher accumulated wealth. This is why financial products often highlight their compounding frequency, as it directly relates to the effective annual yield—the actual rate of return after accounting for compounding.

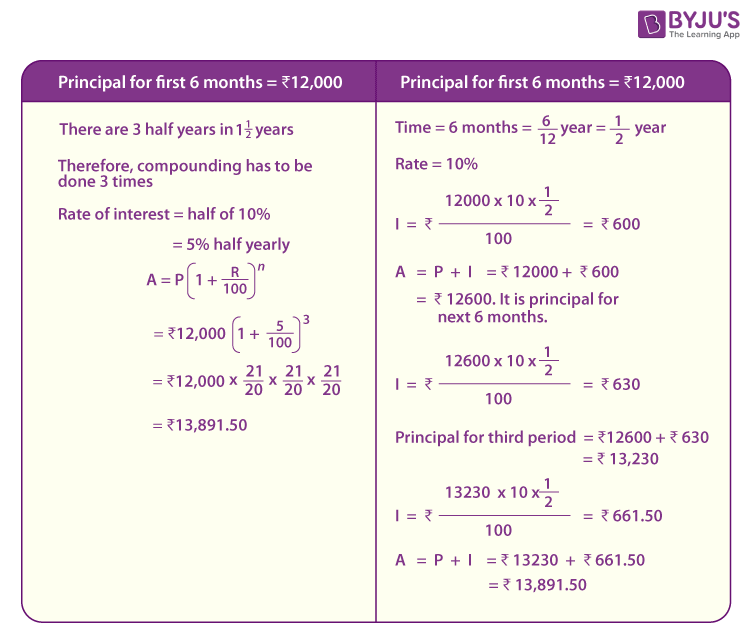

The Formula Behind the Magic

For those who appreciate the mathematical elegance, compound interest can be calculated using a specific formula, although a deep understanding of it isn’t strictly necessary to grasp the concept. The formula is:

A = P (1 + r/n)^(nt)

Where:

- A = the future value of the investment/loan, including interest

- P = the principal investment amount (the initial deposit or loan amount)

- r = the annual interest rate (as a decimal)

- n = the number of times that interest is compounded per year

- t = the number of years the money is invested or borrowed for

This formula mathematically encapsulates the “interest on interest” principle, demonstrating how the principal grows exponentially based on the interest rate, compounding frequency, and duration. For instance, a 5% annual rate compounded monthly (n=12) will yield a slightly higher return than a 5% annual rate compounded annually (n=1), simply because the interest is added to the principal more times within the year, allowing it to start earning additional interest sooner. Understanding these components helps in evaluating financial products and making choices that optimize for growth.

Why Compound Interest is a Wealth-Building Powerhouse

The true allure of compound interest lies not just in its definition, but in its profound implications for wealth creation. It’s the silent partner in every successful long-term financial strategy, turning modest consistent efforts into substantial riches.

The Power of Time: The Long-Term Advantage

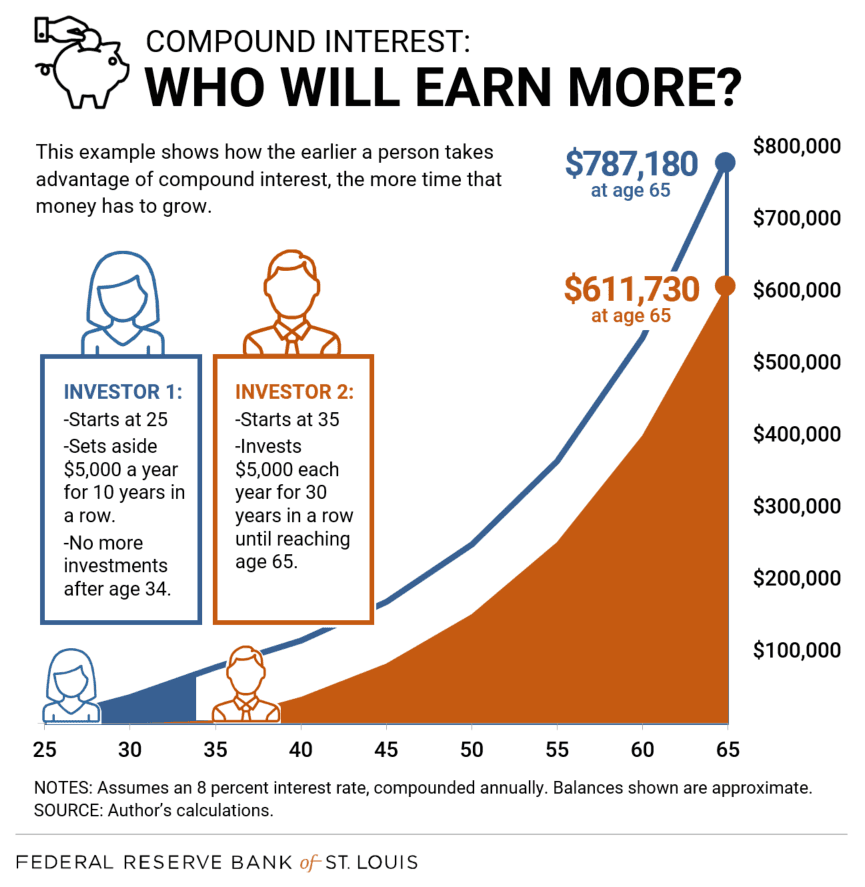

Perhaps the most critical factor in harnessing compound interest is time. The longer your money has to grow, the more pronounced the compounding effect becomes. This is often referred to as the “snowball effect”—a small snowball rolling down a hill gradually picks up more snow and gains momentum, becoming an avalanche. Similarly, initial investments, even small ones, accumulate interest which then earns interest, and over decades, this can result in truly remarkable sums.

Consider two individuals, Alice and Bob, both investing $5,000 annually at an average 7% return. Alice starts at age 25 and invests for 10 years, then stops, letting her money grow until age 65. Bob starts at age 35 and invests for 30 years, stopping at age 65. Despite Alice investing for a shorter period (10 years) and contributing less overall ($50,000) than Bob (30 years, $150,000), Alice’s final sum will likely be significantly larger. The early start gives her initial investments decades more time to compound, proving that the early bird truly gets the worm in the world of investing. This illustrates that starting early, even with smaller amounts, often outweighs starting later with larger contributions.

Reinvesting Returns: Fueling Exponential Growth

For compound interest to work its magic effectively, the returns generated must be reinvested. If you consistently withdraw the interest or dividends your investments earn, you are essentially converting your compound interest strategy into a simple interest one. Reinvesting means that any dividends from stocks, interest from bonds, or capital gains from mutual funds are used to purchase more shares or increase your principal, further accelerating the growth cycle.

For example, if you own dividend-paying stocks, opting for a dividend reinvestment plan (DRIP) means that instead of receiving cash payouts, your dividends are automatically used to buy more shares of the same stock. These new shares then go on to earn their own dividends, creating a self-perpetuating loop of growth. This strategy ensures that your “snowball” is continuously growing larger, ready to pick up even more snow on its next rotation. This discipline of reinvestment is a cornerstone for maximizing the exponential power of compounding.

Battling Inflation: Preserving and Growing Purchasing Power

In a world where the cost of living consistently rises due to inflation, simply saving money in a basic account that offers minimal interest can lead to a loss of purchasing power over time. If your savings earn 1% interest annually but inflation runs at 3%, your money is effectively losing value. Compound interest provides a crucial weapon in this battle.

By investing in assets that offer rates of return significantly higher than the inflation rate, and allowing those returns to compound, you can not only preserve your purchasing power but also grow it. For instance, historical average stock market returns have often outpaced inflation over long periods. Through compounding, these investments can generate enough growth to counteract the erosive effects of inflation, ensuring that your future self can afford more, not less. This makes compound interest an essential tool for securing long-term financial stability and achieving real growth beyond mere preservation.

Practical Applications: Leveraging Compound Interest in Your Financial Life

Understanding the mechanics and power of compound interest is one thing; applying it effectively across various aspects of your financial life is another. From retirement planning to managing debt, compound interest is a double-edged sword that can either build wealth or deplete it.

Retirement Savings: The Cornerstone of Long-Term Planning

Perhaps the most prominent application of compound interest is in retirement planning. Accounts like 401(k)s, IRAs, and Roth IRAs are specifically designed to maximize the benefits of long-term compounding. Contributions to these accounts, especially when made consistently over decades, grow exponentially due to compound interest and often tax advantages.

For example, contributing to a 401(k) allows your money to grow tax-deferred (or tax-free in a Roth 401(k)). This means the interest, dividends, and capital gains earned within the account are not taxed annually, allowing even more of your money to compound. An employer match in a 401(k) further supercharges this effect, as it’s essentially free money that immediately begins to compound alongside your contributions. The earlier you start contributing and the more consistently you do so, the larger your retirement nest egg will become, thanks to the magic of time and compounding.

Investment Portfolios: Stocks, Bonds, and Mutual Funds

Compound interest is the driving force behind the growth of diversified investment portfolios. Whether you invest in individual stocks, bonds, mutual funds, or exchange-traded funds (ETFs), the underlying principle for long-term growth is compounding.

- Stocks: Dividends received from stocks can be reinvested to purchase more shares, directly leveraging compound interest. Capital gains from stock price appreciation, when not realized and withdrawn, also contribute to the growing value of your principal.

- Bonds: Interest payments from bonds can be reinvested to buy more bonds or other assets, allowing the interest to earn additional interest.

- Mutual Funds/ETFs: These pooled investments automatically reinvest dividends and capital gains (unless you opt out), continuously growing your investment base.

A well-diversified portfolio held for the long term provides the ideal environment for compound interest to thrive, transforming relatively modest regular investments into significant wealth.

Debt Management: The Dark Side of Compounding

While compound interest is a powerful ally for saving and investing, it becomes a formidable adversary when it comes to debt, especially high-interest consumer debt like credit cards. Just as interest compounds on your savings, it also compounds on your outstanding debt. If you carry a balance on a credit card with an annual percentage rate (APR) of 20%, the interest you accrue in one month is added to your principal balance, and the next month’s interest is calculated on this larger sum. This leads to a rapidly increasing debt burden, making it incredibly difficult to pay off unless significant payments are made.

The strategy here is to reverse the compounding effect. Prioritizing the payoff of high-interest debt first is crucial. By eliminating these debts, you stop the compounding against you and free up funds that can then be directed towards savings and investments, where compound interest can work in your favor. Understanding the “negative compounding” of debt is just as vital as understanding the positive compounding of investments.

Educational Savings and Other Long-Term Goals

Beyond retirement, compound interest is an invaluable tool for funding other long-term financial goals, such as a child’s education, a down payment on a house, or starting a business.

- 529 Plans: These tax-advantaged savings plans for education allow investments to grow tax-free (at the federal level, and often state level) and are withdrawn tax-free for qualified educational expenses. The long time horizon before college enrollment provides ample opportunity for significant compounding.

- General Savings Accounts: Even for goals with a shorter but still substantial time horizon (e.g., 5-10 years), placing funds in accounts that offer a reasonable interest rate (like high-yield savings accounts or Certificates of Deposit) allows for some degree of compounding, helping your money grow beyond your direct contributions.

By consciously applying the principles of compound interest to these various life goals, individuals can significantly increase their chances of achieving them, turning aspirations into reality through disciplined saving and investing.

Strategies to Maximize the Power of Compounding

Harnessing compound interest isn’t just about understanding its mechanics; it’s about actively implementing strategies that allow it to flourish. Here are key approaches to ensure you’re making the most of this financial superpower.

Start Early, Stay Consistent

As previously discussed, time is the single most important variable in the compound interest equation. The longer your money is invested, the more periods it has to compound, leading to exponentially greater returns. This underscores the critical importance of starting to save and invest as early as possible. Even small contributions made in your 20s can often outperform much larger contributions made later in life due to this prolonged compounding advantage. Beyond starting early, consistency is key. Regularly contributing to your investments, even modest amounts, creates a steady stream of principal that can earn interest, continually feeding the compounding cycle. Automating your savings and investments, such as setting up automatic transfers from your checking account to your investment account, is an excellent way to ensure this consistency without relying on willpower alone.

Maximize Your Contributions

While starting early is paramount, maximizing your contributions whenever possible significantly amplifies the compounding effect. The larger the principal, the larger the interest earned in each period, leading to even faster growth. As your income grows throughout your career, aim to increase your savings rate. Take full advantage of employer-sponsored retirement plans like 401(k)s, especially if your employer offers a matching contribution—this is an immediate, guaranteed return on your investment that starts compounding from day one. Look for opportunities to save “extra” money, whether it’s from a bonus, a tax refund, or simply cutting back on discretionary spending, and direct those funds towards your investments. Every additional dollar contributed is another dollar that can start earning interest and compounding for your future.

Understand Compounding Frequencies and Rates

Not all financial products are created equal when it comes to compound interest. When choosing savings accounts, bonds, or other interest-bearing investments, pay close attention to the stated interest rate and the compounding frequency. A higher interest rate will, of course, lead to faster growth. However, a product that compounds daily or monthly at a slightly lower nominal annual rate might sometimes yield a better effective annual return than one that compounds annually at a slightly higher nominal rate. Always compare the “Annual Percentage Yield” (APY) for savings products, as APY accounts for the effect of compounding frequency and gives you the true annual rate of return. For loans, the “Annual Percentage Rate” (APR) tells you the total cost, including compound interest, which is important for understanding your debt obligations.

Be Patient and Avoid Emotional Decisions

The power of compound interest is a long-term game. Market fluctuations, economic downturns, and periods of low returns are inevitable. During these times, it can be tempting to panic, withdraw investments, or try to “time the market.” However, such emotional decisions often derail the compounding process. Frequent buying and selling incurs transaction costs and can lead to missing out on periods of recovery. For compound interest to truly work its magic, a long-term perspective and a steady hand are essential. Resist the urge to check your portfolio daily, and trust in the historical trend of markets to grow over extended periods. Patience, combined with a disciplined approach to saving and investing, will allow your wealth to compound effectively over decades, weathering short-term volatility to achieve substantial long-term growth.

Conclusion

Compound interest stands as one of the most powerful forces in personal finance, a true testament to the notion that steady effort and patience can yield extraordinary results. It transforms the modest act of saving into a dynamic engine of wealth creation, allowing your money to generate its own earnings and creating an accelerating cycle of growth. From building a comfortable retirement to funding a child’s education or simply growing a substantial emergency fund, the principle of earning “interest on interest” is indispensable.

Understanding its core mechanism, distinguishing it from simple interest, and recognizing the critical role of time and reinvestment are fundamental steps toward harnessing its potential. While it can be a formidable foe when leveraged against you in the form of high-interest debt, it is an unparalleled ally when applied to savings and investments. By starting early, staying consistent with contributions, maximizing savings when possible, and maintaining a patient, long-term perspective, anyone can unlock the profound benefits of compounding. Embrace this financial superpower, and you will lay a solid foundation for a prosperous and secure financial future, allowing your money to truly work for you.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.