In the intricate world of personal finance, certain numbers serve as silent architects, facilitating the seamless flow of money that underpins our modern economy. Among these, the “checking number” holds a paramount, though often unsung, position. While not a term you’ll typically find on official bank documents, it’s a common colloquialism for a critical piece of information: the Routing Transit Number (RTN). This nine-digit code is far more than just a sequence of digits; it is the unique identifier for your financial institution, an essential cog in the machinery that processes everything from your bi-weekly paycheck to your monthly utility bills.

Understanding your checking number, or RTN, is fundamental to managing your finances effectively in today’s digital age. It’s the key that allows funds to be directed to and from your bank with precision, preventing delays and misdirections that could otherwise disrupt your financial life. This article will delve into what the checking number truly is, where to locate it, its indispensable role in various transactions, and the crucial considerations surrounding its accuracy and security.

The Core Identity: Understanding the Routing Transit Number (RTN)

At its heart, a checking number is the unique identification code for your bank within the American financial system. While the term “checking number” might suggest it’s specific to your individual checking account, it actually identifies the financial institution itself, rather than your specific account.

What Exactly is an RTN?

The Routing Transit Number (RTN), often referred to as an ABA routing number (after the American Bankers Association, which established the system), is a nine-digit code that identifies the specific financial institution and its location where a payment originates or is received. Its primary purpose is to ensure that funds are transferred to the correct bank during transactions. Think of it as a postal code for your bank, directing mail (or in this case, money) to the right branch before your specific account number guides it to your personal mailbox.

This system was developed in 1910 by the American Bankers Association to facilitate the processing of paper checks. Each financial institution operating in the U.S. has at least one RTN, and larger banks, especially those with a national presence, may have multiple RTNs corresponding to different regions or types of transactions.

How RTNs Facilitate Money Movement

The RTN is a cornerstone of the Automated Clearing House (ACH) network, which is the primary system for electronic funds transfers in the United States. When you set up a direct deposit, pay a bill online, or transfer money between bank accounts, the RTN is used alongside your individual account number to ensure the funds reach the intended destination.

Without an RTN, the financial system would struggle to differentiate between thousands of banks and credit unions across the country. It acts as a critical intermediary, guiding the transaction to the correct institution before your unique account number then directs the funds to your specific account within that institution. This two-tiered identification system ensures both accuracy and security in a high-volume, complex financial environment.

Distinguishing RTN from Account Number

It’s crucial to understand the fundamental difference between your checking number (RTN) and your account number, as they serve distinct purposes and are both necessary for most financial transactions.

- Routing Transit Number (RTN): This is the bank’s identifier. It tells the financial system which bank to send the money to. It’s generally the same for all customers of a specific bank (or a specific branch/region of a larger bank) for a given type of transaction.

- Account Number: This is your specific account’s identifier. It tells your bank which individual account within their institution the money belongs to. This number is unique to your checking, savings, or other bank account.

To use an analogy, if you’re sending a letter, the RTN is akin to the city and state on the address, ensuring it arrives at the correct postal district. Your account number is then like the street name and house number, directing the letter to the precise recipient’s mailbox within that district. Both pieces of information are indispensable for successful delivery.

Where to Find Your Checking Number (RTN)

Locating your checking number (RTN) is usually straightforward, as banks make this information readily accessible given its necessity for various financial activities. There are several reliable places to find this nine-digit code.

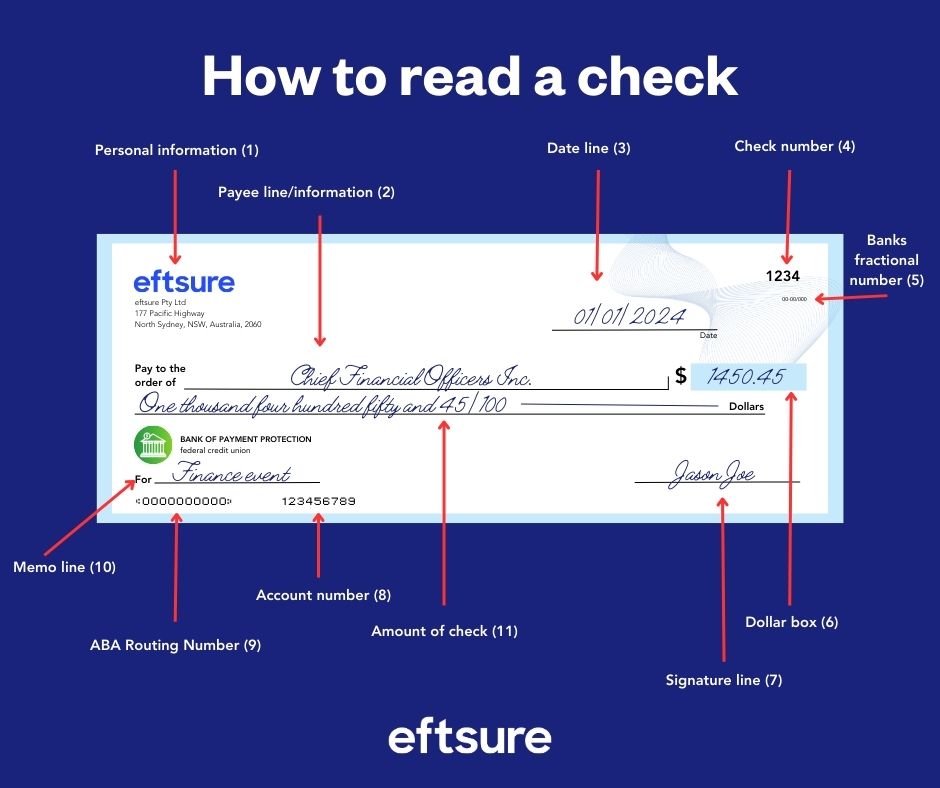

On Your Checks

The most traditional and perhaps easiest place to find your RTN is on a physical check. Look at the bottom of a personalized check. You will typically see three sets of numbers printed in magnetic ink (MICR — Magnetic Ink Character Recognition).

- The first set of numbers on the left (usually nine digits) is your Routing Transit Number (RTN).

- The middle set of numbers is your account number.

- The last set of numbers is the check number.

It’s important to note that the order of these numbers can sometimes vary, so always confirm with your bank if you’re unsure. However, the RTN is almost universally a nine-digit code.

Through Online Banking

In the age of digital finance, your online banking portal or mobile app is an excellent resource for finding your RTN.

- Log in to your online banking account.

- Navigate to your checking account details. This is often found under sections like “Account Summary,” “Account Information,” or “Direct Deposit Information.”

- Your RTN will typically be displayed prominently, often labeled as “Routing Number,” “ABA Routing Number,” or simply “Routing.”

Most banks also have a dedicated section for “Direct Deposit Forms” or “ACH Information” where both your routing and account numbers are clearly listed for easy setup with employers or payment providers.

Contacting Your Bank Directly

If you don’t have physical checks and cannot find the information through online banking, contacting your bank directly is always an option.

- Customer Service: Call your bank’s customer service line. After verifying your identity, they can provide you with the correct routing number for your account.

- Bank Statements: Your monthly bank statements, whether paper or digital, often include your routing number alongside your account number.

- Branch Visit: A visit to a local branch is another reliable way to obtain this information. A bank teller or representative can assist you.

Using the ABA Website (for Verification)

While not for initially finding your personal RTN, the American Bankers Association (ABA) website offers a lookup tool where you can verify routing numbers. This can be useful if you’ve been given an RTN and want to confirm its legitimacy or identify the bank it belongs to. However, always refer to your own bank’s official channels for the most accurate RTN specific to your account and transaction type.

The Critical Role of Your Checking Number in Financial Transactions

The checking number, or RTN, is an unsung hero in virtually every electronic financial transaction you conduct. Its accurate use is paramount for the smooth and timely processing of funds.

Direct Deposits: Seamless Income Flow

Perhaps the most common use of the RTN is for direct deposits. When your employer pays you, or a government agency (like the Social Security Administration or IRS) issues benefits, they require your bank’s routing number and your account number. This ensures that your earnings are deposited directly into your designated checking or savings account, eliminating the need for paper checks and offering instant access to your funds. Without the correct RTN, your paycheck could be delayed, returned, or even misdirected.

Automated Bill Payments: Convenience and Consistency

Setting up automated bill payments directly from your bank account relies heavily on your RTN. Whether it’s your mortgage, utilities, credit card bills, or subscription services, companies use your routing and account numbers to debit funds directly from your account on a recurring basis. This convenience helps avoid late payments and simplifies financial management, but it underscores the necessity of accurate banking details.

Wire Transfers: Domestic and International

Wire transfers, which are typically used for high-value or time-sensitive transactions, also depend on routing numbers. For domestic wire transfers, your bank’s RTN is used. For international wire transfers, an additional code, such as a SWIFT/BIC (Society for Worldwide Interbank Financial Telecommunication / Bank Identifier Code), often comes into play, which serves a similar purpose to an RTN but on a global scale. It’s important to note that some banks may have different routing numbers specifically for wire transfers versus standard ACH transactions, so always verify with your bank for these types of transactions.

Check Processing: The Original Use Case

While less common in daily life now, paper checks are still used. When you write a check, the printed RTN on the bottom left is read by specialized machines that identify your bank and facilitate the clearing process through the Federal Reserve system. The RTN ensures the check is routed to the correct institution for funds to be debited from your account and credited to the recipient’s bank. This was the original inspiration for the ABA routing number system and remains a fundamental function.

ACH Payments: The Backbone of Digital Transfers

Beyond direct deposits and bill payments, the RTN is the backbone of the Automated Clearing House (ACH) network, which processes a vast array of digital transfers. This includes peer-to-peer payments (e.g., sending money to a friend via a bank-linked app), electronic tax payments, refund disbursements, and electronic transfers between your own accounts at different financial institutions. Any time funds move electronically between U.S. bank accounts without a physical check or a wire transfer, an RTN is almost certainly involved.

Security, Accuracy, and Potential Pitfalls

While the checking number (RTN) is a robust and efficient system, understanding its nuances, ensuring accuracy, and practicing general security measures are crucial for seamless financial operations.

The Importance of Accuracy

Providing an incorrect RTN can lead to significant headaches. If you provide an incorrect routing number for a direct deposit, your funds could be delayed, returned, or even misdirected to the wrong bank. This can result in late fees, missed payments, or an inability to access your funds when needed. Banks typically charge fees for returned items due to incorrect information, adding to the frustration. Always double-check your routing and account numbers before initiating any new transaction or setting up recurring payments.

Safeguarding Your Information

While an RTN alone is not sufficient for fraudsters to access your account, it is still a piece of your financial puzzle. Combined with your account number, and especially your Social Security number, it could potentially be used for unauthorized transactions. It’s generally safe to share your RTN and account number with trusted entities like your employer or utility companies for legitimate transactions. However, always exercise caution with unsolicited requests for this information. Ensure you are dealing with reputable organizations and always use secure, encrypted platforms for sharing sensitive data. Regularly monitor your bank statements for any suspicious activity.

Understanding Different RTNs (e.g., Wire vs. ACH)

A lesser-known complexity is that some financial institutions, particularly larger ones, may have different routing numbers for different types of transactions or different geographical regions. For instance, the routing number used for direct deposits (ACH transactions) might be different from the one required for incoming wire transfers. Similarly, a bank with a national presence might have different routing numbers for different states. Always confirm the specific routing number required with your bank for the exact type of transaction you intend to make, especially for wire transfers, which are often irreversible.

What if Your Bank Changes Its RTN?

While not a frequent occurrence, banks can occasionally change their routing numbers. This typically happens in the event of mergers, acquisitions, or significant internal system reorganizations. When such a change occurs, your bank is legally obligated to notify you well in advance. It is critical to update any entities that have your old routing number on file (e.g., employers for direct deposit, utility companies for bill pay) to prevent disruptions in your financial flow. Ignoring these notifications can lead to payment failures and administrative complications.

In conclusion, the checking number, or Routing Transit Number, is a seemingly simple nine-digit code that plays an extraordinarily complex and vital role in the mechanics of modern finance. It is the fundamental identifier for your financial institution, enabling the secure and efficient movement of funds across the vast network of banks and credit unions. From receiving your salary to paying your bills, the RTN is the invisible hand guiding your money to its correct destination. By understanding what it is, where to find it, and its critical importance, you empower yourself to navigate your personal finances with greater confidence, accuracy, and security in an increasingly digital world. Always keep your financial information accurate and protected, ensuring your checking number continues to serve its silent, indispensable purpose.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.