In the landscape of personal finance, investors often find themselves caught between the desire for high returns and the fundamental need for capital preservation. While the stock market offers long-term growth potential, its volatility can be a deterrent for those with specific short-term goals or a low risk tolerance. This is where the Certificate of Deposit, or CD, becomes an essential tool in a well-rounded financial strategy. Often viewed as the “slow and steady” engine of a savings plan, a CD provides a predictable, low-risk way to grow your money, backed by federal protections that ensure your principal remains safe.

Understanding the Fundamentals of Certificates of Deposit

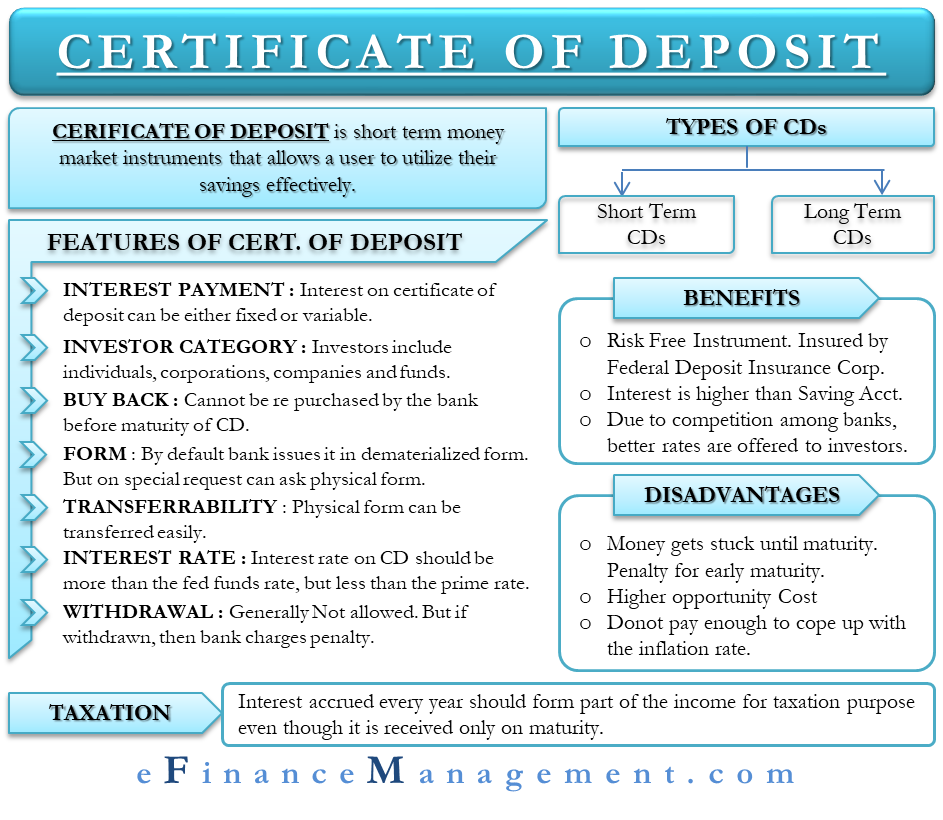

A Certificate of Deposit is a type of savings account offered by banks and credit unions that holds a fixed amount of money for a fixed period of time—such as six months, one year, or five years. In exchange for leaving your money untouched for that duration, the issuing institution pays you a higher interest rate than you would typically find in a standard savings account.

How a CD Works: The Financial Contract

When you open a CD, you are essentially entering into a legal agreement with a financial institution. You agree to “lend” the bank your money for a specified term. In return, the bank agrees to pay you a fixed rate of interest for the life of the term and return your original principal at the end. This is a departure from a traditional savings account, where you can withdraw funds at any time but the interest rate can fluctuate based on market conditions.

Key Terminology: Principal, APY, and Maturity

To navigate the world of CDs, one must understand three core components:

- Principal: The initial amount of money you deposit.

- Annual Percentage Yield (APY): This represents the real rate of return on your deposit, accounting for the effect of compounding interest over the year.

- Maturity Date: The day the CD term ends. On this date, you gain full access to your funds and the interest earned without penalty.

The Role of FDIC and NCUA Insurance

The primary appeal of a CD is its near-absolute safety. In the United States, CDs opened at banks are insured by the Federal Deposit Insurance Corporation (FDIC), while those at credit unions are insured by the National Credit Union Administration (NCUA). Both provide coverage up to $250,000 per depositor, per insured institution, for each account ownership category. This means that even if the bank were to fail, your investment is protected by the full faith and credit of the U.S. government.

Exploring the Diverse Types of CDs

Not all CDs are created equal. As the financial market has evolved, banks have introduced various “flavors” of CDs to cater to different investor needs regarding liquidity, interest rate movements, and deposit sizes.

Standard and High-Yield CDs

The most common type is the fixed-rate CD. You lock in a rate at the beginning, and it remains the same until the maturity date. High-yield CDs are essentially the same but are usually offered by online banks that have lower overhead costs than brick-and-mortar institutions, allowing them to pass on higher interest rates to the consumer.

Specialized Structures: Bump-Up, Step-Up, and No-Penalty

For investors worried about rising interest rates, Bump-Up CDs allow you to request a one-time rate increase if the bank’s rates go up during your term. Step-Up CDs have a pre-scheduled interest rate increase built into the term.

On the other hand, No-Penalty CDs address the primary drawback of these accounts: liquidity. A no-penalty CD allows you to withdraw your full balance and earned interest before the maturity date without paying an early withdrawal fee, though they typically offer slightly lower interest rates than their traditional counterparts.

Jumbo CDs and Brokered CDs

Jumbo CDs require a significantly higher minimum deposit—often $100,000 or more. In exchange for this large capital commitment, the bank may offer a premium interest rate. Brokered CDs are purchased through a brokerage firm rather than directly from a bank. These are often traded on the secondary market, which means you might be able to sell them if you need your money back early, though the price you get will depend on current market interest rates.

The Mechanics of CD Investing: Rates and Penalties

Investing in a CD requires more than just picking the highest rate. It involves understanding how interest is calculated and what happens if your financial circumstances change unexpectedly.

How Interest Rates Are Determined

CD rates are largely influenced by the Federal Reserve’s federal funds rate. When the Fed raises rates to combat inflation, CD rates typically follow suit. Conversely, in a low-rate environment, CD yields may drop. Generally, the longer the term of the CD, the higher the interest rate, as the bank is rewarding you for committing your capital for a longer period.

Navigating the Early Withdrawal Penalty (EWP)

The “catch” of a CD is the early withdrawal penalty. If you need to access your principal before the maturity date, the bank will charge a fee. This penalty is often calculated as a specific number of months’ worth of interest (e.g., six months of interest for a two-year CD). In some cases, if you withdraw very early, the penalty could even eat into your original principal. This makes CDs unsuitable for emergency funds that you might need to access on short notice.

The Strategic Value of CD Laddering

To mitigate the risks of interest rate fluctuations and lack of liquidity, many savvy investors use a strategy called “CD Laddering.” Instead of putting $50,000 into a single five-year CD, you might put $10,000 into five different CDs with terms of one, two, three, four, and five years.

Each year, one CD matures, providing you with cash flow or the opportunity to reinvest at current market rates. This ensures that you are never more than a year away from a portion of your money while still benefiting from the higher rates offered by longer-term certificates.

Comparing CDs to Other Financial Instruments

To determine if a CD belongs in your portfolio, it is helpful to compare it against other common “cash-equivalent” or low-risk investments.

CDs vs. High-Yield Savings Accounts (HYSA)

The main difference is flexibility. An HYSA allows for frequent withdrawals and has a variable interest rate. If rates rise, your HYSA rate goes up immediately. If they fall, your return drops. A CD locks your rate in. Therefore, CDs are better when you believe interest rates will fall in the future, while HYSAs are better for money you might need next month.

CDs vs. Money Market Accounts (MMA)

Money Market Accounts are a hybrid between savings and checking accounts. They often come with debit cards or check-writing privileges but offer rates competitive with savings accounts. Compared to CDs, MMAs offer much more liquidity but usually lower interest rates than a long-term CD.

CDs vs. Treasury Bonds

Treasury bonds are backed by the U.S. Treasury and are also considered extremely safe. While CD interest is subject to federal and state taxes, interest from Treasury bonds is exempt from state and local taxes. This “tax-equivalent yield” can sometimes make Treasuries more attractive for investors in high-tax states, even if the nominal CD rate is slightly higher.

Is a CD Right for Your Financial Strategy?

Deciding to open a CD depends on your specific financial goals and your timeline. It is not a “get rich quick” scheme, but rather a “keep what you have” strategy.

Pros and Cons Summary

Pros:

- Guaranteed Returns: You know exactly how much you will earn.

- Safety: FDIC/NCUA insurance protects against bank failure.

- Encourages Discipline: The penalty for early withdrawal discourages “dipping into” savings for impulse purchases.

Cons:

- Liquidity Risk: Your money is locked away for a set period.

- Inflation Risk: If inflation rises faster than your CD’s interest rate, your “real” purchasing power may actually decrease over time.

- Fixed Returns: You won’t benefit if market interest rates skyrocket after you’ve locked in your rate.

When to Choose a CD

A CD is an ideal choice for money earmarked for a specific purchase in the near future—such as a house down payment in two years, a wedding next year, or a car purchase. It is also an excellent tool for retirees who need a portion of their portfolio to be shielded from stock market downturns while still generating a modest income.

In conclusion, the Certificate of Deposit remains a cornerstone of conservative personal finance. While it may lack the excitement of equity trading or the flexibility of a standard savings account, its unique combination of predictable growth and government-backed security makes it an invaluable asset. By understanding the different types of CDs and employing strategies like laddering, you can build a financial cushion that protects your principal while ensuring your money is working as hard as possible in a low-risk environment.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.