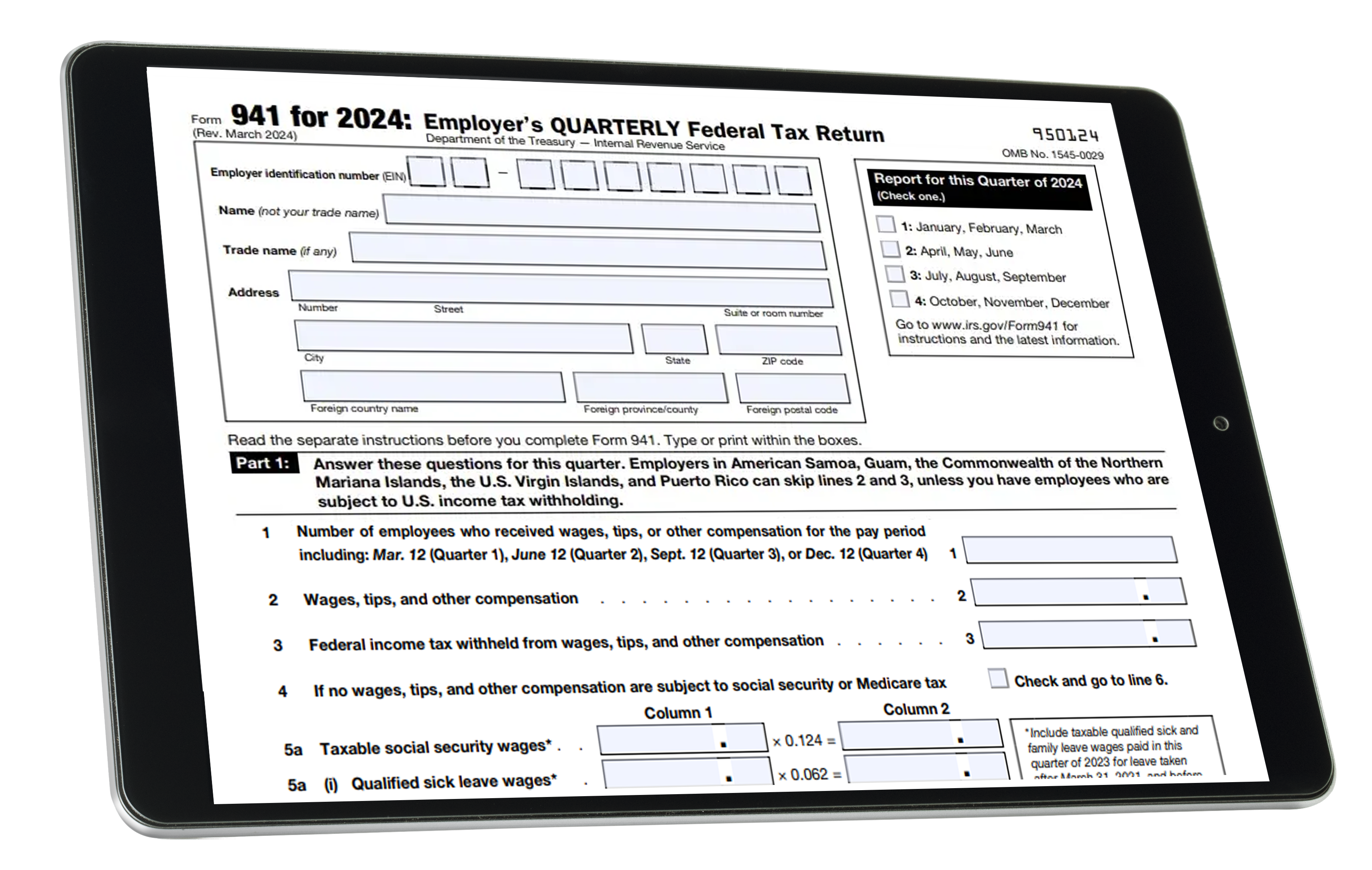

Navigating the landscape of business finance requires a keen understanding of various regulatory requirements, none of perhaps more critical than payroll tax compliance. For any business owner with employees, Form 941, officially titled the Employer’s Quarterly Federal Tax Return, is a cornerstone of financial reporting. This document is the primary mechanism through which the Internal Revenue Service (IRS) tracks the movement of income taxes and payroll taxes from the private sector to the federal treasury. Understanding the nuances of Form 941 is not just about legal compliance; it is a vital component of managing business cash flow and maintaining financial integrity.

Understanding the Basics of Form 941

At its core, Form 941 is the report card of a business’s payroll activities over a three-month period. While many business taxes are handled annually, the federal government requires a more frequent pulse check on payroll-related funds to ensure that taxes withheld from employees are being properly accounted for and remitted.

Definition and Purpose

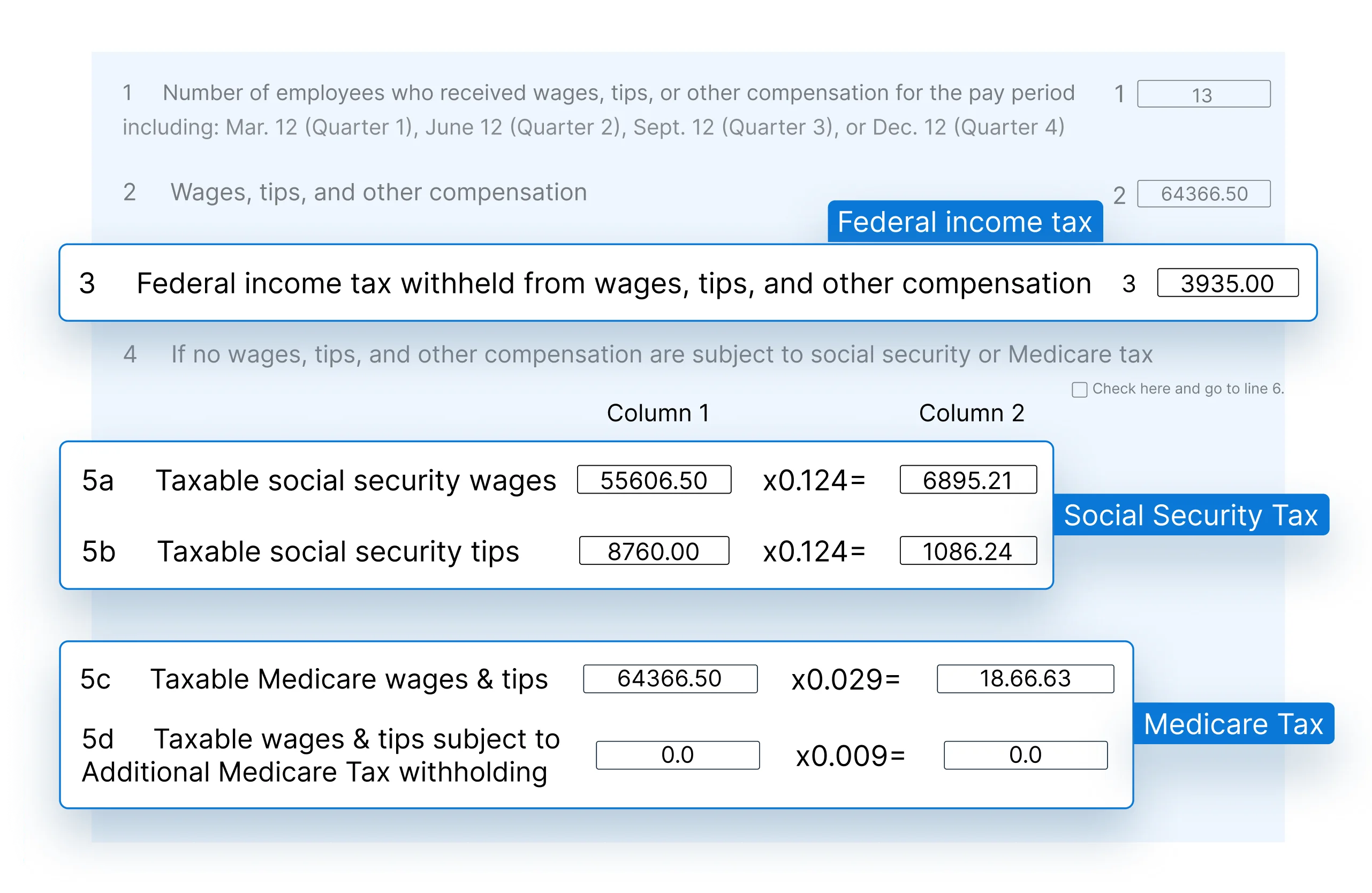

Form 941 is used by employers to report income taxes, Social Security tax, and Medicare tax withheld from employee wages. Furthermore, it is the document used to calculate the employer’s portion of Social Security and Medicare taxes. The purpose is two-fold: it provides the IRS with a record of the total wages paid and ensures that the amount of tax withheld matches the amount deposited by the company throughout the quarter. Because these funds are often referred to as “trust fund taxes”—meaning the employer holds them in trust for the government—the IRS monitors this form with high scrutiny.

Who is Required to File?

Generally, if you pay wages to an employee, you are required to file Form 941 every quarter. This applies even if you have no taxes to report for a specific quarter, as long as you are still in business and have not filed a final return. There are very few exceptions to this rule. Seasonal employers only file for quarters in which they paid wages, and very small businesses (those with an annual liability of $1,000 or less in payroll taxes) may be permitted to file Form 944 annually instead. However, for the vast majority of American enterprises, Form 941 is a non-negotiable quarterly obligation.

Key Components of the Form

Form 941 is divided into several sections that demand precise mathematical accuracy. It asks for the total number of employees paid during the quarter, the total wages paid, and the specific amounts of federal income tax withheld. It also includes sections for “adjustments,” which allow for minor corrections due to rounding or sick pay, and a section for the “Qualified Small Business Payroll Tax Credit for Increasing Research Activities,” which can be a significant financial boon for tech-heavy startups or innovative firms.

Financial Implications and Withholding Requirements

From a financial management perspective, Form 941 represents a significant portion of a company’s tax liability. It is not merely a reporting document; it is a calculation of the debt the business owes to the federal government.

Social Security and Medicare Taxes

Commonly referred to as FICA (Federal Insurance Contributions Act) taxes, these are split between the employer and the employee. As of current regulations, the Social Security tax rate is 6.2% for the employer and 6.2% for the employee, totaling 12.4% on wages up to a specific annual limit known as the wage base. Medicare tax is 1.45% for each party, totaling 2.9%. On Form 941, the employer must report both the employee’s share that was withheld and the employer’s matching share. This means for every dollar an employee contributes to these social safety nets, the business must also contribute a dollar, making payroll a significant expense beyond just the gross salary.

Federal Income Tax Withholding

Unlike FICA taxes, federal income tax is borne entirely by the employee, but the responsibility for its collection and reporting lies with the employer. The amount withheld is based on the information provided by the employee on their Form W-4. On Form 941, the employer aggregates these withholdings. Failure to report these accurately can lead to a “mismatch” in the IRS system, triggering audits that can disrupt business operations and financial planning.

The Role of the Employer’s Share

It is a common misconception among new entrepreneurs that their tax obligation is limited to what they take out of an employee’s paycheck. In reality, the employer’s share of Social Security and Medicare taxes is a direct business expense. This cost must be factored into the “total cost of labor” when budgeting. For a business with a $1,000,000 annual payroll, the employer’s share of FICA taxes alone can exceed $76,500. Form 941 is the crucible where these figures are finalized each quarter, directly impacting the company’s bottom line and net income.

The Filing Timeline and Compliance Procedures

Consistency is the hallmark of effective financial administration. The IRS operates on a strict quarterly schedule for Form 941, and missing these dates can result in compounding financial friction.

Critical Deadlines for Quarterly Filing

The tax year is divided into four quarters:

- Q1 (Jan–Mar): Due April 30

- Q2 (Apr–Jun): Due July 31

- Q3 (Jul–Sep): Due October 31

- Q4 (Oct–Dec): Due January 31

If the due date falls on a weekend or legal holiday, the return is due on the next business day. It is important to note that the deadline for filing the form is different from the deadline for depositing the taxes, which often occurs much more frequently.

Methods of Submission: E-filing vs. Paper

The IRS strongly encourages electronic filing (e-file) for Form 941. E-filing is generally more secure, results in fewer errors, and provides an immediate receipt of confirmation. Most modern payroll software platforms handle this automatically. For those who still prefer manual processes, paper forms can be mailed to specific IRS addresses based on the state where the business is located and whether a payment is included with the return. However, in an era of digital business finance, paper filing is increasingly seen as an inefficient practice that increases the risk of data entry errors.

Payment Schedules: Monthly vs. Semi-weekly Deposits

While Form 941 is filed quarterly, the actual money must usually be sent to the IRS more often. Your deposit schedule is determined by the total tax liability you reported on Form 941 during a previous “lookback period.”

- Monthly depositors must deposit taxes for a given month by the 15th day of the following month.

- Semi-weekly depositors deposit taxes based on the day of the week the payroll was paid.

Understanding which schedule your business falls under is crucial for maintaining liquidity. If a business fails to deposit the funds correctly, the Form 941 filed at the end of the quarter will show a discrepancy, leading to immediate penalties.

Avoiding Penalties and Common Financial Pitfalls

The IRS is particularly aggressive regarding payroll taxes because a portion of the money belongs to the employees. Mismanagement in this area is viewed not just as a tax error, but as a failure of the business to act as a proper fiduciary.

Late Filing and Payment Penalties

The financial consequences of missing a Form 941 deadline are steep. The penalty for filing late is generally 5% of the tax due for each month or part of a month the return is late, capped at 25%. Additionally, there is a penalty for late payment, which is usually 0.5% of the unpaid tax amount per month, also capped at 25%. These penalties, combined with accruing interest, can quickly snowball, turning a manageable tax bill into a significant financial crisis.

Accuracy and Reconciliation (Form 941 vs. W-2)

At the end of the fiscal year, the IRS compares the totals reported on your four quarterly Form 941s with the totals reported on the annual Form W-3 (which summarizes all employee W-2s). If these numbers do not match, it triggers an inquiry. Common errors include failing to account for taxable fringe benefits, miscalculating the Social Security wage base limit, or simple data entry mistakes. Regular reconciliation—checking your numbers every month—is a vital financial habit that prevents year-end headaches.

Adjustments and Corrections (Form 941-X)

If you discover an error after you have already filed your Form 941, you must use Form 941-X, the Adjusted Employer’s Quarterly Federal Tax Return or Claim for Refund. This form allows you to correct underreported or overreported taxes. From a cash flow perspective, if you overpaid, filing a 941-X can result in a credit toward future tax liabilities or a refund, which can be reinvested into the business.

Best Practices for Modern Business Finance Management

In the modern economy, managing Form 941 compliance should not be a manual, stressful task. Leveraging technology and expertise can turn a bureaucratic requirement into a streamlined part of your financial workflow.

Utilizing Payroll Software for Accuracy

The most effective way to manage Form 941 is through automated payroll systems. Modern software calculates withholdings in real-time, tracks changing tax rates, and handles the electronic filing and payment deposits automatically. This reduces the “human error” factor significantly. For a business, the cost of a payroll subscription is often much lower than the cost of a single IRS penalty for a misfiled return.

Record Keeping and Audit Readiness

The IRS recommends that businesses keep all payroll tax records for at least four years. This includes copies of filed Form 941s, records of tax deposits, employee W-4 forms, and documentation of any credits claimed. In the event of a financial audit, having a clean, organized digital trail of your 941 filings demonstrates professional management and can significantly shorten the audit process.

Professional Consultation and Outsourcing

As a business grows, its tax situation often becomes more complex, involving multi-state employees or complex benefit structures. In such cases, consulting with a Certified Public Accountant (CPA) or a dedicated tax professional is a wise financial move. They can provide insights into tax-saving credits that might be reported on Form 941, such as the Employee Retention Credit (ERC) or other stimulus-related incentives, ensuring that the business is not only compliant but also tax-efficient.

Form 941 is more than just a piece of paperwork; it is a vital instrument in the financial symphony of a healthy business. By understanding its requirements, staying ahead of deadlines, and utilizing the right tools, business leaders can ensure that their payroll obligations are met with precision, protecting the company’s capital and its reputation with the federal government.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.