The journey of a startup is often paved with innovation, ambition, and, crucially, equity. As companies grow, the value of their stock can skyrocket, presenting significant financial opportunities for those who are instrumental in their success. However, the way equity is taxed can have a profound impact on an individual’s net gains. This is where an 83(b) election, a provision under Section 83(b) of the U.S. Internal Revenue Code, comes into play. It’s a strategic financial decision that can significantly alter the tax implications of receiving stock that is subject to a substantial risk of forfeiture.

For founders, early employees, and investors in private companies, understanding the 83(b) election is not just beneficial; it can be a game-changer. It allows individuals to pay taxes on the current, often lower, fair market value of their stock rather than waiting until the stock vests and its value has potentially increased dramatically. This article delves into the intricacies of the 83(b) election, its benefits, drawbacks, and the critical considerations for making this important financial decision.

Understanding the Core of Section 83(b) and Restricted Stock

At its heart, Section 83 of the Internal Revenue Code governs the taxation of property transferred in connection with the performance of services. This commonly applies to stock options and restricted stock awards (RSAs) granted to employees, founders, or service providers. The key concept here is “substantial risk of forfeiture.”

Restricted Stock Awards (RSAs) and Forfeiture

When a company grants stock as part of compensation, it’s often not immediately fully yours. It may be “restricted” for a period, meaning you could lose it if certain conditions aren’t met. This is known as a substantial risk of forfeiture. A common example is vesting, where you earn the right to your stock over time, typically tied to continued employment or company milestones.

Vesting Schedules: Most RSAs have vesting schedules. For instance, a grant might vest over four years, with a one-year cliff. This means you receive 25% of your stock after one year of employment, and the remaining 75% vests ratably over the next three years. If you leave the company before you are fully vested, you forfeit the unvested portion of your stock.

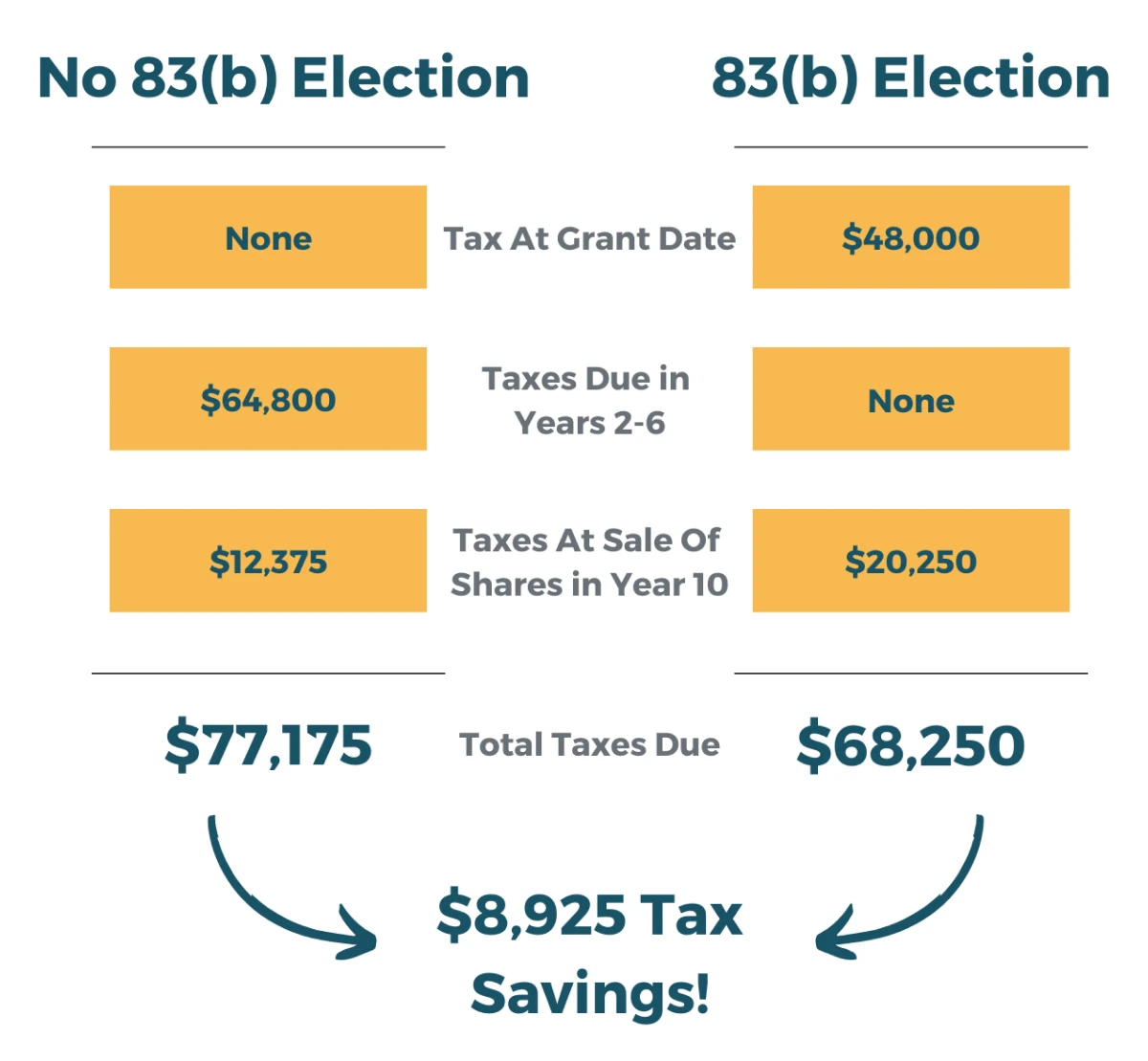

Taxation Without an 83(b) Election: If you do not make an 83(b) election, the IRS will tax you on the fair market value (FMV) of the stock at the time it vests. At vesting, the stock is no longer subject to the substantial risk of forfeiture, meaning it is now considered fully taxable income. The difference between the FMV at vesting and any amount you paid for the stock (if anything) becomes ordinary income, subject to income tax rates. Any appreciation in the stock’s value after vesting is then treated as a capital gain when you eventually sell the stock. Capital gains typically have more favorable tax rates than ordinary income.

The Role of the 83(b) Election

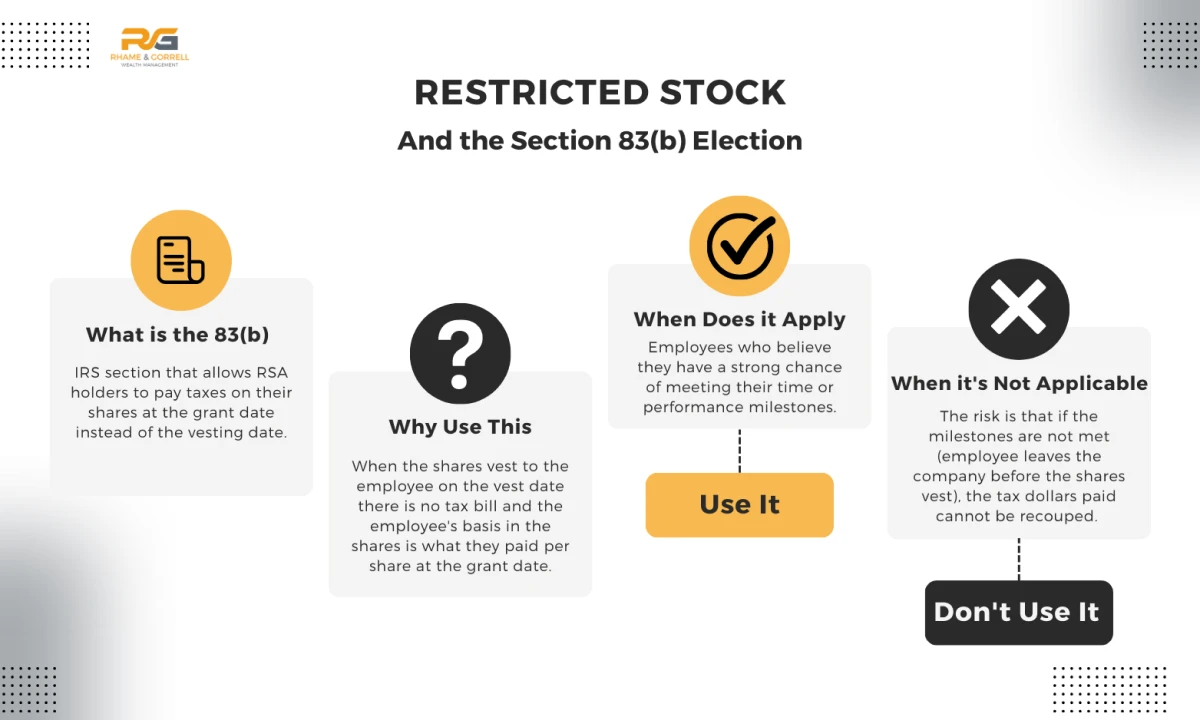

An 83(b) election allows you to elect to be taxed on the value of the restricted stock at the time it is granted, rather than at the time it vests. This means you are essentially treating the stock as fully owned from the moment of the grant, even though there might still be a substantial risk of forfeiture.

How it Works: To make an 83(b) election, you must file a specific election statement with the IRS. This election must be filed within 30 days of the date you receive the restricted stock. This is a strict deadline, and missing it means you cannot make an 83(b) election for that specific grant.

Taxation With an 83(b) Election: If you make a timely 83(b) election, you will pay ordinary income tax on the difference between the fair market value of the stock on the grant date and any amount you paid for it. This tax is based on the stock’s value at the beginning of the journey. Once this tax is paid, the stock is no longer subject to ordinary income tax upon vesting. Any future appreciation in the stock’s value from the grant date until you sell it will be treated as a capital gain, taxed at potentially lower capital gains rates.

The Advantages of Making an 83(b) Election

The primary allure of the 83(b) election lies in its potential to significantly reduce future tax burdens, especially in high-growth startup environments.

Capturing Lower Initial Valuation for Tax Purposes

Startups, particularly in their early stages, typically have a very low fair market value for their stock. This is because the company is still developing its product, finding its market, and has not yet achieved significant revenue or profitability. By making an 83(b) election, you pay taxes on this low initial valuation.

Example: Imagine you receive 100,000 shares of stock when a startup is valued at $0.10 per share.

- Without 83(b): If your stock vests over four years, and by the time it vests, the company is valued at $5.00 per share, you will owe ordinary income tax on $4.90 per share ($5.00 FMV – $0.10 purchase price). For 100,000 shares, this is $490,000 in income.

- With 83(b): If you make an 83(b) election, you pay ordinary income tax on $0.10 per share ($0.10 FMV – $0.00 purchase price). For 100,000 shares, this is $10,000 in income. The remaining appreciation to $5.00 per share would be subject to capital gains tax.

This dramatic difference highlights the power of locking in the low initial valuation.

Shifting Taxation to Capital Gains

As mentioned, capital gains are often taxed at lower rates than ordinary income. By paying taxes on the initial low value, any subsequent growth in the stock’s value is treated as capital appreciation. When you eventually sell your vested shares, the profit (the difference between the sale price and the fair market value on the grant date) will be taxed as a capital gain. This can lead to substantial tax savings over the long term, particularly if the company experiences significant growth.

Long-Term vs. Short-Term Capital Gains: The tax rate on capital gains depends on how long you have held the asset. Gains on assets held for more than one year are considered long-term capital gains and are taxed at preferential rates. Gains on assets held for one year or less are short-term capital gains and are taxed at ordinary income rates. Making an 83(b) election effectively “starts the clock” on your holding period for capital gains purposes from the grant date, ensuring that any appreciation upon sale will benefit from long-term capital gains treatment.

Mitigating Future Tax Surprises

The growth trajectory of a startup is inherently unpredictable. Without an 83(b) election, you face the risk of a substantial tax liability upon vesting, especially if the company has experienced rapid growth. This tax bill could come at a time when you don’t have liquid assets to pay it, forcing you to sell stock prematurely or take on debt. An 83(b) election allows for a more predictable tax event upfront, enabling better financial planning.

Critical Considerations and Potential Drawbacks

While the 83(b) election offers compelling advantages, it’s not a one-size-fits-all solution. There are significant risks and considerations to weigh before making this decision.

The Risk of Forfeiture

The most significant drawback is the risk of forfeiture. If you make an 83(b) election and pay taxes on the stock, but then you forfeit that stock (e.g., you leave the company before it vests), you will have paid taxes on income you never actually received. In such a scenario, you can claim a capital loss on your tax return for the amount you paid for the stock and the taxes you paid. However, this doesn’t recoup the full value, and it’s still a loss.

Example: You pay $1,000 for stock with a grant-date FMV of $10,000 and make an 83(b) election. You pay ordinary income tax on $9,000. If you then forfeit the stock due to termination, you’ve lost the $1,000 purchase price and paid taxes on $9,000 of income. You can claim a capital loss for the $1,000.

Immediate Tax Liability

The 83(b) election requires you to pay taxes on the stock’s value at the time of the grant, even if that value is currently theoretical or if the stock is illiquid. This means you could face an immediate tax bill at a time when you may not have significant disposable income, especially if you are an early employee or founder.

Cash Flow Management: It’s crucial to assess your personal financial situation and ensure you have the liquidity to cover the tax liability. If the stock is not publicly traded, you might need to sell some of your vested shares or use other assets to pay the tax.

Illiquid Stock and Valuation Challenges

For private companies, determining the fair market value (FMV) of the stock on the grant date can be challenging. The IRS requires that the FMV be “reasonable.” Companies often hire third-party valuation firms to conduct independent valuations, especially for more established startups. However, in the very early stages, valuations can be more subjective.

Accuracy of Valuation: If the IRS later determines that the FMV used for the 83(b) election was significantly underestimated, you could face an audit, back taxes, penalties, and interest. It’s important to ensure that the valuation used is well-supported and defensible.

Company Exit and Liquidation Preferences

Even if the company is successful, the actual cash you receive upon an exit event (like an acquisition or IPO) can be affected by liquidation preferences. Investors who put capital into the company often have liquidation preferences, meaning they get their money back (and sometimes a multiple of it) before common stockholders receive anything. This can reduce the actual payout for common stockholders, and thus the effective gain you receive. While an 83(b) election taxes you on the theoretical value, the actual realized value at exit might be different due to these structures.

The Process of Making an 83(b) Election

Executing an 83(b) election involves specific steps and adherence to strict deadlines.

Filing Requirements and Deadlines

The 30-Day Rule: The absolute, non-negotiable deadline for filing an 83(b) election is within 30 days of the date you receive the restricted stock. This date is typically the date the stock is legally transferred to you, not necessarily the date you sign the agreement or when it vests. It is critical to identify this date precisely.

IRS Form 83(b): The election is made by filing IRS Form 83(b), “Election to Defer Recognition of Gain or Loss by Recipient of Property Transferred in Connection with Performance of Services,” with the IRS. You must include:

- Your name, address, and Social Security number.

- A description of the property (the stock).

- The date you received the property.

- The date the property is transferable and not subject to a substantial risk of forfeiture (the vesting date).

- The fair market value of the property at the time of transfer.

- The amount you paid for the property.

- A statement that you are electing under Section 83(b).

Delivery Method: You can file the form by mailing it to the IRS, or in some cases, electronically. It is highly recommended to send it via certified mail with a return receipt requested to have proof of timely filing.

Importance of Consulting Professionals

Given the complexity and financial implications, it is strongly advised to consult with qualified professionals before making an 83(b) election.

Tax Advisors: A tax advisor or CPA specializing in startup equity can help you:

- Determine the fair market value of your stock on the grant date.

- Calculate the potential tax liability associated with the election.

- Analyze the long-term tax implications based on your personal financial situation and projected company growth.

- Ensure the election is filed correctly and on time.

Legal Counsel: An attorney specializing in corporate and securities law can:

- Review the terms of your stock grant and ensure you understand the forfeiture provisions.

- Advise on the legal implications of the election within the context of your employment or founder agreement.

What Happens If You Don’t Make an 83(b) Election?

If you decide not to make an 83(b) election, the default tax treatment under Section 83 will apply. This means you will recognize ordinary income upon the vesting of your restricted stock, based on the fair market value of the stock at that time, less any amount you paid for it. All appreciation prior to vesting will be taxed as ordinary income, and any appreciation from vesting until sale will be taxed as capital gains.

Who Should Consider an 83(b) Election?

The decision to make an 83(b) election is highly personal and depends on several factors, but it is most commonly considered by:

Founders of Early-Stage Companies

Founders are often the first to receive equity and typically do so when the company’s valuation is at its lowest. The potential upside for founders is immense, making an 83(b) election a powerful tool for long-term wealth creation, provided the company achieves success.

Early Employees of High-Growth Startups

Employees who join a startup in its nascent stages often receive significant equity grants with substantial vesting periods. If the company is poised for rapid growth and a potentially lucrative exit, locking in the current low valuation through an 83(b) election can be a strategic move to defer taxes and benefit from capital gains treatment on future appreciation.

Investors in Early-Stage Ventures

Angel investors and early venture capital investors who receive stock or warrants in exchange for their investment may also consider the implications of Section 83(b), particularly if the securities are subject to vesting or forfeiture.

Conclusion

The 83(b) election is a sophisticated financial planning tool that can offer substantial tax advantages for individuals receiving restricted stock in private companies. By allowing you to pay taxes on the current, often depressed, fair market value of the stock, it shifts future appreciation into the realm of capital gains, which are typically taxed at more favorable rates. However, this power comes with significant responsibility and risk. The immediate tax liability and the potential for forfeiture necessitate careful consideration, thorough due diligence, and expert advice. For founders and early employees navigating the exciting but often uncertain landscape of startups, understanding and strategically utilizing the 83(b) election can be a pivotal step in maximizing their financial outcomes. It’s not a decision to be taken lightly, but when executed correctly, it can be a cornerstone of building long-term wealth.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.