At first glance, the question “what is .4 as a fraction?” might seem like a simple mathematical exercise, a relic from elementary school. However, beneath this seemingly straightforward query lies a foundational principle critical for navigating the complex world of finance. In an era where financial data is omnipresent, from stock market reports and interest rates to personal budgets and investment returns, a deep understanding of how decimals and fractions interrelate is not just academic – it’s an essential pillar of financial literacy. This article will delve into the practical conversion of .4 to its fractional equivalent, then expand to explore why this seemingly trivial skill forms a bedrock for informed personal finance, shrewd investing, and robust business understanding.

The Foundational Importance of Fractions and Decimals in Finance

Financial discussions are inherently numerical. Whether you’re assessing a 2.5% interest rate, understanding a 1/3 share of a company, or calculating a 20% discount, decimals and fractions are the universal languages. They are not merely different ways of expressing numbers; they represent different perspectives that can illuminate distinct aspects of a financial situation. While calculators and software can instantly convert between these forms, a conceptual grasp of their relationship empowers individuals to interpret data more profoundly, question assumptions, and make more insightful decisions.

Bridging the Gap: From Abstract Numbers to Real-World Value

Imagine trying to understand the allocation of your budget. Seeing “0.25 of your income goes to housing” is technically correct, but visualizing “1/4 of your income” often provides a more intuitive sense of proportion and impact. Fractions inherently deal with parts of a whole, making them exceptionally powerful for understanding distributions, shares, and ratios – concepts at the heart of finance. Decimals, on the other hand, offer precision and are often preferred for calculations, especially when dealing with large numbers or when an exact value is needed, such as in interest rate calculations. The ability to fluidly move between these two forms allows for a comprehensive understanding of financial figures, transforming abstract numbers into tangible insights about real-world value.

The Language of Financial Literacy

Financial literacy isn’t just about knowing terms like “mortgage” or “stocks”; it’s about the ability to understand, analyze, and communicate financial information effectively. This requires numerical fluency. When an investment advisor mentions that a certain asset constitutes 0.4 of your portfolio, or a market report highlights that a company captured 0.4 of the new market share, converting that to 2/5ths provides an immediate, intuitive understanding of magnitude. It tells you that for every five parts, two belong to that category. This intuitive grasp is often more powerful than a decimal point when trying to convey scale or relative importance, especially in discussions with others or when trying to visualize complex financial structures.

Deciphering .4: A Step-by-Step Conversion for Financial Clarity

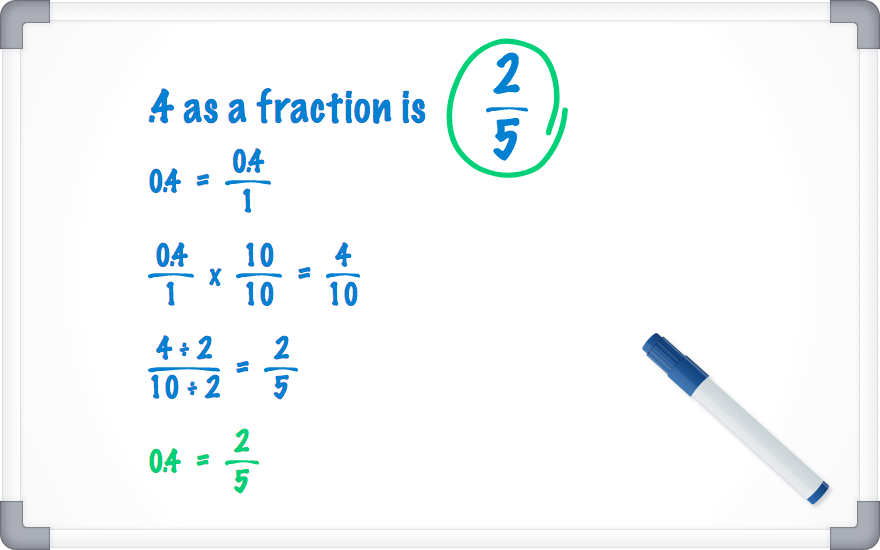

The conversion of .4 to a fraction is a fundamental mathematical operation that, when understood, unlocks a deeper comprehension of proportional relationships in finance. Let’s break down the process.

Understanding Place Value: The Key to Decimal Conversion

The decimal .4 signifies “four tenths.” In the decimal system, each position to the right of the decimal point represents a decreasing power of ten.

- The first digit after the decimal point is the “tenths” place.

- The second is the “hundredths” place.

- The third is the “thousandths” place, and so on.

So, .4 means 4 out of 10 parts. To write this as a fraction, we place the number after the decimal point over its corresponding place value.

Therefore, .4 becomes 4/10.

Simplifying the Fraction: Achieving the Most Useful Form

While 4/10 is a correct fractional representation of .4, it’s not in its simplest form. In mathematics and finance, we generally prefer fractions to be simplified to their lowest terms. This means dividing both the numerator (the top number) and the denominator (the bottom number) by their greatest common divisor (GCD).

For 4 and 10, the greatest common divisor is 2.

- Divide the numerator: 4 ÷ 2 = 2

- Divide the denominator: 10 ÷ 2 = 5

So, the simplest form of 4/10 is 2/5.

This simplified form, 2/5, is often the most insightful for financial applications, as it provides the clearest representation of the proportion.

Practical Applications of 2/5 in Financial Scenarios

Understanding that .4 equals 2/5 has numerous direct applications in finance:

- Budgeting: If 0.4 of your monthly income is allocated to discretionary spending, it means 2/5ths of your income is for non-essential items. This fraction visually emphasizes that nearly half of your income is going towards these expenses, prompting a re-evaluation if necessary.

- Investing: If a particular stock represents 0.4 of your investment portfolio, it means 2/5ths of your wealth is tied up in that single asset. This can immediately highlight a concentration risk, suggesting a need for diversification.

- Discounts and Sales: A retailer offering a “0.4 off” sale is giving you 2/5ths off the original price. This helps in quickly estimating the final cost or comparing different promotional offers.

- Business Ratios: In analyzing a company’s financial statements, if a certain ratio (e.g., debt-to-equity) is 0.4, interpreting it as 2/5ths can give a more intuitive sense of the company’s financial leverage or health relative to its peers.

Beyond Simple Conversion: Applying Fractional Thinking in Personal Finance

The ability to convert .4 to 2/5 is merely the entry point. The real value lies in cultivating “fractional thinking” – a mindset that uses proportions and ratios to understand and manage personal finances more effectively.

Budgeting and Allocating Resources with Fractions

Budgeting is fundamentally about allocating a finite whole (your income) into various parts (expenses, savings, investments). Fractional thinking excels here. Instead of just seeing percentages or decimal allocations, viewing your budget in terms of fractions helps you visualize the relative weight of each category.

- “1/10 for savings”

- “1/2 for essentials”

- “1/5 for debt repayment”

- “2/5 for discretionary spending” (our .4 example)

This perspective makes it easier to identify imbalances, such as too large a fraction going to non-essential spending, or too small a fraction being saved. It aids in creating a balanced financial pie that aligns with your goals.

Understanding Discounts, Interest Rates, and Returns

Financial transactions often involve fractional components.

- Discounts: A “20% off” sale is equivalent to 1/5 off. A “40% off” sale is 2/5 off. Understanding these fractional equivalents allows for quick mental calculations and comparisons of deals. Is 1/3 off better than 2/5 off? Yes, 1/3 is approximately 0.33, while 2/5 is 0.40, so 2/5 off is a better deal.

- Interest Rates: While often expressed as decimals (e.g., 0.05 for 5%), understanding that 5% is 1/20 gives a clearer picture of what that rate means over time, especially in simple interest calculations. If you’re borrowing money at 1/20 interest, for every $20 you borrow, you pay $1 in interest per period.

- Investment Returns: A 1/10 return on investment (10%) provides a clearer mental model of growth than just 0.10, especially when considering compounding over multiple periods.

Analyzing Investment Portfolios and Diversification Ratios

Diversification is key in investing, and it’s inherently about fractions. Your portfolio is a whole, made up of various asset classes, sectors, and geographies.

- If your portfolio has 2/5 (.4) in tech stocks, 1/5 in real estate, and 2/5 in bonds, you immediately understand the relative weighting and potential risks.

- Fractional thinking helps in setting and maintaining target allocations. If your target is to have no more than 1/4 of your portfolio in a single sector, you can quickly assess if you’re over-allocated when a sector grows to 0.3 of your holdings. It prompts rebalancing to ensure your risk exposure aligns with your comfort level.

Fractional Insights in Business Finance and Economic Understanding

The power of fractional thinking extends beyond personal finance into the realm of business and macroeconomics, providing crucial context for decision-making and analysis.

Interpreting Financial Ratios and Performance Metrics

Businesses rely heavily on financial ratios to assess performance, solvency, efficiency, and profitability. These ratios are almost always expressed as decimals or fractions.

- Current Ratio (Current Assets / Current Liabilities): A ratio of 0.4 (or 2/5) would indicate serious liquidity issues, as the company only has $0.40 in current assets for every $1 in current liabilities. Understanding this as 2/5ths makes the precarious position more vivid. A healthy ratio is typically above 1 or 1/1.

- Debt-to-Equity Ratio: If a company has a debt-to-equity ratio of 0.4 (2/5), it means for every $5 of equity, there are $2 of debt. This is generally considered conservative, indicating good financial health. A higher fraction, like 3/1 (3.0), would signal significant leverage and potentially higher risk.

Interpreting these ratios through a fractional lens allows business owners, investors, and analysts to quickly grasp the underlying financial health and operational efficiency of a company.

The Role of Fractions in Market Share and Economic Data

Understanding market dynamics and economic trends often involves grasping proportions.

- Market Share: If a company captures 0.4 of a new market segment, it controls 2/5ths of that segment. This provides a clear competitive advantage and insights into market dominance. Conversely, if its market share drops from 1/2 to 2/5, it signifies a notable decline.

- Economic Indicators: Government budgets often allocate fractions of GDP to various sectors (e.g., healthcare, defense). Understanding that 0.4 of a country’s exports go to a particular region highlights significant economic dependencies. Similarly, a central bank might indicate that 0.4 of inflation is driven by energy costs, pinpointing a critical factor for policymakers.

Making Informed Business Decisions with Proportional Reasoning

From product pricing strategies to resource allocation and investment decisions, businesses constantly engage in proportional reasoning.

- Resource Allocation: A business might decide to allocate 2/5 of its marketing budget to digital channels, 1/5 to print, and 2/5 to experiential marketing. This fractional breakdown provides clarity on strategic priorities.

- Profit Sharing: Partnerships or employee bonus structures often involve fractional profit sharing. Understanding that 0.4 of the profits go to a specific partner means 2/5ths of the financial success is distributed to them.

- Break-even Analysis: While often done with specific numbers, the conceptual understanding of what fraction of total capacity needs to be utilized to cover fixed costs is a fractional insight crucial for strategic planning.

Tools and Strategies for Mastering Financial Math

While conceptual understanding is paramount, leveraging available tools and continually honing your skills can further enhance your financial numeracy.

Leveraging Digital Tools and Calculators

In the modern financial landscape, digital tools are indispensable. Online calculators, spreadsheet software (like Excel or Google Sheets), and financial apps can perform complex calculations and conversions instantly. For instance, inputting 0.4 into a fraction converter will immediately yield 2/5. While these tools reduce the need for manual calculation, understanding the underlying principles (like place value and simplification) allows you to verify results, troubleshoot errors, and confidently interpret the output. They are powerful aids, but not substitutes for foundational knowledge.

The Enduring Value of Mental Math and Estimation

Despite the prevalence of digital aids, the ability to perform quick mental math and estimations based on fractional understanding remains incredibly valuable.

- On-the-spot decisions: Quickly estimating 2/5 of $100 (which is $40) when considering a 40% discount can save time and prevent overspending.

- Sanity checks: If a calculator gives you an answer that seems wildly off, your mental estimation using fractions can serve as a quick sanity check. For example, if you’re expecting something around 2/5 of a value, but the calculator shows 4/5, you know to re-examine your input.

- Enhanced comprehension: The mental exercise of converting and simplifying strengthens your grasp of numbers and proportions, making you a more astute financial observer.

Continuous Learning: Building Your Financial Numeracy

Financial literacy is not a one-time achievement but an ongoing journey. Regularly engaging with financial content, practicing mathematical conversions, and consciously applying fractional thinking to your daily financial interactions will significantly boost your confidence and competence. Reading financial news, analyzing personal statements, or even reviewing business reports from a fractional perspective can transform abstract numbers into meaningful insights, empowering you to make more informed, strategic, and ultimately, more successful financial decisions. The simple question, “what is .4 as a fraction?” opens the door to a richer, more powerful understanding of the financial world around us.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.