In the world of personal finance and professional investing, numbers are the primary language of communication. While many of us learn basic arithmetic in primary school, the transition from theoretical fractions to practical decimals is where the true mastery of money begins. When someone asks, “What is 3/4 as a decimal?” the mathematical answer is a straightforward 0.75. However, in the context of your bank account, your investment portfolio, and your long-term wealth strategy, 0.75 represents much more than a simple calculation. It represents 75%—a critical threshold for budgeting, a significant move in interest rates, and a common benchmark for portfolio performance.

Understanding the decimal representation of 3/4 is the first step toward high-level financial literacy. Whether you are calculating interest on a high-yield savings account or determining your debt-to-income ratio, the ability to pivot between fractions and decimals allows for a more nuanced understanding of where your money is going and how it is growing.

The Mathematics of Wealth: Converting Fractions to Financial Decimals

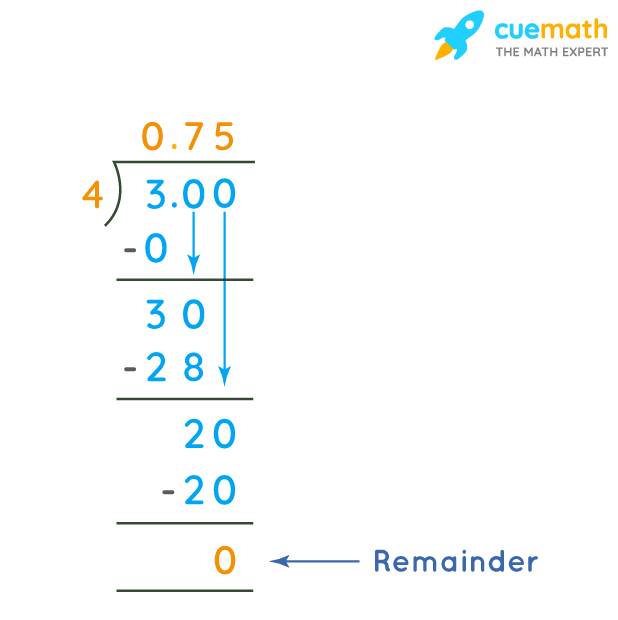

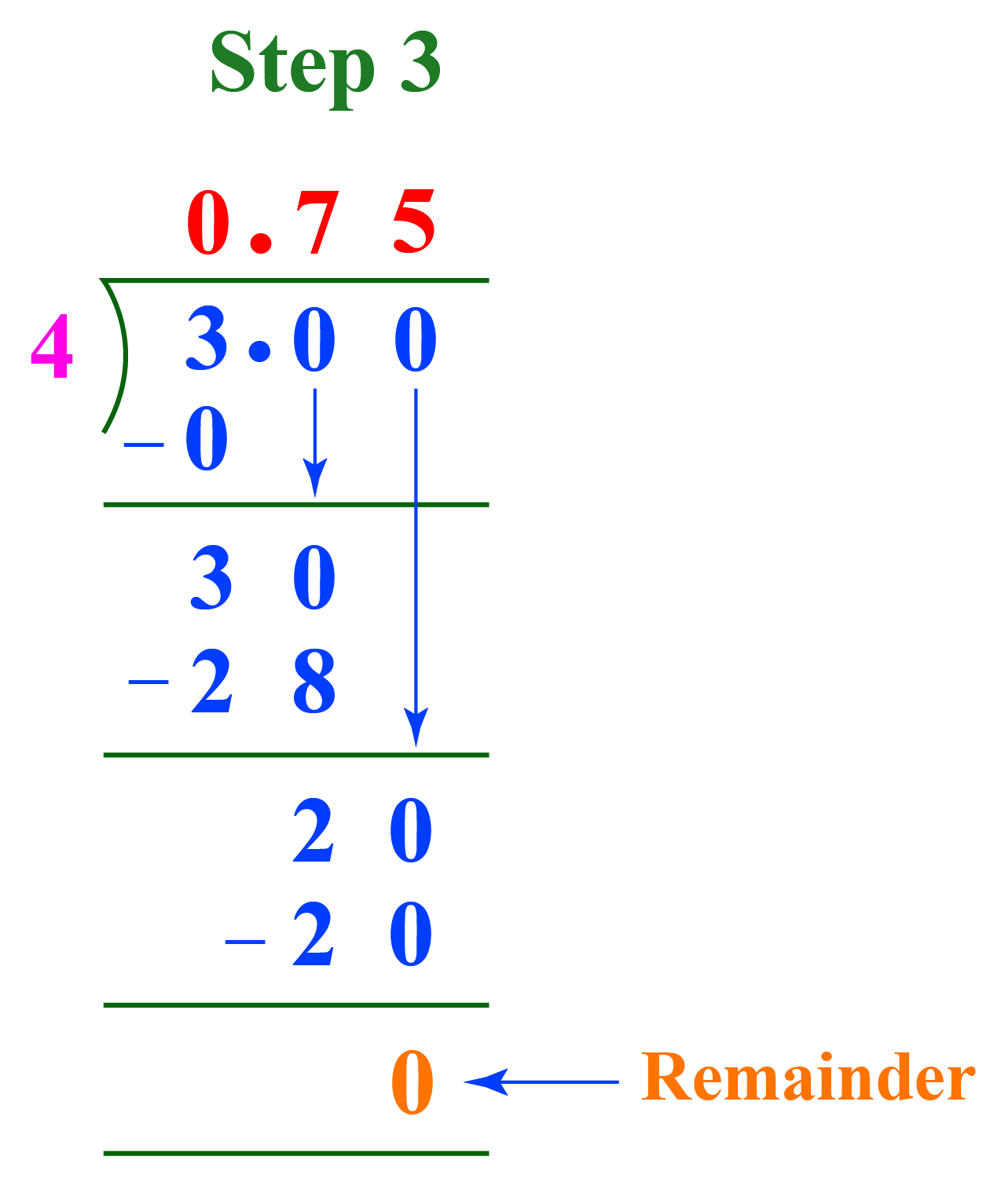

To understand why 0.75 is a cornerstone of financial calculations, we must first look at the mechanics of the conversion. A fraction like 3/4 is essentially an expression of division: three divided by four. In financial terms, this represents taking three parts of a four-part whole. When we convert this to a decimal—0.75—we are moving into the “base-10” system, which is the standard for almost every global currency and accounting software.

The Precision of Decimals in Accounting

In professional finance, decimals provide a level of precision that fractions cannot easily convey on a ledger. While 3/4 might suffice for a casual conversation about a business stake, a bank will always record that stake as 0.75 or 75%. This precision is vital when dealing with large sums of money. For instance, on a $1,000,000 investment, a discrepancy of even a few decimal points can result in thousands of dollars in gains or losses. By viewing 3/4 as 0.75, investors can align their mental math with the digital tools used by brokerage firms and banks.

Currency and the “Quarter” System

Our entire monetary system in the United States and many other nations is built on the concept of quarters. Since 1/4 of a dollar is $0.25 (a quarter), it follows logically that 3/4 of a dollar is $0.75. This fundamental relationship makes 0.75 one of the most recognizable and frequently used decimals in daily commerce. From tax rates to small-business margins, seeing the world in “quarters” and their decimal equivalents allows for quicker mental auditing of financial transactions.

The 75% Rule: Applying 0.75 to Budgeting and Asset Allocation

In the niche of personal finance, the number 0.75 often serves as a “Golden Ratio” for sustainable living and aggressive wealth building. Many financial advisors suggest that an individual should aim to live on 75% (0.75) of their net income, while allocating the remaining 25% (0.25) toward savings, debt repayment, and investments.

The Sustainable Lifestyle Buffer

Living on 0.75 of what you earn creates a 25% margin of safety. This margin is the difference between financial fragility and financial freedom. When you view your income through the lens of the 0.75 decimal, you treat 75 cents of every dollar as “spending money” and 25 cents as “future money.” This psychological shift is easier to maintain when you use decimals to track your spending. If your monthly take-home pay is $5,000, your “0.75 ceiling” is $3,750. Staying under this decimal threshold ensures that you are consistently building equity.

Asset Allocation and the 75/25 Split

For moderate-to-aggressive investors, the 0.75 ratio often appears in asset allocation. A common strategy for those with a long-term time horizon is to keep 0.75 of their portfolio in equities (stocks) and 0.25 in fixed income (bonds or cash). This 75% equity tilt captures the growth of the market while the 25% provides a cushion against volatility. Understanding that 3/4 of your wealth is tied to market performance allows you to calculate risk more effectively. If the stock market drops by 10%, you know immediately that the impact on your total portfolio is a 7.5% (0.075) reduction, rather than the full 10%.

Interest Rates and Basis Points: The Power of 0.75 in Macroeconomics

Perhaps the most impactful application of the 0.75 decimal is in the world of central banking and interest rates. In financial news, you will often hear about the Federal Reserve raising or lowering rates by “75 basis points.”

Understanding Basis Points

A basis point is one-hundredth of a percentage point (0.01%). Therefore, 75 basis points is equal to 0.75%. While 0.75% might seem like a small number in isolation, in the context of the global economy, it is a “jumbo” move. When interest rates rise by 0.75, the cost of borrowing for mortgages, credit cards, and business loans increases significantly.

The Impact on Mortgages and Loans

Consider a $400,000 mortgage. An increase of 0.75 (75 basis points) in the interest rate can result in hundreds of dollars more in monthly payments and tens of thousands of dollars in extra interest over the life of a 30-year loan. For a savvy borrower, knowing that 3/4 of a percent is 0.75 allows them to use online calculators more effectively to forecast their future liabilities. It allows for a deeper understanding of “APR” (Annual Percentage Rate) and how small decimal shifts impact long-term net worth.

Bond Yields and Fixed Income

For bond investors, a 0.75 shift in yields is a massive event. Bond prices and yields move in opposite directions. If the yield on a 10-year Treasury note increases by 0.75, the market value of existing bonds with lower rates will drop. Professional traders use the decimal 0.75 to calculate “duration,” which measures how much a bond’s price will fluctuate based on interest rate changes.

Fractional Shares and Dividend Yields: Precision in Modern Investing

The rise of “Fintech” has made the conversion of 3/4 to 0.75 more relevant than ever for the average retail investor. In the past, you had to buy whole shares of a stock. Today, platforms allow for the purchase of fractional shares.

Owning 0.75 of a Share

If a single share of a high-priced tech stock costs $1,000, but you only have $750 to invest, you now own 0.75 of that share. This decimal ownership means you are entitled to 0.75 of the dividends and 0.75 of the capital gains. Understanding this decimal relationship is crucial for tracking your “cost basis.” If you buy 0.75 of a share today and 0.25 of a share next month, you finally own 1.00 full share. Keeping track of these decimals is essential for tax reporting and portfolio balancing.

Analyzing Dividend Ratios

Dividend yields are almost always expressed as decimals or percentages. If a stock has a dividend yield of 3.4%, and it increases its payout so that the yield becomes 4.15%, the change is 0.75. Investors look for these decimal increments to determine if a company is becoming more or less efficient at returning value to shareholders. A company that consistently grows its dividend by 0.75% annually can provide a significant “yield on cost” over a decade, thanks to the power of compounding.

The Psychological Value of 0.75 in Business and Marketing

Finally, we must consider the business finance aspect of 0.75. In pricing psychology and profit margin analysis, the decimal 0.75 plays a strategic role.

Profit Margins and the 0.75 Threshold

For many retail and service businesses, a gross margin of 0.75 (or 75%) is considered the gold standard for scalability. This means that for every $1.00 of revenue, the cost of goods sold is only $0.25, leaving $0.75 to cover overhead, marketing, and net profit. Entrepreneurs who monitor their margins in decimals can quickly identify when their business is becoming inefficient. If a margin slips from 0.75 to 0.65, it signals a 10% increase in costs that must be addressed immediately to save the business’s bottom line.

Psychological Pricing and the “Rule of Quarters”

In marketing and sales, prices ending in .75 are often used to signal value or a “premium discount.” While .99 is used for mass-market appeal, .75 is frequently seen in professional services or high-end boutique pricing. Financially, these decimals add up. A business owner selling 10,000 units of a product at $19.75 vs. $19.00 is generating an additional $7,500 in pure profit—all by understanding the value of that three-quarter decimal.

Conclusion: Why 0.75 is the Decimal of Financial Clarity

While “what is 3/4 as a decimal” might begin as a simple school-age question, its implications in the world of money are profound. The conversion to 0.75 is a bridge between basic math and sophisticated financial management. It allows you to:

- Budget with a Margin of Safety: By living on 0.75 of your income.

- Invest with Precision: By understanding fractional shares and asset allocation.

- Analyze Macro Trends: By recognizing the weight of a 75-basis-point interest rate hike.

- Optimize Business Growth: By maintaining 0.75 profit margins.

In the pursuit of wealth, clarity is power. The more comfortably you can move between the fraction 3/4 and the decimal 0.75, the more prepared you are to navigate the complexities of the modern financial landscape. Numbers are not just symbols; they are the roadmap to your financial independence. When you see 0.75, don’t just see a decimal—see the potential for three-quarters of a dollar to grow, compound, and secure your future.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.